Limited Company Buy-to-Let Mortgages

Buying a rental property through a limited company can change how lenders assess your mortgage. It can also affect tax, legal ownership, rental profit and long-term planning. That is why a limited company buy-to-let mortgage needs more than a rate search. At Connect Mortgages, we help landlords arrange buy-to-let mortgages through UK limited companies, including SPVs, portfolio landlords, HMOs and refinancing cases. If you are deciding whether to buy personally or through a company, we can explain the mortgage route. You should also speak to a qualified accountant or tax adviser before choosing your ownership structure.

Limited Company Buy-to-Let Mortgagesat a Glance

A limited company buy-to-let mortgage is used when a company buys or refinances a rental property. Most landlords use a Special Purpose Vehicle, often called an SPV. This is a company set up mainly to hold rental property.

The structure may suit landlords who want to build a portfolio, retain profits within a company or plan long term. However, it may not suit every landlord.

Lenders will assess the company, property, rent, directors, shareholders and wider portfolio. They may also ask for personal guarantees from directors.

Before applying, check the tax position, deposit, rental income, company structure and lender criteria.

You can also review our wider Buy-to-Let Mortgage guide.

What is Limited Company Buy-to-Let Mortgages?

A limited company buy-to-let mortgage is a mortgage for a rental property owned by a limited company.

The company is usually a Special Purpose Vehicle. Many lenders prefer SPVs because the company has a simple purpose: owning and letting property.

The mortgage is secured against the rental property. The lender will assess whether the rent supports the loan.

The lender may also review:

- The company registration details

- The SIC codes

- The directors and shareholders

- Director income and credit history

- Expected or current rental income

- The property type and condition

- Deposit or equity level

- Existing buy-to-let portfolio

- Landlord experience

- The repayment strategy

Limited company buy-to-let mortgages are usually used for investment properties. They are not designed for buying your main home.

What Is an SPV Buy-to-Let Mortgage?

An SPV buy-to-let mortgage is a limited company mortgage where the company is set up for property investment.

SPV stands for Special Purpose Vehicle. In this context, it usually means the company exists to buy, own and let property. Lenders often expect the company to use property-related SIC codes. These codes help show the company’s activity.

Common SIC codes may include property letting, property management or buying and selling real estate. The right code depends on the company’s purpose.

You should check the company structure with your accountant before applying.

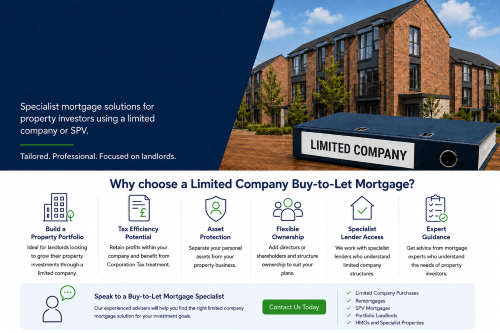

Why Landlords Use Limited Companies For Buy-to-Let

Some landlords use a limited company because it can support long-term property planning.

This may include:

- Buying rental property through an SPV

- Keeping rental profit within the company

- Reinvesting profits into future property purchases

- Separating rental property from personal ownership

- Managing a growing portfolio

- Planning how income is taken from the company

- Working with other shareholders or family members

However, the structure is not automatically better. It can involve higher admin, accountancy, and legal costs, as well as different lender rules. A tax adviser should confirm whether the company route suits your wider financial position.

Limited Company Buy-to-Let Mortgage Benefits

A limited company buy-to-let mortgage may offer useful planning options for some landlords.

Possible mortgage and planning benefits

- The structure may support portfolio growth.

- Some lenders assess company applications differently.

- Profits may be retained inside the company.

- It may help separate property activity from personal assets.

- It can support joint investment between directors or shareholders.

- It may suit landlords buying more than one rental property.

- It may help landlords build a clearer property business structure.

Important tax note

Mortgage advice and tax advice are not the same. Connect Mortgages can advise on mortgage options and lender criteria. A qualified accountant or tax adviser should advise on tax, profit extraction, incorporation and company structure.

How Lenders Assess Limited Company Buy-to-Let Mortgages

Limited company buy-to-let lenders look at both the property and the people behind the company.

They may review the company first. This includes the company name, registration date, structure, SIC codes and trading activity.

They will then assess the directors and shareholders. This can include credit history, income, experience and existing mortgage commitments.

The property also matters. Lenders will check the rent, valuation, location, condition and tenancy type.

Some lenders may consider first-time landlords. Others prefer applicants with landlord experience.

If you already own several rental properties, visit our Buy-to-Let Portfolio Mortgages page.

Deposit Requirements For Limited Company Buy-to-Let

Limited company buy-to-let mortgages usually need a larger deposit than residential mortgages.

