Remortgage

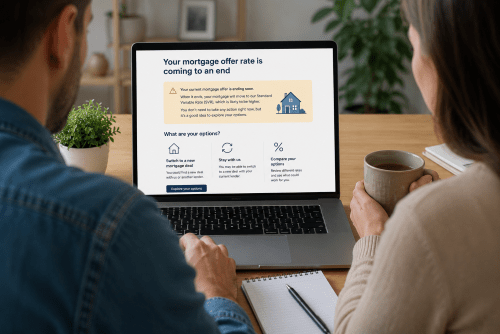

Review your mortgage before your current deal ends Your mortgage rate can change when your fixed, tracker or discount period ends. For many homeowners, this is the point where monthly payments may rise. Therefore, it can help to review your mortgage before your lender moves you onto its Standard Variable Rate. Connect Mortgages helps UK homeowners understand their remortgage options. You may want a new rate, lower monthly payments, more certainty, or a way to raise money against your home. You can also compare whether a full remortgage or a product transfer may be more suitable.

What is a Remortgage?

A remortgage means replacing your current mortgage with a new mortgage on the same property.

You are not moving home. Instead, you are reviewing the mortgage secured against your current home.

A remortgage may help you:

- Review your rate before your current deal ends

- Avoid moving onto a higher Standard Variable Rate

- Borrow more for home improvements

- Release equity from your home

- Change your mortgage term

- Move from interest-only to repayment

- Review your options after income or credit changes

However, remortgaging is not always the right answer. Fees, early repayment charges, affordability checks and lender criteria all matter.

Why Homeowners Review Their Mortgage

A mortgage is often one of the largest monthly commitments in a household.

When your current rate ends, your lender may move you to its Standard Variable Rate. This rate may be higher than your current deal.

That is why many homeowners review their mortgage several months before the current deal ends.

A review can help you understand:

- What your current lender may offer

- What other lenders may consider

- Whether your home value has changed

- Whether your loan-to-value has improved

- Whether your income still fits lender criteria

- Whether borrowing more is possible

- Whether keeping your mortgage as it is may be better

For wider home finance support, you can also read our residential mortgage advice page.

When Should You Start Looking at a Remortgage?

It is sensible to review your mortgage before your current deal ends.

Many lenders allow a new deal to be arranged months in advance. This can give you time to compare options without rushing.

You may want to start reviewing your mortgage if:

- Your fixed-rate deal ends soon

- Your tracker rate is becoming less suitable

- Your monthly payment is due to rise

- Your property value may have increased

- Your income has changed

- You want to borrow more

- You want to reduce the mortgage term

- You want more payment certainty

If you are unsure how much you can borrow, our residential affordability calculator can help you get started.

Remortgage or Product Transfer?

A remortgage and a product transfer are not the same. A remortgage usually means moving your mortgage to a new lender. The new mortgage pays off your existing mortgage.

A product transfer means staying with your current lender and switching to a new deal. Both options can be useful. However, they work differently.

A remortgage may suit you if:

- Another lender may offer a more suitable deal

- You want to borrow more

- Your circumstances have changed

- Your current lender has limited options

- You want to review the wider market

- You need a different mortgage structure

A product transfer may suit you if:

- You want to stay with your current lender

- You want a simpler process

- You do not need to borrow more

- Your circumstances have become more complex

- You want to avoid a new full lender application

A mortgage adviser can help you compare both routes before you decide.

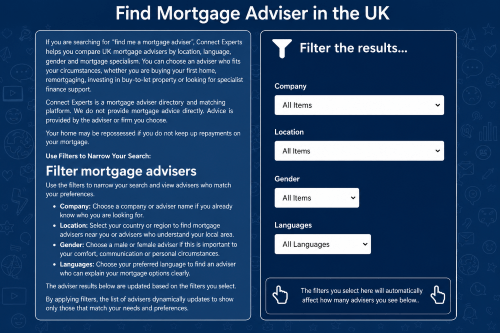

If you want to search for an adviser by mortgage type, location or language, you can use Connect Experts to find a residential adviser for a new rate.

What lenders may check when you remortgage

A remortgage is still a mortgage application.

