Specialist Mortgages UK: Not every mortgage application fits a standard lender checklist.

You may have strong income, but it may come from self-employment, contracts, dividends, rental property, overseas work or more than one source. You may have a good deposit, but your credit file may show missed payments, defaults or older financial issues. You may be buying a property that needs a lender with more flexible criteria.

This is where specialist mortgages may help.

A specialist mortgage is not one single product. It is a way of matching a borrower, property or borrowing purpose with lenders that can assess more detailed cases. The right route depends on your income, credit history, deposit, property type, repayment plan and future plans.

Connect Mortgages helps UK clients understand their options before they apply. We are a credit broker and not a lender. After assessing your needs, we can recommend lender options that may suit your circumstances.

What is a specialist mortgage?

A specialist mortgage may be suitable when your situation does not fit standard high-street criteria.

This may include:

- Self-employed income

- Company director income

- Contractor or freelancer income

- Credit issues

- Buy-to-let or portfolio landlord finance

- Limited company buy-to-let

- HMO or multi-unit property finance

- Bridging finance

- Second charge borrowing

- Large mortgage loans

- Non-standard property types

- Expat or foreign national borrowing

- Complex affordability

Lenders still assess affordability, income, credit conduct, deposit, property type and risk. The FCA sets rules and guidance around responsible lending and affordability assessment for regulated mortgage contracts.

A specialist mortgage adviser can help you understand which lenders may consider your case before you apply.

Why Some Mortgage Applications Need Specialist Advice

Many mortgage applications are straightforward. Others need more explanation.

A lender may want to understand how your income is earned, how stable it is and whether it can support the mortgage. This can be more detailed when income does not come from a basic salary.

A lender may also look closely at:

- How recent any credit issues were

- Whether debts have been settled

- How much deposit you have

- Your monthly commitments

- The property type

- The repayment method

- The purpose of the borrowing

- Your wider financial position

Specialist advice can help because lender criteria can vary. One lender may decline a case that another lender may consider.

Before applying, you may also want to check your borrowing position using our mortgage calculator.

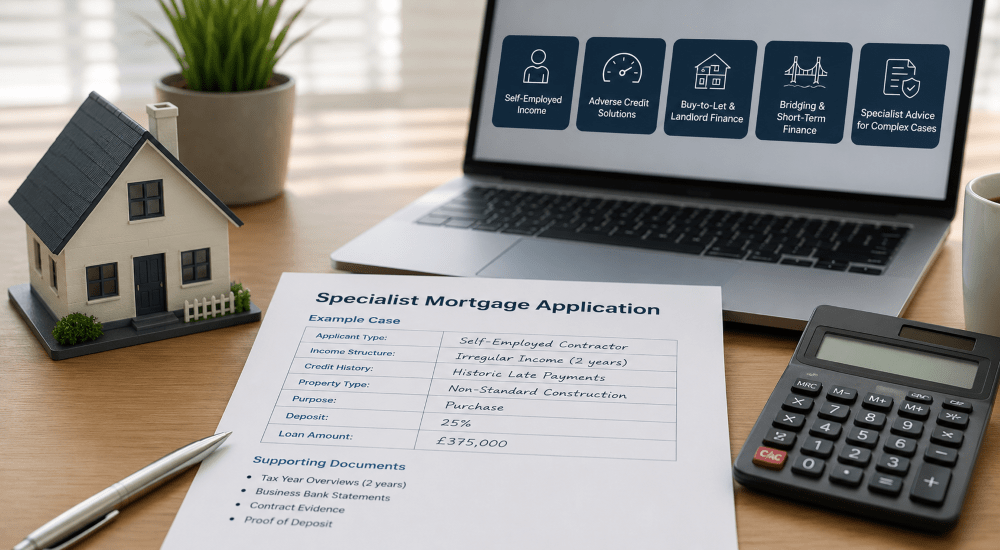

Self-Employed Specialist Mortgages

Self-employed applicants can get mortgages, but lenders may check income differently.

If you are employed, lenders may use payslips and a P60. If you are self-employed, lenders may ask for tax calculations, Tax Year Overviews, account statements, business bank statements, or accountant details.

This can apply if you are:

- A sole trader

- A freelancer

- A contractor

- A limited company director

- A business partner

- A CIS worker

- A shareholder with business income

Some lenders prefer two or more years of trading history. Others may consider shorter trading periods if the wider case is strong.

Connect Mortgages can help you prepare the right evidence before you apply. Read more about self-employed mortgage advice. You can also use Connect Experts to find a self-employed mortgage adviser by location, language and adviser preference.

Specialist Mortgages with Adverse Credit

Credit issues do not always stop someone from getting a mortgage. However, they can affect lender choice, deposit requirements, interest rates and the documents needed.

