Holiday Let Mortgages: Separating Myth from Market Reality!

Holiday lets often sit between two stories.

One story says they take homes away from local people. Another says they are an easy route to higher rental income.

The truth is usually more measured.

Holiday lets are not all the same. A coastal cottage, a rural lodge, a city apartment and an inherited family property may all sit under the same broad label. Yet each one can carry different planning rules, income patterns, running costs and mortgage requirements.

For landlords and property investors, the question is not whether holiday lets are good or bad. The better question is whether the property, location, mortgage and long-term plan work together.

That is where the conversation should begin.

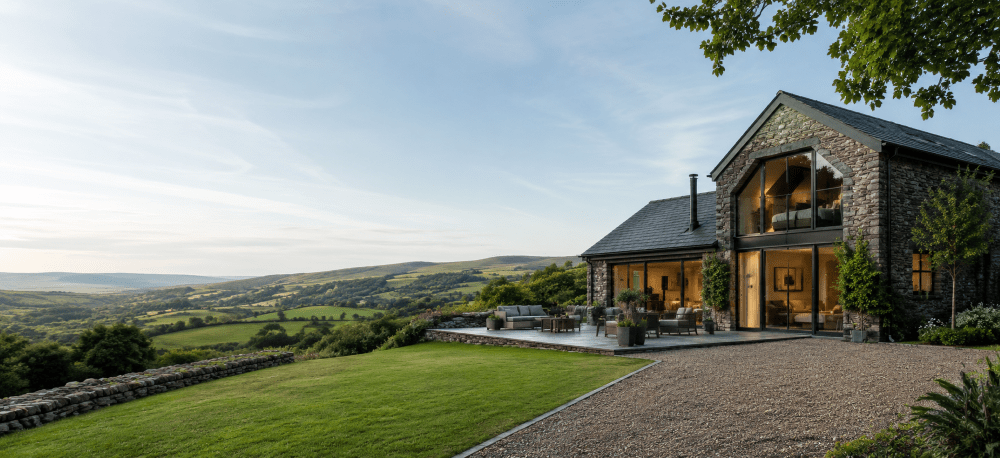

What Is a Holiday Let?

A holiday let is a property rented to guests on a short-term basis.

It may be used by visitors, families, business travellers or people staying in an area for leisure. Unlike a standard buy-to-let property, the income is usually seasonal. Bookings may be strong during peak periods, then quieter at other times of the year.

Because of this, holiday let mortgages are assessed differently from standard buy-to-let mortgages.

A standard buy-to-let lender may expect a long-term tenancy agreement. A holiday let lender may look at expected short-term rental income, location, property type, occupancy and wider affordability.

Myth 1: Holiday Lets Are Always Taking Homes From Local Residents

This is one of the most common assumptions.

In some areas, high levels of short-term letting can create local pressure. That concern should not be ignored. Housing supply, local employment and community balance all matter.

However, it is too simple to treat every holiday let as a lost family home.

Some properties were built for tourism. Some sit in locations where year-round residential demand is limited. Others may need a level of upkeep, marketing and management that differs from a normal rental home.

The UK Government has also confirmed plans for a mandatory national registration scheme for short-term lets in England. This is expected to begin in 2026. The aim is to give local authorities better data on the short-term lets operating in their area.

That matters because better data can lead to better decisions. A market cannot be properly understood if it is viewed only through assumptions.

Myth 2: Holiday Lets Are Only For Wealthy Investors

Holiday lets are often discussed as if they are only for cash-rich investors.

That is not always the case.

Some owners inherit a property and want to keep it in the family. Some buy in a location they know well. Others move from traditional buy-to-let because their plans have changed.

For some landlords, a holiday let may form part of a wider property portfolio. For others, it may be a single property with a clear lifestyle or investment purpose.

However, motivation does not remove responsibility.

A holiday let still needs a proper financial plan. Owners should think about mortgage payments, insurance, cleaning, repairs, utilities, management costs, booking fees, tax and quieter months.

Income can look attractive during peak season. Yet lenders and owners also need to consider the months when bookings may slow.

Myth 3: Holiday Lets Work Like Standard Buy-to-Let

Holiday lets and standard buy-to-let properties can both generate rental income. However, they do not operate in the same way.

A traditional buy-to-let property usually relies on monthly rent from a tenant. A holiday let relies on short stays, guest demand and seasonal booking patterns.

That changes the risk profile.

A holiday let may need:

- Active booking management.

- Cleaning between stays.

- Guest communication.

- Suitable insurance.

- Furniture and maintenance.

- Local compliance checks.

- Marketing and listing costs.

- A plan for quieter periods.

This is why mortgage advice matters. The lender must be comfortable with the property use. The borrower must also understand whether the expected income can support the borrowing.

If you are comparing options, our mortgage calculators can help you estimate monthly payments before you speak with an adviser.

Why Holiday Let Demand Has Stayed Relevant

UK holiday lets are linked to more than property investment.

They are also part of the wider domestic travel market. Many people still value UK breaks, shorter trips and flexible stays. Coastal towns, national parks, rural villages and historic cities can all attract visitors at different times of year.

This does not mean every holiday let will perform well.

Location remains central. So does pricing, presentation, access, local attractions, parking, transport links and guest demand.

A strong holiday let is not created by a mortgage alone. It depends on the relationship between the property, the market and the owner’s ability to manage the business.

