Specialist Mortgage Brokers: Some mortgage cases are not difficult because the borrower has not done anything wrong. They are difficult because the situation does not fit a standard lender box.

You may be self-employed, receive income from several sources, buy an unusual property, invest through a limited company, or raise funds without changing your current mortgage. In these cases, a specialist mortgage broker can help you understand which lenders may consider your circumstances before you apply.

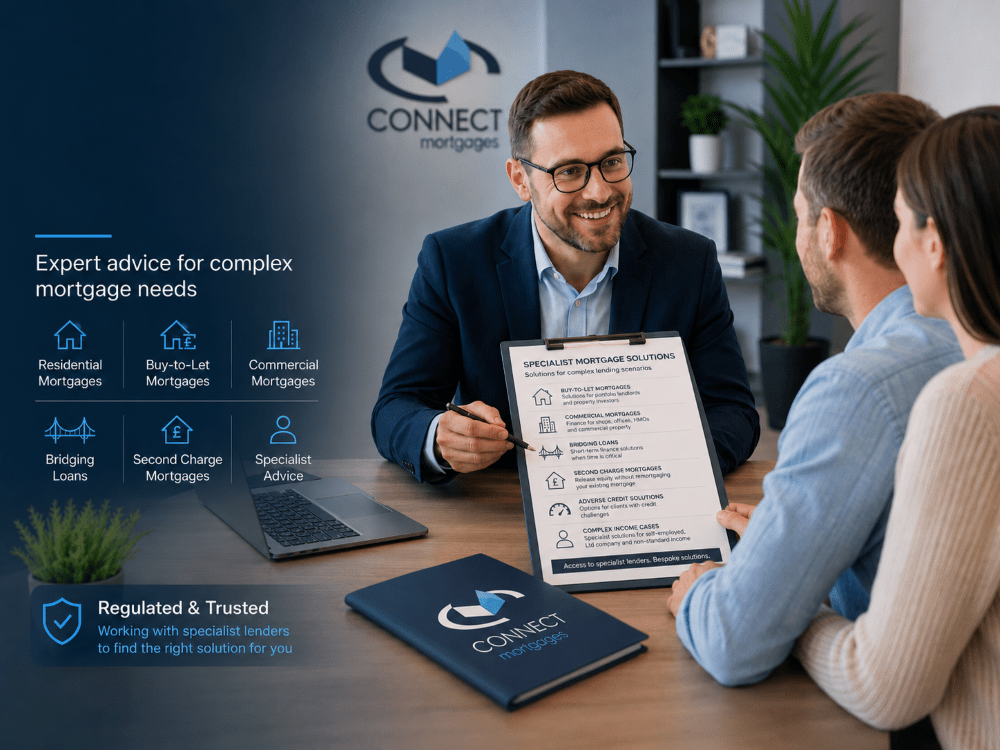

Connect Mortgages helps UK borrowers speak with advisers who understand residential, buy-to-let, commercial, bridging, second charge and other specialist mortgage areas.

What Does a Specialist Mortgage Broker Do?

A specialist mortgage broker can help when your mortgage needs do not fit standard lenders’ criteria.

This may include complex income, adverse credit, buy-to-let portfolios, commercial property, bridging finance, second charge borrowing, expat income, contractor income, or unusual property types.

The broker’s role is to review your circumstances, explain possible lender routes, help prepare your case, and guide you through the application process.

When Might You Need a Specialist Mortgage Broker?

You may need a specialist mortgage broker when your case needs more than a basic rate comparison.

This can happen when the lender needs extra evidence, a clearer explanation, or a more detailed view of affordability. It can also happen when the property, income, credit history, or purpose of borrowing requires a specialist lender.

Common examples include:

- Self-employed income.

- Contractor or freelancer income.

- Multiple income sources.

- Adverse credit.

- Recent credit issues.

- Buy-to-let portfolios.

- Limited company buy-to-let.

- Houses in multiple occupation.

- Semi-commercial property.

- Commercial property.

- Bridging finance.

- Development finance.

- Second charge mortgages.

- Expat or overseas income.