Lenders usually assess your income, outgoings, credit history, property value and mortgage balance.

They may also look at:

- Employment status

- Bonus, overtime or commission income

- Self-employed income

- Existing debts

- Childcare costs

- Credit commitments

- Loan-to-value

- Property type

- Reason for borrowing more

- Remaining mortgage term

If your situation has changed since your last mortgage, lender choice can matter.

Reasons People Remortgage

Homeowners remortgage for different reasons. The right route depends on your mortgage, income, property value and plans.

To review a rate before it ends

This is one of the most common reasons.

If your current rate is ending, you may want to compare a new fixed rate, tracker rate or other available option.

To avoid the Standard Variable Rate

Your lender’s Standard Variable Rate may be higher than your current rate.

Reviewing before the deal ends can help you avoid a sudden payment change.

To release equity

If your home has increased in value, you may be able to release equity.

This means borrowing more against your home. The money may be used for home improvements, debt consolidation or another purpose.

You should always consider the risks before increasing borrowing secured against your home.

To fund home improvements

Some homeowners remortgage to pay for renovations, repairs or extensions.

The lender will consider affordability, equity and the reason for borrowing.

To consolidate debt

Some people remortgage to consolidate unsecured debt.

This can reduce monthly payments. However, it may increase the total amount repaid over time.

You should take advice before securing short-term debts against your home.

To change the mortgage term

You may want to shorten your mortgage term to repay the loan sooner.

Alternatively, you may want to extend the term to reduce monthly payments.

Both choices affect the overall cost of borrowing.

To switch mortgage type

You may want to move from interest-only to repayment.

You may also want to move from a variable rate to a fixed rate for more certainty.

Mortgage Advice..

Thinking of getting a mortgage? Our experienced team of skilled mortgage advisers are here to offer the essential guidance you require. Relying on our comprehensive understanding of the mortgage market, we’ll ensure you secure the perfect mortgage to suit your specific situation.

Remortgaging to Raise Money

Some homeowners remortgage to raise extra funds.

This is sometimes called capital raising.

Common reasons include:

- Home improvements

- Debt consolidation

- Family support

- School fees

- Business purposes

- Buying another property

- Large planned expenses

The lender will ask why you want to borrow more.

They will also check affordability and available equity.

If a remortgage is not suitable, a second charge mortgage may be considered. This is a separate loan secured against your property.

What lenders may check when you remortgage

A remortgage is still a mortgage application.

Lenders usually assess your income, outgoings, credit history, property value and mortgage balance.

They may also look at:

- Employment status

- Bonus, overtime or commission income

- Self-employed income

- Existing debts

- Childcare costs

- Credit commitments

- Loan-to-value

- Property type

- Reason for borrowing more

- Remaining mortgage term

If your situation has changed since your last mortgage, lender choice can matter.

Can I Remortgage if My Income Has Changed?

Yes, you may still be able to remortgage if your income has changed.

However, the lender will need to check affordability.

This can matter if you have become self-employed, reduced your hours, changed jobs, taken maternity leave, retired or started contract work.

Some lenders may be more suitable than others.

If your income is complex, advice can help you avoid applying to a lender that is unlikely to fit your circumstances.

Can I Remortgage with Credit Problems?

It may be possible to remortgage with credit problems.

This depends on the type of credit issue, when it happened, the amount involved and your current financial position.

Credit issues may include:

- Missed payments

- Defaults

- County Court Judgments

- Debt management plans

- Bankruptcy

- Repossessions

- Payday loan history

Some lenders may still consider your application. However, rates and criteria can vary.

You can read more on our adverse credit mortgage advice page.

Should I Use a Mortgage Broker to Remortgage?

You can approach lenders directly.

However, a mortgage broker can help you compare more options and understand which lenders may fit your needs.

This can be useful when:

- Your deal is ending soon

- You want to borrow more

- Your income is complex

- Your credit file has changed

- You are unsure about product transfer options

- You want to compare total costs

- You want someone to manage the process

Connect Mortgages is a credit broker, not a lender. Our advisers review your circumstances before recommending a suitable option.

