Remortgage vs Second Charge Mortgage: Which Route Fits? The right borrowing route is rarely the loudest option. It is usually the one that fits the numbers, the risk, and the reason for borrowing.

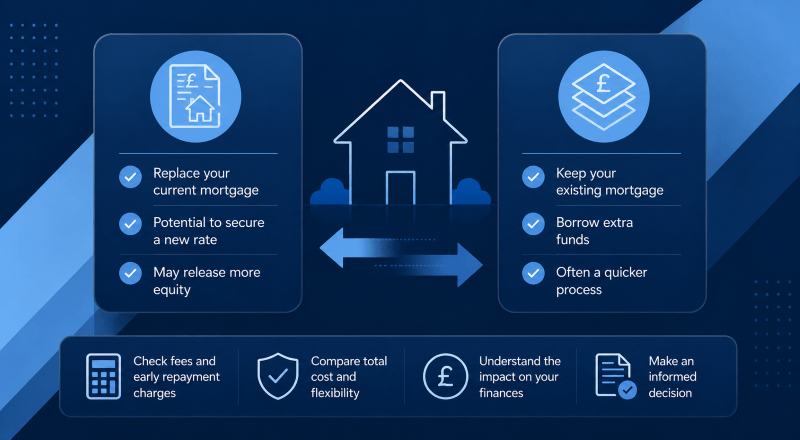

A remortgage and a second charge mortgage can both help homeowners raise funds from property equity. However, they work in different ways. A remortgage replaces your current mortgage with a new one. A second charge mortgage keeps your current mortgage in place and adds a separate loan secured against the same property.

That difference matters. It can affect your rate, monthly payments, early repayment charges, lender choice, legal work, affordability checks and long-term cost.

This guide explains the practical differences between remortgaging and taking a second-charge mortgage, so you can understand what an adviser may review before recommending a route.

Your home may be repossessed if you do not keep up repayments on your mortgage or any loan secured on it.

At a Glance

A remortgage may suit homeowners who want to replace their current mortgage, switch rate, change lender, raise extra funds, or combine borrowing into one new mortgage.

A second charge mortgage may suit homeowners who need extra borrowing but do not want to disturb their current mortgage deal. This can be relevant if they have a low fixed rate, face early repayment charges, or cannot borrow more from their current lender.

Neither option is automatically better. The right route depends on total cost, affordability, equity, credit profile, loan purpose and future plans.

Remortgage vs Second Charge Mortgage: Key Differences

| Feature | Remortgage | Second Charge Mortgage |

|---|---|---|

| What happens to your current mortgage? | It is replaced by a new mortgage | It stays in place |

| Number of secured loans | Usually one main mortgage | Two secured loans |

| Rate position | New rate applies to the whole mortgage balance | New rate applies only to the extra borrowing |

| Early repayment charges | May apply if you leave your current deal early | May help avoid disturbing the current deal |

| Monthly payments | Usually one mortgage payment | Two separate payments |

| Lender assessment | Full mortgage assessment | Second charge assessment plus consent from first lender |

| Legal charge | First legal charge | Second legal charge behind the main lender |

| Common use | New deal, rate switch, capital raising, debt consolidation | Capital raising without replacing the first mortgage |

| Main risk | Losing a favourable existing rate or paying exit costs | Higher rate on extra borrowing and another secured payment |

What Is a Remortgage?

A remortgage means replacing your current mortgage with a new mortgage. This may be with a new lender or, in some cases, a new deal with your existing lender.

Homeowners often consider a remortgage when their current deal is ending, their circumstances have changed, or they want to raise extra funds. The new mortgage may cover the existing balance plus the additional borrowing required.

This can be useful if the new rate, fees and loan size make sense as a whole. However, it can be less attractive if your existing mortgage has a strong rate that would be lost by switching.

A remortgage should be judged on total cost, not only the headline rate. Adviser checks may include:

- Your current balance

- Your current rate

- Any early repayment charge

- Exit, valuation, legal and product fees

- The new interest rate

- The new term

- Your income and outgoings

- Your credit profile

- The reason for raising funds

- The cost over the full mortgage term

What Is a Second Charge Mortgage?

A second charge mortgage is a separate loan secured against a property that already has a mortgage.

Your existing mortgage remains in place as the first charge. The new lender registers a second legal charge behind it. If the property had to be sold because payments were not maintained, the first charge lender would usually be repaid before the second charge lender.

Because the second lender sits behind the first lender, pricing and criteria can differ from a standard residential remortgage. A second charge mortgage may have a higher rate than a first charge mortgage, but that does not make it unsuitable in every case. The key question is whether it produces a better overall outcome than replacing the whole mortgage.

A second charge mortgage may be considered when:

- You want to keep your current mortgage rate

- You face high early repayment charges

- Your current lender will not offer further borrowing

- You need funds for home improvements

- You want to consolidate debts

- Your income needs specialist lender review

- Your credit history limits standard remortgage options

When Might a Remortgage Be More Suitable?

A remortgage may be more suitable when replacing the whole mortgage produces a better overall cost.

This can happen when your current deal is ending, early repayment charges are low, or the new rate is competitive. It may also help if you want one mortgage account rather than two separate secured payments.

A remortgage may also be useful if the extra borrowing is part of a wider financial plan. For example, you may be funding home improvements, changing the mortgage term, moving from interest-only to repayment, or reviewing your monthly budget.