- Non-standard property types.

If your situation is not straightforward, it does not always mean a mortgage is out of reach. It means the advice process needs to be more detailed.

Why Specialist Mortgage Advice Matters

A standard mortgage search can miss important details.

A lender may assess your income, deposits, credit file, property type, age, business structure, rental income, or existing borrowing in different ways. Some lenders may decline a case quickly, while others may consider it with the right documents and explanation.

A specialist mortgage broker can help you understand:

- Which lenders may consider your case.

- What documents may be needed.

- How affordability could be assessed.

- Whether timing could affect the application.

- Which risks need to be considered.

- Whether another mortgage route may be more suitable.

Good advice should not only focus on whether you can borrow. It should also consider whether the mortgage is suitable and affordable.

Specialist Residential Mortgage Cases

Residential mortgage advice can become specialised when the borrower’s income, credit history, property type, or age does not fit standard criteria.

This may include first-time buyers with complex income, self-employed applicants, contractors, applicants with recent credit issues, or borrowers buying a property that needs extra lender review.

If your case still relates to your home, you may also want to read our guide to residential mortgage advice.

A specialist broker can help you prepare the facts before a lender reviews the application. This can reduce confusion and help you avoid unsuitable lender routes.

Specialist Buy-to-let Mortgage Brokers

Buy-to-let lending can become complex quickly.

A landlord may own several properties, borrow through a limited company, buy an HMO, refinance a portfolio, or use rental income in ways that require careful lender matching.

Connect Mortgages supports landlords and property investors with buy-to-let mortgage advice across different property and ownership structures.

Specialist buy-to-let advice may be useful if you are:

- Buying through a limited company.

- Managing several rental properties.

- Buying an HMO.

- Looking at a holiday let.

- Refinancing a rental property.

- Raising capital from an investment property.

- Buying a property with mixed-use elements.

A specialist broker can help you understand lender stress testing, rental income requirements, deposit expectations, and portfolio checks.

Commercial and Semi-Commercial Mortgage Brokers

Commercial mortgages are used for business premises, trading properties, investment properties, or properties with a commercial element.

A case may need specialist advice if the property includes retail, office, industrial, hospitality, mixed-use, or semi-commercial space. Lenders may review the business, lease, trading history, property value, deposit, and future plans.

For more details, visit our commercial mortgage page.

A specialist commercial mortgage broker can help explain which lender route may fit the property and borrowing purpose.

Bridging Finance and Short-term Lending

A bridging loan is usually used when timing matters.

This may include auction purchases, broken property chains, refurbishment projects, delayed sales, or situations where long-term finance is not ready in time.

Because bridging finance is short-term borrowing secured against property, it needs a clear exit plan. This means the borrower should understand how the loan will be repaid before proceeding.

Connect Mortgages provides guidance on bridging loans for property buyers, investors and homeowners who need short-term finance.

A specialist broker can help you review the purpose, term, security, costs, and exit route.

Second Charge Mortgage Brokers

A second charge mortgage allows a homeowner to borrow against equity while keeping the existing main mortgage in place.

This may be considered when remortgaging is not suitable, when early repayment charges apply, or when the current mortgage deal is worth keeping.

You can read more in our guide to second charge mortgages.

Second charge borrowing is secured against your home. Therefore, advice should consider affordability, repayment risk, the total cost of borrowing, and whether other options may be more suitable.

Specialist Mortgage Advice for Complex Income

Income can be more complex than a payslip.

Many borrowers earn income from a mix of salary, dividends, bonuses, commissions, overtime, contracts, rental income, pensions, or business profits. Some lenders may use this income differently.

A specialist mortgage broker can help package income evidence clearly. This may include accounts, tax calculations, payslips, contracts, bank statements, accountant references, or business documents.

This can be useful for:

- Self-employed applicants.

- Company directors.

- Contractors.

- Freelancers.

- Professionals with bonus income.

- Borrowers with several income sources.

- Landlords with rental income.

- Applicants returning from overseas.

The aim is not to force a case through. The aim is to understand which lenders may assess the income correctly.