Many lenders ask for around 20% to 25% deposit. Some cases may need more.

The deposit can depend on:

- Property type

- Rental income

- Loan-to-value ratio

- Director profile

- Landlord experience

- Company structure

- Credit history

- Fixed-rate period

- Lender stress test

- Whether the property is an HMO

A larger deposit may improve lender choice. However, rental income still needs to pass lender checks. You can use the Buy-to-Let Affordability Calculator to estimate your borrowing capacity.

Personal Name vs Limited Company Buy-to-Let

| Area | Personal Name Buy-to-Let | Limited Company Buy-to-Let |

|---|---|---|

| Ownership | You own the property personally | The company owns the property |

| Mortgage borrower | Individual applicant | Limited company, usually with director guarantees |

| Tax treatment | Rental income forms part of personal tax position | Company profits are subject to Corporation Tax |

| Admin | Usually simpler | More company filing and accounting duties |

| Lender choice | Often broad | Specialist lender criteria may apply |

| Portfolio planning | May suit smaller or simpler cases | May suit landlords planning to grow |

| Advice needed | Mortgage and tax advice | Mortgage, tax, legal and accountancy advice |

The right route depends on your plans, income, tax position and property strategy.

Mortgage Advice..

Thinking of getting a mortgage? Our experienced team of skilled mortgage advisers are here to offer the essential guidance you require. Relying on our comprehensive understanding of the mortgage market, we’ll ensure you secure the perfect mortgage to suit your specific situation.

Rental Income And Stress Testing

Buy-to-let lenders usually assess whether the rent covers the mortgage payment by a set margin.

This is often called rental coverage or interest cover.

For limited company buy-to-let mortgages, the calculation can vary by lender. Some lenders use different stress rates for company applications.

The result may depend on:

- Monthly rent

- Mortgage amount

- Interest rate used for testing

- Fixed-rate period

- Property type

- Loan-to-value ratio

- Company structure

- Wider landlord portfolio

- Whether the property is let as a single let or HMO

This is why one lender may decline a case that another lender may accept.

Limited Company Buy-to-Let Mortgage Rates

Limited company buy-to-let mortgage rates can differ from personal name buy-to-let rates.

The rate is only one part of the mortgage cost.

You should also consider:

- Arrangement fees

- Valuation fees

- Legal fees

- Early repayment charges

- Stress testing

- Product length

- Reversion rate

- Rental coverage rules

- Personal guarantee requirements

- Whether the lender fits your company structure

The lowest headline rate may not be the best option if the criteria do not fit your case.

Risks And Costs To Check Before You Apply

A limited company buy-to-let mortgage should be reviewed carefully before you apply.

Check the following first:

- Company setup and accountancy costs

- Legal fees for company purchases

- SDLT position

- Capital Gains Tax if transferring property

- Corporation Tax position

- Dividend or salary planning

- Personal guarantee requirements

- Higher product fees

- Rental stress testing

- Exit strategy

- Future refinancing plans

This is where joined-up mortgage, tax and legal advice matters.

Can I Transfer A Buy-to-Let Property Into A Limited Company?

You may be able to move a personally owned buy-to-let property into a limited company. However, this is not a simple name change.

In many cases, the company buys the property from you. That can create tax, legal and mortgage consequences.

You may need to consider:

- Stamp Duty Land Tax

- Capital Gains Tax

- Legal fees

- Valuation costs

- Existing mortgage charges

- Early repayment charges

- New lender underwriting

- Company setup costs

- Accountant advice

- New mortgage affordability checks

You should not transfer property into a company without tax and legal advice.

Connect Mortgages can explain the mortgage process. Your accountant and solicitor should explain the tax and legal position.

Limited Company Buy-to-Let For Portfolio Landlords

Limited company buy-to-let mortgages can be relevant for portfolio landlords.

If you own four or more mortgaged rental properties, many lenders will assess you as a portfolio landlord.

They may ask for:

- A property schedule

- Mortgage balances

- Monthly rental income

- Property values

- Tenancy details

- Business plan

- Bank statements

- Tax documents

- Evidence of landlord experience

A portfolio case can involve more paperwork. Good preparation can reduce delays.

You can read more in our Buy-to-Let Portfolio Mortgages guide.

Limited Company HMO Mortgages

Some landlords buy HMOs through limited companies.

An HMO can provide higher rental income, but the mortgage assessment can be more detailed.

Lenders may look at:

- HMO licence position

- Number of tenants

- Number of bedrooms

- Room-by-room rent

- Property layout

- Fire safety requirements

- Landlord experience

- Local authority rules

- Valuation method

Some lenders prefer experienced landlords for HMO lending.

For more detail, visit our HMO Property page.