Tax Changes Have Changed The Conversation

Holiday let owners should also understand the tax position.

The furnished holiday lettings tax regime was abolished from April 2025. Before then, qualifying furnished holiday lets received different tax treatment from some other property businesses.

This change means tax planning should be reviewed before buying, refinancing or changing how a property is used.

Connect Mortgages does not provide tax advice. You should speak to a qualified tax adviser or accountant before making ownership, company structure or disposal decisions.

However, the tax change is important for mortgage planning. If the expected net income changes, affordability and long-term returns may also change.

Planning And Registration Rules Matter

Holiday let rules can vary by location.

Some areas may have specific planning rules, licensing requirements or local restrictions. The UK Government has also said a national registration scheme for short-term lets in England is expected to begin in 2026.

Before buying or converting a property, owners should check:

- Local planning rules.

- Lease restrictions.

- Freeholder consent.

- Insurance requirements.

- Mortgage lender consent.

- Local authority rules.

- Tax position.

- Fire and safety duties.

- Management arrangements.

This is especially important if you plan to convert a residential property into a holiday let.

A property may look suitable on paper. Yet lender criteria, local rules and long-term running costs may tell a different story.

Holiday Let Mortgage Considerations

A holiday let mortgage is not the same as a residential mortgage.

You should not use a standard residential mortgage if the property will be let to paying guests. You may also find that a standard buy-to-let mortgage is not suitable for short-term letting.

Lenders may consider:

- Expected rental income.

- Personal income.

- Deposit size.

- Property location.

- Property type.

- Ownership structure.

- Previous landlord experience.

- Whether personal use is allowed.

- Seasonal demand.

- Existing borrowing.

- Credit history.

Some lenders may want evidence from a letting agent or holiday rental specialist. Others may look at projected income, comparable properties or wider affordability.

The right route depends on the case.

When A Holiday Let Mortgage May Be Suitable

A holiday let mortgage may suit you if:

- You want to buy a property for short-term guest stays.

- You already own a property and want to convert its use.

- You want to remortgage an existing holiday let.

- You understand seasonal income patterns.

- You have a clear plan for running costs.

- You have checked local rules.

- You have taken tax advice.

- You want to compare specialist lender options.

It may not be suitable if the property is mainly for personal use. It may also be unsuitable if the income is uncertain, the local rules are unclear, or the running costs are underestimated.

For indepth information visit our Holiday Let Mortgages for Property Investors page.

Why Advice Matters

Holiday let lending is a specialist area.

A mortgage adviser can help you compare the holiday let route with other options. These may include a standard buy-to-let mortgage, a residential remortgage, a second charge mortgage or commercial finance.

The right answer depends on the property and your circumstances.

You can start by reading more about buy-to-let mortgages or by visiting our guide to mortgage brokers near you.

If you want to search for an adviser with holiday let experience, you can also use Connect Experts to find a holiday let mortgage adviser.

A More Balanced Way To View Holiday Lets

Holiday lets should not be judged by headlines alone.

They can support tourism, help owners make use of suitable property and bring visitors into local economies. They can also create pressure in some areas if growth is not managed carefully.

Both points can be true.

That is why a better conversation is not built on myth. It is built on evidence, suitability and clear advice.

For landlords, the decision should come down to the numbers, the location, the rules and the long-term purpose of the property.

A holiday let can be a useful part of a property plan. It can also become expensive if the risks are misunderstood.

Connect Mortgages can help you review the mortgage side of that decision, so you understand the options before you apply.

Speak To Connect Experts

If you are thinking about buying, refinancing or converting a holiday let property, speak to Connect Mortgages.

We can help you understand the mortgage options available and explain how lenders may assess your case.

Visit Connect Experts Advisers to start your enquiry.

FAQs About Holiday Let Mortgages

What is a holiday let mortgage?

A holiday let mortgage is designed for a property rented to guests on a short-term basis. It is different from a standard residential mortgage or normal buy-to-let mortgage.

Can I use a residential mortgage for a holiday let?

Usually, no. If you plan to let the property to paying guests, you should tell your lender and seek advice. Using the wrong mortgage could breach your mortgage conditions.

Is a holiday let the same as buy-to-let?

No. A buy-to-let property is usually let to tenants under longer tenancy agreements. A holiday let is normally rented to short-term guests, often with seasonal income.

Are holiday lets still allowed in the UK?

Yes, but rules can vary by location. Owners should check planning rules, local authority requirements, lease terms, insurance and tax before buying or converting a property.

Is the furnished holiday lettings tax regime still available?

No. The furnished holiday lettings tax regime was abolished from April 2025. Owners should take tax advice before making decisions.

Do holiday let lenders use rental income?

Many lenders look at projected holiday let income. However, they may also consider personal income, deposit, property type, location and affordability.

Can I stay in my own holiday let?

Some lenders may allow limited personal use. Others may restrict it. You should check lender criteria before applying.

Are holiday let mortgages more expensive?

They can be. Rates, fees and deposit requirements may differ from standard residential or buy-to-let mortgages. The final cost depends on lender criteria and your circumstances.

Can I remortgage an existing holiday let?

Yes, subject to lender criteria. You may want to remortgage when your deal ends, raise funds, review the rate or change ownership structure.

Should I get mortgage advice before buying a holiday let?

Yes. Holiday let mortgages can be more complex than standard mortgage products. Advice can help you understand lender criteria, affordability, risks and suitable options.