Moving Home Mortgages

Moving home is not only about finding the next property. It is also about deciding what happens to your current mortgage. You may be able to take your existing mortgage deal with you. This is known as porting. However, you may need a new mortgage if your current deal is not suitable, not portable, or no longer competitive. Connect Mortgages helps UK home movers compare their options before they commit to their next property. We can explain porting, new mortgage deals, affordability checks, early repayment charges and the cost of borrowing more. Contact Connect Mortgages to discuss your moving home mortgage options. Your home may be repossessed if you do not keep up repayments on your mortgage.

Moving Home Mortgages

If you are moving home with a mortgage, you usually have two main choices.

- You may be able to port your current mortgage to the new property.

- You may choose a new mortgage with your current lender or another lender.

- Your lender will still check affordability, credit history and the new property.

- You may need to borrow more if the new home costs more.

- You may face early repayment charges if you leave your current deal.

- A mortgage adviser can compare both options before you decide.

You can also use the Residential Affordability Calculator to estimate what you may be able to borrow.

Choose a Mortgage Adviser

What Is a Moving Home Mortgage?

A moving home mortgage is the mortgage you arrange when buying your next home.

You may already have a mortgage on your current property. When you move, that mortgage does not automatically transfer to the new home. Your lender must agree to the change, and the new property must meet their criteria.

There are usually two routes to consider.

- Port your current mortgage deal to the new home.

- Replace your current mortgage with a new mortgage deal.

The right route depends on your current rate, your lender’s rules, your new property, your income and the total cost of moving.

Can You Move Your Existing Mortgage To A New Home?

You may be able to move your existing mortgage to another property if your deal is portable.

This is called porting a mortgage. It means you keep your current mortgage product, including the rate and remaining deal period.

However, porting is not guaranteed. Your lender will treat the move as a new application. They will check your income, outgoings, credit profile and the new property.

Porting may be useful if:

- Your current rate is lower than new rates available today.

- You want to avoid or reduce early repayment charges.

- You are happy to stay with your current lender.

- Your new property meets the lender’s rules.

- Your borrowing amount is still affordable.

If the new home costs more, you may need extra borrowing. This extra amount may sit on a separate rate. It may also have a different product end date.

When Might a New Mortgage Be Better?

A new mortgage may be better if porting does not suit your plans.

This may apply if your current mortgage is not portable, your lender will not approve the new property, or your financial position has changed. It may also apply if another lender offers a more suitable deal.

A new mortgage may help if:

- You need to borrow more than your current lender allows.

- Your current lender’s criteria no longer fit your circumstances.

- You want to change your mortgage term.

- You want to change from interest-only to repayment.

- You want to compare more lenders before moving.

- Your current deal has no early repayment charge.

If you are unsure whether to port or switch, read our Remortgage Guide to understand how changing deals can work.

Porting Or New Mortgage: What Should You Compare?

Do not choose based on rate alone. The right option depends on the total cost.

Compare:

- Current mortgage rate

- New mortgage rate

- Early repayment charges

- Product fees

- Valuation fees

- Legal costs

- Broker fees, where applicable

- Monthly repayment changes

- Mortgage term

- Extra borrowing rate

- Future flexibility

A lower rate may not always mean a cheaper move. Fees and early repayment charges can change the result.

How Lenders Assess Home Movers

Lenders will check whether the new mortgage is affordable.

Even if you have paid your current mortgage on time, the lender will still review your case. This is because the loan, property and risk may change when you move.

Lenders may review:

- Income and employment

- Self-employed income evidence

- Credit commitments

- Dependants

- Monthly household costs

- Deposit or equity

- Property value

- Property type

- Loan-to-value

- Mortgage term

- Credit history

If your income has changed since your last mortgage, get advice early. This helps avoid delays once you find a property.

You can start with the Quick Mortgage Calculator to estimate monthly repayments.

Upsizing: Borrowing More When You Move

If your next home costs more, you may need a larger mortgage.

This can affect affordability because the lender must check the full borrowing amount. Your deposit may come from savings, equity in your current home, or both.

You should check:

- How much equity you may have

- How much deposit you need

- Whether your income supports higher borrowing

- Whether your current mortgage can be ported

- Whether extra borrowing will be on a different rate

- Whether the new monthly payment is comfortable

Upsizing can work well when planned early. However, extra borrowing can affect your budget after the move.

Downsizing: Moving To A Lower-Value Property

If you are moving to a lower-value property, you may need a smaller mortgage.

This can reduce your monthly payments or clear part of your mortgage balance. However, your current mortgage terms still matter.

You should check whether:

- Early repayment charges apply

- Your lender allows partial repayment

- Your mortgage can be reduced when ported

- You want to keep, reduce or repay your loan

- The new property meets lender criteria

Downsizing may seem simple, but the mortgage details still need checking before you agree to a sale or purchase.

Mortgage Advice..

Thinking of getting a mortgage? Our experienced team of skilled mortgage advisers are here to offer the essential guidance you require. Relying on our comprehensive understanding of the mortgage market, we’ll ensure you secure the perfect mortgage to suit your specific situation.

What Costs Should Home Movers Budget For?

Moving home can involve more than the mortgage deposit.

Common costs may include:

- Stamp Duty, where applicable

- Estate agent fees

- Solicitor or conveyancing fees

- Survey costs

- Valuation fees

- Mortgage product fees

- Broker fees, where applicable

- Removal costs

- Early repayment charges

- Mortgage exit fees

- Buildings insurance

You can use our Stamp Duty Calculator to estimate Stamp Duty costs before you move.

What If You Cannot Sell Your Current Home First?

Some homeowners find a new property before their current home sells.

In this situation, you may need to consider whether you can keep the existing property and buy the next one. This can be complex because lenders may assess both mortgages.

