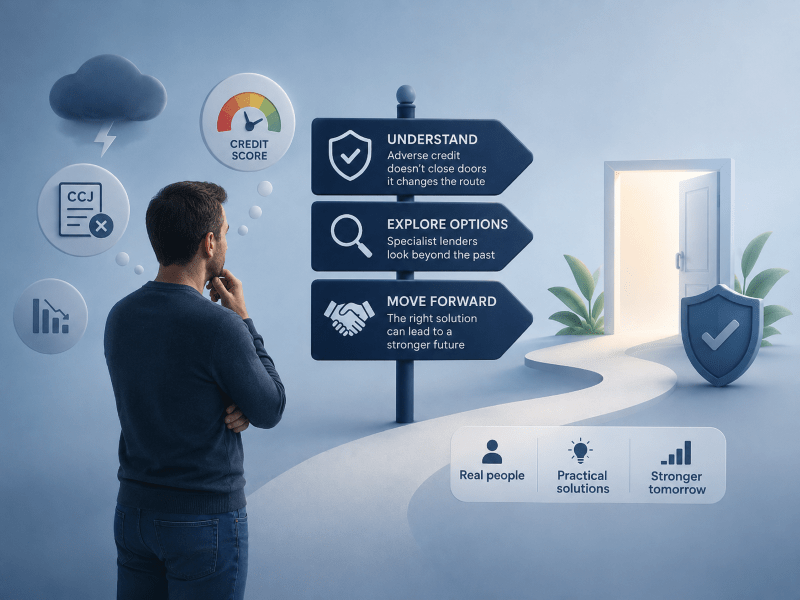

The Fear of Adverse Credit: How Lenders Assess Risk – A credit file can feel like a record of mistakes. Yet mortgage lending is not built on memory alone. It is built on risk, evidence, affordability and timing.

Adverse credit may affect your mortgage options, but it does not always close the door. A missed payment, default, County Court Judgment, debt management plan or previous bankruptcy can all matter. However, lenders also look at what happened, when it happened, whether it has been settled, and how your finances look today.

Fear often grows when people do not know what lenders can see. Clarity begins when the credit issue is named, measured and understood.

At a Glance

Adverse credit can make a mortgage more complex, but it does not always mean a mortgage is impossible. Lenders usually assess the type of credit issue, how recent it was, whether it was settled, the deposit size, loan-to-value, income stability, affordability and the property itself. A larger deposit, cleaner recent conduct and clear documents may improve your position. Before applying, check your credit file, avoid repeated applications and speak with an adviser who understands adverse credit mortgages.

What does adverse credit mean?

Adverse credit means your credit history shows previous financial difficulty. This may include missed payments, late payments, defaults, CCJs, debt management plans, IVAs, bankruptcy or repeated credit applications.

For mortgage purposes, the label matters less than the detail.

A lender may ask:

- What type of credit issue happened?

- How much money was involved?

- When was it registered?

- Has it been settled?

- Was it linked to a one-off life event?

- Has your recent credit conduct improved?

- Can the mortgage still pass affordability checks?

This is why two borrowers with “bad credit” may receive very different outcomes. One person may have a small settled default from several years ago. Another may have recent unpaid arrears. The words sound similar, but the lending risk is different.

For a broader guide, read our Adverse Credit Mortgage page.

Why Adverse Credit Creates Fear

The fear of adverse credit is rarely just about numbers. It is about being judged by a past version of yourself.

Many people delay seeking advice because they assume rejection is certain. Others apply too quickly, receive a decline, and then worry that every future lender will say the same thing.

A mortgage decline is not always a verdict on you. It may simply mean the lender’s criteria did not fit your circumstances. Some lenders prefer clean credit profiles. Others may consider specialist cases where the risk can be explained and evidenced.

The practical question is not “Will every lender accept me?”

The better question is, “Which lender criteria may fit the facts of my case?”

What Lenders Check When There is Adverse Credit

When adverse credit is present, lenders usually look beyond a simple credit score. They often assess the full shape of the application.

Key areas include:

- Credit event type: A missed utility payment may be viewed differently from mortgage arrears.

- Recency: Recent credit issues usually carry more weight than older ones.

- Settlement status: Settled credit issues may be viewed more positively than unpaid debts.

- Deposit size: A larger deposit can reduce the lender’s risk.

- Loan-to-value: Lower LTV often gives lenders more comfort.

- Affordability: Income, commitments, dependants and spending still matter.

- Income stability: Employed, self-employed and contractor income may be assessed differently.

- Property type: Flats, new builds, unusual construction and buy-to-let properties can add criteria layers.

- Reason for the issue: Some lenders may consider factors such as illness, redundancy, or divorce.

This is where adverse-credit mortgages get technical. A lender is not only asking whether something went wrong. They are asking whether the current risk is acceptable.

Credit Score Versus Lender Criteria

Many borrowers focus only on their credit score. That can be misleading.

A credit score is useful, but mortgage lenders do not all use the same scoring model. They also apply their own criteria. This means a low score may reduce options, but it may not tell the full story.

A lender may care more about:

- The date of the default

- The value of the CCJ

- Whether mortgage payments were missed

- Whether payday loans were used

- Whether debts are now settled

- The deposit available

- Current income and affordability

Before applying, it may help to review your Credit File so you can see what lenders may review.

Why Loan-to-Value Matters

Loan-to-value, often called LTV, compares the mortgage amount with the property value.

For example, a £180,000 mortgage on a £200,000 property is 90% LTV. A £150,000 mortgage on the same property is 75% LTV.

When adverse credit is present, LTV can become more important. A lower LTV means the borrower has more equity or deposit in the property. This may reduce the lender’s risk.

