UK Green Mortgages & Net Zero Homes | As global attention intensifies on climate change and sustainability, the United Kingdom has committed to achieving net-zero carbon emissions by 2050. This bold target is reshaping how we build, live, and invest, especially in the UK property and mortgage markets.

The transition to a net-zero future is not just a government objective; it’s a shift influencing homebuyers, developers, and lenders alike. From energy-efficient homes to the rise of green mortgages, the UK is redefining housing priorities to align with environmental responsibility.

In this article, we explore how the UK’s drive toward net-zero homes is creating both challenges and opportunities for buyers, mortgage seekers, and industry professionals. We’ll also examine the growing importance of EPC ratings, how sustainable upgrades can affect remortgage valuations, and how this journey will shape sustainable housing for generations to come.

What Does Net Zero Mean?

Net zero refers to the balance between the greenhouse gases a country emits and the amount it removes from the atmosphere. Achieving this state is a major step in reducing climate impact and advancing toward a low-carbon future. For the UK, net zero represents a long-term commitment to decarbonisation, aiming to reshape how we build, live, and invest in property.

For homeowners and buyers, this shift is already influencing mortgage choices, particularly with the rise of green mortgages and incentives for energy-efficient homes. If you’re planning to buy or improve a property, understanding how net-zero goals affect your mortgage options is more important than ever.

Learn more about how energy upgrades could impact your remortgage eligibility or access to specialist lending products.

The UK’s Policy Commitment to Net Zero

The UK government has established a strong legal framework to reduce emissions and promote sustainable housing. Since the Climate Change Act 2008, the country’s net-zero roadmap has evolved through major policies and frameworks that directly shape how homes are built, valued, and financed.

Key milestones include:

- The Net Zero Carbon Buildings Framework, which encourages carbon-conscious construction

- The Clean Growth Strategy, which promotes energy efficiency in homes

- The Green Industrial Revolution plan, driving investment in renewable technologies and sustainable infrastructure

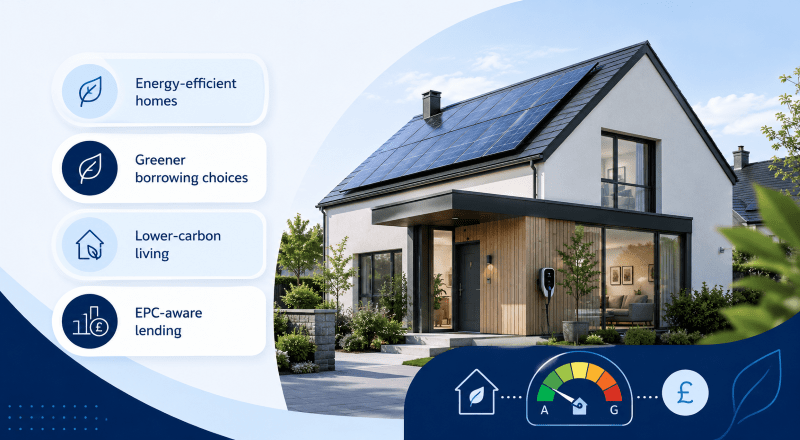

These initiatives signal a clear direction: future homes will need to meet higher environmental standards. As a result, lenders are increasingly factoring in EPC ratings, carbon emissions, and property sustainability when assessing mortgage applications.

Transitioning to Renewable Energy in the UK’s Net Zero Plan

Achieving net-zero emissions relies heavily on reducing dependence on fossil fuels and shifting to cleaner alternatives. In the UK, the transition to renewable energy is accelerating, with substantial growth in wind and solar power and in community-led green initiatives.

The expansion of offshore wind farms and consistent investment in cutting-edge green technologies are reshaping the national energy mix. These efforts are complemented by government-backed community energy projects that empower local areas to contribute to the country’s net-zero property goals.

As the energy sector evolves, homebuyers and investors are increasingly considering energy-efficient homes and green mortgages to align their property choices with environmental values.

Electrification and Sustainable Transport in the UK

Transportation accounts for a significant share of the UK’s carbon footprint, prompting a nationwide push toward sustainable transport solutions. To support its net zero goals, the UK government has committed to ending the sale of new petrol and diesel cars by 2030. This shift is driving rapid adoption of electric vehicles (EVs) and expanding access to EV charging infrastructure across residential and commercial areas.

In addition to electrification, new initiatives are promoting low-carbon travel alternatives such as walking, cycling, and enhanced public transport networks. These efforts are designed to reduce emissions, ease urban congestion, and create greener, more accessible communities that align with the future of energy-efficient housing.

Buyers exploring green mortgage options or investing in eco-conscious homes should also consider how sustainable transport links impact property value and eligibility for government incentives.

Green Building and Sustainable Infrastructure

The UK property market is undergoing a major shift as green building practices and sustainable infrastructure become central to reducing carbon emissions. With residential and commercial properties being major contributors to the UK’s carbon footprint, improving energy efficiency is a national priority.

For existing homes, the focus is on retrofitting insulation, upgrading to low-emission heating systems, and increasing EPC ratings through smart home technologies. For new builds, regulations continue to tighten, requiring developers to use sustainable materials and adopt eco-friendly construction methods that support the UK’s net zero targets.

Green infrastructure doesn’t just benefit the environment; it creates healthier, more efficient living spaces and can significantly boost a property’s long-term value. As a buyer or homeowner, choosing a home with strong energy performance may also increase eligibility for green mortgage options and lender incentives.

Sustainable Agriculture and Land Use: A Key to Net Zero

Reducing emissions from agriculture and land use is essential to achieving the UK’s net-zero targets. The government is working to reshape farming through sustainable land management, regenerative practices, and climate-resilient agriculture. Strategies such as peatland restoration and reforestation not only reduce greenhouse gas emissions but also enhance biodiversity, improve soil health, and help protect the UK’s natural ecosystems.

As green policies evolve, understanding how environmental goals influence property value, land use, and green mortgage eligibility will be vital for homebuyers and investors.

Green Finance and the Road to Net Zero

Reaching the UK’s net-zero targets requires significant investment in sustainable technologies, renewable infrastructure, and eco-conscious innovation. At the heart of this transformation is green finance, a growing sector that channels private capital into climate-aligned initiatives and energy-efficient developments.

The UK is taking a leadership role by developing clear regulatory frameworks that support green bonds, sustainability-focused funds, and financial instruments tied to environmental, social, and governance (ESG) criteria. These strategies help drive capital toward solutions that accelerate the net-zero property transition while ensuring long-term value for investors and homeowners.

Investing in a Net Zero Future

The journey toward a greener UK housing market is complex. While progress has been made in energy-efficient mortgages, EPC improvement incentives, and funding for low-carbon homes, the path ahead remains challenging. These include:

- Closing the technology gap for older, less efficient homes

- Making sustainability upgrades accessible to all income levels

- Maintaining political and financial momentum over the long term

At Connect Mortgages, we help homeowners and landlords explore finance options for eco-friendly property upgrades. If you’re considering a remortgage to fund insulation, heat pump installation, or solar panels, our advisers can help you compare rates and lenders.

Why Collaboration Matters

Creating a sustainable housing landscape takes more than policy. It requires collaboration between the government, lenders, homeowners, and communities. By encouraging public engagement, offering green mortgage advice, and building awareness around energy performance certificates (EPCs), we can drive real change.

If you’re unsure how your home’s energy efficiency could impact your mortgage, our Find Mortgage Advisers tool connects you with specialists who understand green lending criteria and how to navigate this growing space.