Possible options may include:

- Waiting until your current home sells

- Asking your lender about consent to let

- Considering let-to-buy

- Reviewing short-term finance options

- Reducing the purchase price for the next home

Let-to-buy may allow you to rent out your current home and buy another property. However, this depends on rental income, equity, affordability and lender criteria.

If your move depends on keeping your current property, speak to an adviser before making an offer.

Moving Home When You Are Self-Employed

Moving home can be more detailed if you are self-employed.

Lenders may ask for accounts, tax calculations, tax year overviews and business bank statements. They may also assess your income differently.

You should prepare early if:

- Your latest income has changed.

- You changed from employed to self-employed.

- You trade through a limited company.

- You retained profits in the business.

- You have variable income.

- You have recent business borrowing.

Connect Mortgages can help you understand how lenders may view your income before you apply.

Moving Home With Credit Issues

A past credit issue does not always stop a home move. However, it can affect lender choice.

Credit issues may include missed payments, defaults, county court judgments, debt management plans or previous arrears.

Lenders may consider:

- Type of credit issue

- Date it was registered

- Whether it has been settled

- Size of the issue

- Deposit amount

- Current credit conduct

- Income and affordability

If you have credit concerns, get advice before applying. This can reduce the risk of declined applications.

Protecting Your New Home

When you move, your protection needs may change.

A larger mortgage, different term, new household costs or a change in family circumstances can affect the cover you need.

You may want to review:

- Life insurance

- Critical illness cover

- Income protection

- Mortgage protection insurance

- Buildings and contents insurance

Read more about Mortgage Protection Insurance and Buildings and Contents Insurance before completion.

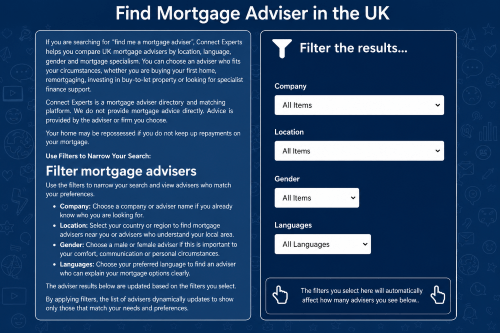

Looking For A Mortgage Adviser Near You?

Some home movers prefer to speak with an adviser based on location, language or mortgage type.

You can use Connect Experts to find a mortgage adviser to help you move home. Connect Experts is a mortgage adviser directory and matching platform. Advice is provided by the adviser or firm you choose.

You can also read the Connect Experts Moving Home Mortgage Guide for extra guidance before choosing an adviser.

FAQs: Moving Home

Most frequent questions and answers about moving home

Yes, it is possible to move your mortgage from one house to another. This process is known as a “portable” mortgage. You will need to qualify for the new loan, and you may incur additional fees or costs associated with the transfer. Your lender can provide more details on what is involved in transferring your mortgage to a different property.

Yes, you can move house on a fixed term mortgage. However, depending on your lender’s terms and conditions, there may be additional costs associated with transferring the mortgage to another property. You will also need to qualify for the new loan and ensure that all of your financial obligations are met in order for the transfer to take place.

Not necessarily. If you’re struggling to sell, some lenders may allow a ‘consent to let’ arrangement where you rent out your current home temporarily. You may also consider a let-to-buy mortgage, allowing you to let your existing property and use released equity as a deposit for your next home.

The typical deposit is 5% to 20% of the new property’s value, depending on the mortgage product and your credit profile. If you’re porting your mortgage or using equity from your current home, your deposit may come from the sale proceeds or a remortgage arrangement.

If you’re upsizing, you may need to borrow more, which could involve a top-up mortgage or switching to a new deal entirely. Your lender will assess your affordability based on both existing and new borrowing if you still own your previous property.

Yes. As a current homeowner, lenders view you as a home mover, not a first-time buyer. While many mortgage features are similar, you may have access to different rates, and your eligibility will depend on equity, existing commitments, and credit history.

Absolutely! In fact, using a broker can be especially helpful when moving. A broker like Connect Mortgages can compare deals from multiple lenders, assist with porting, and manage the paperwork all while ensuring you’re getting the best option for your situation.

Beyond your mortgage, plan for:

Stamp Duty (if applicable)

Estate agent fees (if selling)

Legal/conveyancing costs

Survey and valuation fees

Moving company expenses

Your adviser will help estimate total costs and ensure you’re financially prepared.

What next?

We will come back to you quickly to let you know how we can help. If you would like to speak to us immediately, call us on 01708 676 111.

Looking for our intermediaries site?

Liz Syms is the CEO and Founder of Connect Mortgages and Connect for Intermediaries, a leading firm specialising in property investment finance. With more than 25 years of experience in the mortgage and financial services industry, Liz has helped thousands of clients secure both residential homes and investment properties.

Renowned for her expertise and commitment to excellence, Liz is passionate about delivering tailored, high-quality advice on mortgages and protection. Her leadership has positioned her as a trusted figure in the sector, and under her guidance, Connect Mortgages has expanded to a national team of over 300 advisers.

Driven by a vision to make Connect Mortgages one of the UK’s most successful mortgage networks, Liz continues to champion professional standards and client-focused solutions across the industry.

About the Author

Liz Syms is the CEO and Founder of Connect Mortgages, a specialist in finance for property investment. With over 25 years of experience in mortgages and financial services, Liz has helped countless people get their dream homes and investment properties. She is passionate about giving her clients the best advice possible when it comes to financial decisions relating to mortgages and protection and is dedicated to providing the highest quality of service. With her wealth of knowledge in the industry, Liz is a respected leader in mortgages and financial services and has grown her team to over 300 advisers nationally. She strives to make Connect Mortgages one of the most successful companies in its field.