A larger deposit does not guarantee approval. However, it may improve the range of lenders willing to consider the case. It may also affect the interest rate and product options available.

The more recent or serious the credit issue, the more important the deposit can become.

Why Affordability Still Comes First

Adverse credit is not assessed in isolation. Lenders must still check whether the mortgage appears affordable.

Affordability may include:

- Basic salary

- Overtime, bonus or commission

- Self-employed income

- Benefits or maintenance income, where acceptable

- Credit commitments

- Childcare costs

- Household spending

- Dependants

- Future payment changes

A borrower may have an older default and a strong deposit but still fail affordability. Another borrower may have a smaller deposit but stable income and lighter commitments.

This is why affordability should be checked before a full application. You can use the Residential Affordability Calculator as an early guide, although it is not a mortgage offer.

Self-Employed Borrowers with Adverse Credit

Self-employed applicants can face extra checks when adverse credit is involved.

Lenders may want to understand:

- How long has the business been trading

- Whether accounts or tax calculations are available

- Whether income is stable or rising

- How net profit or salary and dividends are assessed

- Whether business debts affect personal affordability

- Whether the credit issue was personal or business-related

Some lenders may prefer two years of trading history. Others may consider shorter trading periods, depending on the case. The position can change by lender, income type and credit event.

For more detail, read our guide to Self-Employed Mortgages.

CCJs, Defaults and Missed Payments

Not all credit issues carry the same weight.

A missed payment may suggest short-term pressure. A default may suggest a credit agreement broke down. A CCJ may show that a debt has reached court action.

The timing also matters. A CCJ registered last month may be viewed differently from one registered five years ago. Whether it was paid and when can also affect lender confidence.

GOV. The UK explains that a County Court Judgment can remain on the Register of Judgments, Orders and Fines for 6 years. MoneyHelper also explains that missed payments, CCJs, and several credit applications over a short period can affect your credit position.

These facts do not mean every lender will say no. They mean the application needs to be prepared carefully.

What to do Before Applying

The worst time to understand your credit file is after a mortgage decline.

Before applying, take these steps:

- Download your credit reports from more than one credit reference agency.

- Check that names, addresses and linked accounts are correct.

- Look for missed payments, defaults, CCJs and unsettled debts.

- Correct any errors before submitting a mortgage application.

- Avoid making several credit applications in a short period.

- Prepare bank statements, payslips, accounts or tax documents.

- Be ready to explain the reason for the credit issue.

- Check affordability before choosing a property or lender.

This preparation gives the adviser and lender a clearer picture. It also reduces the risk of applying to a lender whose criteria are unlikely to fit.

What Happens if a Mortgage Application is Declined?

A decline can feel final. In practice, it should be treated as information.

If your application has been declined, pause before applying elsewhere. Repeated applications can create more searches on your credit file and may reduce confidence further.

The next step is to understand why the application failed.

It may relate to:

- Credit score

- Recent missed payments

- Unsettled defaults

- Affordability

- Income evidence

- Deposit source

- Property valuation

- Lender policy

- Debt-to-income position

Once the reason is clear, the next application can be better targeted. In some cases, waiting may be the right decision. In others, a specialist lender may be more suitable.

When Specialist Lenders May Help

Specialist lenders may consider cases that some high-street lenders will not accept. This does not mean they ignore risk. It means they may assess the details differently.

They may consider:

- Older CCJs

- Settled defaults

- Debt management history

- Minor historic arrears

- Lower credit scores

- Complex income

- Self-employed income

- Larger deposits

Rates may be higher than standard products because the lender is pricing the risk. Fees, product terms and future remortgage options should also be considered.

The aim is not only to get accepted. The aim is to understand whether the mortgage is suitable, affordable and realistic.

The Role of an Adviser

An adviser can help turn uncertainty into a structured plan.

This may include reviewing the credit file, checking affordability, identifying lender criteria and deciding whether to apply now or wait. The adviser can also help present the case clearly, especially where the adverse credit was linked to a life event.

If you want to choose an adviser who understands credit concerns, you can use the Residential Credit Issues Mortgage Adviser Search on Connect Experts.

Connect Experts is a mortgage adviser directory and matching platform. It does not provide mortgage advice directly. Advice is provided by the adviser or firm you choose.

Can Adverse Credit Become Less Important Over Time?

Time can help, but time alone is not enough.

Lenders may place more weight on recent conduct. If the last few years show stable income, controlled spending and no further missed payments, the overall picture may improve.

A stronger future mortgage application may include:

- No recent missed payments

- Lower unsecured debt

- Settled defaults or CCJs

- Stable income evidence

- A larger deposit

- Clean bank statements

- Clear explanation of past issues

- Realistic borrowing expectations

Credit history records what happened. Mortgage lending asks what the risk looks like now.

That distinction matters.

FAQs

Can I get a mortgage with adverse credit?

You may still be able to get a mortgage with adverse credit, but this depends on your circumstances. Lenders may consider the type of credit issue, when it happened, whether it has been settled, your deposit, income and affordability.

Does a CCJ stop me getting a mortgage?

A CCJ can affect your mortgage options, but it does not always prevent a mortgage. Lenders may look at the amount, date, settlement status and the wider application.

Do I need a larger deposit with adverse credit?

A larger deposit may help because it reduces loan-to-value. However, it does not guarantee approval. Lenders still assess affordability, income, credit history and property suitability.

Should I apply straight after being declined?

It is usually better to pause and understand why the application was declined. Applying again too quickly may create further credit searches and could weaken the next application.

Do specialist lenders charge higher rates?

Specialist lenders may charge higher rates where the case presents more risk. The product should be reviewed carefully against affordability, fees, criteria and future remortgage plans.