However, care is needed. Extending the borrowing term can reduce the monthly payment but increase the total interest. Consolidating unsecured debts into a mortgage can also place those debts against your home.

When Might a Second Charge Mortgage Be More Suitable?

A second charge mortgage may be more suitable when the existing mortgage should be left alone.

This often happens when a homeowner has a low fixed rate that would be expensive to give up. It may also apply where a remortgage would trigger early repayment charges, or where the current lender will not allow the additional borrowing required.

For example, a homeowner may have a £220,000 mortgage on a low fixed rate and need £40,000 for an extension. If remortgaging means replacing the full £220,000 balance at a much higher rate, the total cost may be unattractive. A second charge mortgage may allow the £40,000 to be assessed separately while the main mortgage remains in place.

This does not remove risk. It adds another secured loan and another monthly payment. The question is whether that extra payment is affordable, sustainable and suitable when compared with the remortgage route.

Cost Is More Than the Interest Rate

The lowest rate is not always the lowest cost decision.

A remortgage may offer a lower rate than a second charge mortgage, but it could apply to the full mortgage balance. A second charge rate may be higher, but it may only apply to the new borrowing.

The comparison should include:

- The current mortgage rate

- The new mortgage rate

- The second charge rate

- Product fees

- Broker fees

- Valuation fees

- Legal fees

- Early repayment charges

- Exit fees

- Term length

- Monthly payment change

- Total amount repayable

Use the mortgage calculators to get a starting point on repayments, but do not treat calculator results as advice. They do not assess lender criteria, credit profile, legal charge position, fees or suitability.

Debt Consolidation Needs Extra Care

Both remortgages and second charge mortgages may be used for debt consolidation.

This can reduce monthly outgoings in some cases. However, it may increase the total amount repaid if debts are spread over a longer term. It can also turn unsecured borrowing, such as credit cards or personal loans, into borrowing secured against your home.

Before consolidating debt, an adviser should consider why the debt arose, whether spending has changed, and whether the new payment is realistic. Lower monthly cost alone is not enough. The long-term position must also make sense.

Regulation and Adviser Evidence

Second charge mortgages are regulated mortgage products. They need proper affordability checks, suitability assessment and clear disclosure of costs and risks.

The Financial Conduct Authority has reviewed second charge mortgage advice, fees, charges and affordability assessments. This makes evidence important. A recommendation should show why one route was considered more suitable than the other, not simply that the client wanted extra funds.

You can read the FCA’s review of second-charge mortgages and consumer outcomes for the regulatory context.

A good advice file should consider:

- The client’s reason for borrowing

- Current mortgage terms

- Early repayment charges

- Equity and loan-to-value

- Income and committed expenditure

- Credit history

- Alternative borrowing routes

- Total cost comparison

- Impact of debt consolidation

- Protection needs linked to higher borrowing

If borrowing increases, it may also be sensible to review mortgage protection and life insurance. The issue is not only whether the loan can be arranged. It is whether the household can keep payments going if life changes.

Choosing Between the Two

The decision should begin with a simple question: what are you trying to protect?

If you are trying to protect a low existing mortgage rate, a second charge mortgage may deserve review. If you are trying to reset the whole mortgage onto a better structure, a remortgage may be more suitable.

If you are trying to reduce short-term pressure, both routes need careful testing. A lower monthly payment can feel helpful today but still cost more over time.

MoneyHelper also explains that homeowners may be better off remortgaging where there is equity, no large early repayment charge and circumstances have not changed. It also notes that a second charge mortgage uses the home as security, so the risk must be understood before applying. Read MoneyHelper’s guide to second charges or second mortgages for independent guidance.

Speak to an Adviser

Connect Mortgages can help you compare remortgage and second charge mortgage options before you apply.

Some clients also prefer to choose an adviser by location, language or specialist experience. Connect Experts lets you find a second charge mortgage adviser or use the wider Find Mortgage Advisers directory.

Connect Experts is a directory and matching platform. Mortgage advice is provided by the adviser or firm selected by the customer.

FAQs: Remortgage vs Second Charge Mortgage

Is a second charge mortgage better than a remortgage?

Not always. A second charge mortgage may help if you want to keep your current mortgage deal, but a remortgage may be cheaper if your existing deal is ending or early repayment charges are low.

Is a second charge mortgage more expensive?

The rate on a second charge mortgage can be higher than a first charge mortgage. However, it may only apply to the extra borrowing. The full comparison should look at total cost, fees and term.

Can I remortgage to release equity?

Yes, subject to lender criteria, affordability and property value. The new mortgage would usually replace the existing mortgage and include the extra borrowing.

Can I use a second charge mortgage for home improvements?

Yes, many homeowners use second charge mortgages for home improvements. The lender will still assess affordability, equity, credit profile and the purpose of the funds.

Can I use either option to consolidate debt?

Yes, but this needs careful advice. Consolidating unsecured debt into secured borrowing can increase the total cost and puts your home at risk if payments are not maintained.

Will my current mortgage lender need to know about a second charge mortgage?

Yes. The first charge lender will usually need to consent before a second charge can be registered against the property.

Which option is quicker?

Timescales vary by lender, property, legal work and case complexity. A second charge mortgage may be quicker in some cases, but speed should not override suitability.

What should I compare before deciding?

Compare the interest rate, fees, early repayment charges, monthly payment, full term cost, flexibility, debt purpose, affordability and the risk of securing more borrowing against your home.