Documents You May Need

Limited company buy-to-let applications often need more documents than a simple residential mortgage.

You may be asked for:

- Company registration details

- Company bank statements

- Director ID

- Proof of deposit

- Personal bank statements

- Existing mortgage statements

- Property schedule

- Tenancy agreement

- Rental valuation

- Accountant details

- Company accounts, if available

- Personal tax documents

- Business plan for larger portfolios

Not every lender asks for the same documents. We can help you prepare for the lender most likely to fit your case.

When A Limited Company Buy-to-Let Mortgage May Suit You

A limited company buy-to-let mortgage may suit you if:

- You plan to build a rental portfolio

- You want to buy through an SPV

- You are buying with other shareholders

- You want to retain profits inside the company

- You already own several rental properties

- You are buying an HMO or specialist rental property

- You have received tax advice supporting this route

- You want a clearer property business structure

It may not suit you if:

- You only want one simple rental property

- You do not want company admin

- Your accountant advises against it

- The tax costs outweigh the benefits

- Lender rates or fees make the case unsuitable

- You need personal access to rental income straight away

Why Use Connect Mortgages?

Limited company buy-to-let mortgages need careful lender matching.

At Connect Mortgages, we help landlords understand which lenders may consider their company structure, property type and rental position.

We can help with:

- SPV buy-to-let mortgages

- Limited company purchases

- Limited company remortgages

- Portfolio landlord mortgages

- HMO buy-to-let mortgages

- Landlord refinancing

- Rental income assessment

- Complex property investment cases

We are a credit broker, not a lender. We will assess your needs and recommend suitable mortgage options based on your circumstances.

Find A Limited Company Buy-to-Let Mortgage Adviser

Some landlords want direct mortgage advice from Connect Mortgages. Others may want to compare adviser profiles first.

If you want to compare advisers by location or specialism, you can use Find Mortgage Advisers on Connect Experts.

Connect Experts is part of the Connect IFA trading style. Mortgage advice is provided by the adviser or firm selected by the customer.

FAQs: Limited Company Mortgages

Most frequent questions and answers about limited company mortgages

Yes. A limited company can get a buy-to-let mortgage if it meets lender criteria. Most lenders prefer an SPV company set up for property investment. They will also assess the directors, shareholders, rent and property.

Many business buy-to-let mortgages are not regulated by the FCA. Some cases may be regulated if they meet consumer buy-to-let rules. Your adviser can explain how your case is treated.

The amount of deposit required will depend on the lender and the type of property being purchased. When it comes to limited company buy-to-let mortgages, lenders commonly ask for a higher deposit than they do with standard residential mortgages, usually, at least 20-25% equity or deposit (sometimes even more). As a result, savvy investors who have lower loan-to-value ratios will possess more choices.

Many lenders prefer SPVs because the company has a clear property purpose. Some lenders may consider trading companies. However, criteria can be more limited and more detailed.

Yes, some landlords buy HMOs through limited companies. The lender will assess the HMO licence, rent, layout, landlord experience and valuation.

You may be able to, but it can trigger tax, legal and mortgage costs. The company may need to buy the property from you. Always take tax and legal advice first.

Some lenders consider first-time landlords using a limited company. Other lenders prefer landlord experience, especially for HMOs or larger borrowing.

Many lenders ask directors to provide personal guarantees. This means directors may remain personally liable if the company cannot meet its mortgage obligations.

What next?

We will come back to you quickly to let you know how we can help. If you would like to speak to us immediately, call us on 01708 676 111.

Looking for our intermediaries site?

Liz Syms is the CEO and Founder of Connect Mortgages and Connect for Intermediaries, a leading firm specialising in property investment finance. With more than 25 years of experience in the mortgage and financial services industry, Liz has helped thousands of clients secure both residential homes and investment properties.

Renowned for her expertise and commitment to excellence, Liz is passionate about delivering tailored, high-quality advice on mortgages and protection. Her leadership has positioned her as a trusted figure in the sector, and under her guidance, Connect Mortgages has expanded to a national team of over 300 advisers.

Driven by a vision to make Connect Mortgages one of the UK’s most successful mortgage networks, Liz continues to champion professional standards and client-focused solutions across the industry.

About the Author

Liz Syms is the CEO and Founder of Connect Mortgages, a specialist in finance for property investment. With over 25 years of experience in mortgages and financial services, Liz has helped countless people get their dream homes and investment properties. She is passionate about giving her clients the best advice possible when it comes to financial decisions relating to mortgages and protection and is dedicated to providing the highest quality of service. With her wealth of knowledge in the industry, Liz is a respected leader in mortgages and financial services and has grown her team to over 300 advisers nationally. She strives to make Connect Mortgages one of the most successful companies in its field.