You can also search by adviser preference through Connect Experts’ residential mortgage adviser search.

Protecting Your Mortgage

A remortgage review can also be a good time to review protection.

Your mortgage may have changed since you first arranged cover.

Your income, family, debts, and monthly commitments may also differ.

You may want to review:

- Life insurance

- Critical illness cover

- Income protection

- Buildings insurance

- Contents insurance

You can read more about mortgage protection, life insurance, and buildings and contents insurance.

Choose an Adviser

Find Remortgage Advice Near You

Some homeowners prefer to speak with an adviser who understands their local area.

Others prefer telephone or online advice.

Connect Mortgages can help you speak with advisers across the UK.

You can also use our mortgage brokers near you page to find location-based support.

FAQs: Remortgage

Most frequent questions and answers about remortgage

If you’re borrowing more on your existing mortgage or switching products, with the same lender (known as a product transfer) then there are no legal charges involved. However, if you move to a new rate or a different deal with your current lender, or move to an entirely different lender, then you will need to use a solicitor or conveyancer. You can use the lender’s conveyancer if this service is included with your chosen product, or you can appoint your own.

When you remortgage, your existing mortgage will be replaced with a new one. It may involve changing lenders, or simply switching to a different deal with your current lender. Your new mortgage can usually offer more favourable terms such as a lower interest rate or more flexibility.

Yes, it is possible to remortgage with blemishes on your credit file. However, you may have difficulty finding a lender, willing to offer favourable terms. It’s also likely that the interest rate will be higher.

Having a poor credit history doesn’t necessarily mean that you won’t get a mortgage – many specialist lenders assess on a case-by-case basis.

Contact a Connect broker in the first instance if you’re concerned about your credit history.

It is possible to remortgage and pay off the debt by borrowing more, if there is sufficient equity in the property. It pays to explore all options before taking additional borrowing to consolidate your debt – after all this would mean taking the debt over a longer period in line with the chosen mortgage term.

Yes, a remortgage can be used to fund the purchase of a second property. Depending on your circumstances, you may need to release equity or use savings to make up the difference. It’s important to speak to an experienced mortgage advisor before making any decisions to purchase additional properties – this could result in you paying stamp duty.

The funds from the remortgage loan are released and your existing mortgage is paid off in full. The new lender then becomes responsible for collecting future payments under the new agreement. The new deal will become effective from the first monthly payment.

No, a deposit is not required to remortgage. In most cases, remortgaging can be done without having to access any savings. Instead, you can use the equity that has built up in your property over time.

No, you can approach lenders directly, but using a mortgage broker like Connect Mortgages gives you access to a wider range of deals, including exclusive rates not available on the high street. A broker will assess your needs, handle the paperwork, and guide you through the process saving you time, stress, and potentially money.

What next?

We will come back to you quickly to let you know how we can help. If you would like to speak to us immediately, call us on 01708 676 111.

Looking for our intermediaries site?

Liz Syms is the CEO and Founder of Connect Mortgages and Connect for Intermediaries, a leading firm specialising in property investment finance. With more than 25 years of experience in the mortgage and financial services industry, Liz has helped thousands of clients secure both residential homes and investment properties.

Renowned for her expertise and commitment to excellence, Liz is passionate about delivering tailored, high-quality advice on mortgages and protection. Her leadership has positioned her as a trusted figure in the sector, and under her guidance, Connect Mortgages has expanded to a national team of over 300 advisers.

Driven by a vision to make Connect Mortgages one of the UK’s most successful mortgage networks, Liz continues to champion professional standards and client-focused solutions across the industry.

About the Author

Liz Syms is the CEO and Founder of Connect Mortgages, a specialist in finance for property investment. With over 25 years of experience in mortgages and financial services, Liz has helped countless people get their dream homes and investment properties. She is passionate about giving her clients the best advice possible when it comes to financial decisions relating to mortgages and protection and is dedicated to providing the highest quality of service. With her wealth of knowledge in the industry, Liz is a respected leader in mortgages and financial services and has grown her team to over 300 advisers nationally. She strives to make Connect Mortgages one of the most successful companies in its field.