Specialist Mortgage Advice for Credit issues

Credit history can affect lender choice.

Some lenders may consider missed payments, defaults, county court judgments, debt management plans, or discharged bankruptcies after a certain period. However, criteria differ between lenders.

A specialist mortgage broker can help review the timing, amount, reason, and current position before suggesting possible routes.

You should be honest about credit issues from the start. This gives the adviser a better chance of finding lenders that may fit the full picture.

What Information Should You Prepare?

Before speaking with a specialist mortgage broker, it helps to gather key details.

You may need:

- Proof of income.

- Bank statements.

- Credit report.

- Property details.

- Deposit details.

- Existing mortgage information.

- Rental income details.

- Business accounts.

- Tax documents.

- Details of current debts.

- Purpose of borrowing.

- Timescale for completion.

You do not need all the answers before your first conversation. However, accurate information helps the adviser assess the case properly.

How Connect Mortgages Can Help

Connect Mortgages helps borrowers access mortgage advice across a wide range of property finance areas.

Our advisers can help you understand whether your case may need a specialist lender, a standard lender, or a different route altogether. They can also explain the next steps before you make a full application.

If you want to compare advisers by location or specialist area, you can also use Connect Experts to find a specialist mortgage and protection broker.

You can also search for mortgage brokers in the UK to compare advisers by location, language, or mortgage type.

Specialist Mortgage Broker Checklist

Before choosing a broker, ask:

- Do they understand your type of mortgage need?

- Can they explain which documents lenders may request?

- Can they discuss more than one lender route?

- Will they explain fees before you proceed?

- Will they explain affordability and risk clearly?

- Are they clear about regulated and unregulated borrowing?

- Can they support you through the application process?

The right advice should make the process clearer. It should not make the decision feel rushed.

Speak to a specialist mortgage broker

If your mortgage case does not fit a standard lender route, it may still have options.

Connect Mortgages can help you understand your next steps, prepare your information, and speak with an adviser who specialises in mortgage cases.

Frequently asked questions

What is a specialist mortgage broker?

A specialist mortgage broker helps borrowers whose circumstances do not fit standard lender criteria. This may include complex income, adverse credit, buy-to-let portfolios, commercial property, bridging finance, or second charge mortgages.

Is a specialist mortgage broker different from a normal mortgage broker?

A specialist mortgage broker usually works with more complex cases. They may have experience with lenders that consider non-standard income, unusual property types, investor finance, or cases that need a more detailed explanation.

Can a specialist mortgage broker help if I am self-employed?

Yes, a specialist mortgage broker may help self-employed borrowers understand which lenders could consider their income. Lenders may review accounts, tax documents, business income, salary, dividends, or retained profits differently.

Can a specialist mortgage broker help with adverse credit?

A specialist mortgage broker may help if you have adverse credit. They can review the type, date, value, and current status of the issue before discussing possible lender routes.

Do specialist mortgage brokers work with buy-to-let investors?

Yes, specialist mortgage brokers often support landlords with portfolio buy-to-let, limited company buy-to-let, HMOs, holiday lets, and rental property refinancing.

Can I get specialist mortgage advice for commercial property?

Yes, specialist mortgage brokers can help with commercial and semi-commercial mortgage cases. These may include business premises, investment property, mixed-use buildings, offices, retail units, or trading premises.

Are bridging loans specialist mortgages?

Bridging loans are a specialist form of short-term property finance. They are usually used when timing, property condition, or funding structure does not fit a standard mortgage route.

Is a second charge mortgage specialist borrowing?

A second charge mortgage can be specialist borrowing because it sits behind your main mortgage. Advice should consider affordability, risk, term, purpose, and whether remortgaging may be more suitable.

Will using a specialist mortgage broker guarantee approval?

No broker can guarantee mortgage approval. A specialist mortgage broker can help you understand suitable routes, prepare your case, and approach lenders that may fit your circumstances.

How do I speak to a specialist mortgage broker?

You can contact Connect Mortgages to discuss your circumstances, or use Connect Experts to search for a mortgage adviser by location, language, gender, or area of expertise.