Adverse credit may include:

- Missed payments

- Defaults

- County Court Judgments

- Debt management plans

- Previous IVA

- Bankruptcy history

- High credit use

- Recent payday loan use

Lenders may look at what happened, when it happened, whether it has been settled and how your finances look now. MoneyHelper also explains that poor credit can affect mortgage options, but there may still be steps borrowers can take.

A specialist mortgage adviser can help you understand how your credit file may be viewed before you apply.

Read more about adverse credit mortgage advice. You can also search for a suitable adviser through the Residential Credit Issues Mortgage Adviser Search.

Specialist Buy-to-Let Mortgages

Buy-to-let mortgage cases can become specialist when the property, landlord profile or ownership structure needs closer review.

This may include:

- First-time landlords

- Portfolio landlords

- Limited company ownership

- HMO properties

- Multi-unit freehold blocks

- Holiday lets

- Expat landlords

- Non-UK resident landlords

- Higher-value rental property

- Remortgaging an existing rental property

Buy-to-let lenders usually assess rental income, property value, deposit, landlord experience, background income and the ownership structure. Portfolio landlord cases can involve more paperwork. The Bank of England’s PRA has set expectations for buy-to-let underwriting standards, including how lenders assess buy-to-let risk.

If you are buying an additional residential property in England or Northern Ireland, higher Stamp Duty Land Tax rates may apply. GOV.UK provides guidance on when these higher rates apply.

Read more about buy-to-let mortgage advice.

Limited company buy-to-let mortgages

Some landlords buy property through a limited company. This route may suit certain landlords, but it needs careful advice.

A limited company buy-to-let mortgage may involve:

- A special purpose vehicle

- Company bank statements

- Director and shareholder checks

- Personal guarantees

- Rental calculations

- Deposit requirements

- Tax planning

- Legal advice

A company structure is not right for every landlord. You should consider mortgage costs, tax, legal duties and future plans before deciding. Connect Mortgages can help you understand the mortgage side. You should also speak to a qualified tax adviser before making tax-led decisions.

Read more about limited company buy-to-let mortgages.

Specialist Mortgages For Non-Standard Property

Some properties need specialist lender review.

This may include:

- Listed buildings

- Thatched properties

- Timber-framed homes

- Flats above commercial premises

- Properties with short leases

- Homes with large acreage

- Ex-local authority flats

- New-build flats

- Mixed-use property

- Properties needing renovation

A lender may want to check whether the property is suitable security for the mortgage. The valuation, construction type, location and condition can all affect the decision.

A specialist mortgage adviser can help identify lenders that may consider the property before you spend time on the wrong route.

Bridging Finance and Short-Term Property Funding

Bridging finance is short-term borrowing. It may help when timing is the main issue.

It may be used for:

- Auction purchases

- Chain breaks

- Buying before selling

- Renovation before refinancing

- Business or investment property deadlines

- Short-term funding gaps

A bridging loan is not the same as a standard mortgage. It can be more expensive and usually needs a clear exit plan. The exit plan may be a sale, refinance or another confirmed repayment route.

Read more about bridging loan advice.

Second Charge Mortgages

A second charge mortgage is a loan secured against a property that already has a mortgage.

It may be considered when a borrower wants to raise funds without changing their current mortgage. This may be relevant if the existing mortgage has an early repayment charge or a favourable rate.

Second charge borrowing may be used for:

- Home improvements

- Debt consolidation

- Business purposes

- Property investment

- Family support

- Large one-off costs

Debt consolidation should be considered carefully. It may reduce monthly payments, but it can increase the total amount repaid over time.

Read more about second charge mortgage advice.

Large Mortgage Loans and Complex Income

Large mortgage loans often need more detailed underwriting.

This may apply where the borrower has:

- High income from several sources

- Bonus or commission income

- Dividend income

- Retained company profit

- Partnership income

- Investment income

- Rental income

- Overseas income

- Trust or family wealth arrangements

A lender may want to understand how reliable the income is and whether it can support the loan over the mortgage term.

Specialist advice can help present the case clearly and avoid applying to lenders that are unlikely to fit.

Expat and Foreign National Mortgage Cases

Some mortgage cases are more complex due to residency, visa status, overseas income, or foreign-currency income.

This may include:

- UK expats buying or refinancing UK property

- Foreign nationals buying in the UK

- Applicants with overseas income

- Applicants paid in foreign currency

- Non-UK resident landlords

- Applicants with limited UK credit history

Lenders may check residency, income source, deposit source, currency risk, visa status and UK credit history.

A specialist mortgage adviser can help explain which lenders may consider the application.

What Documents May Be Needed?

The documents needed depend on your situation.

You may be asked for:

- Proof of ID

- Proof of address

- Bank statements

- Payslips

- P60

- Tax calculations

- Tax Year Overviews

- Company accounts

- Accountant details

- Contract evidence

- Rental income details

- Property schedule

- Credit report

- Deposit evidence

- Existing mortgage statements

- Proof of repayment plan

- Insurance details, where relevant

Preparing documents early can reduce delays. It can also help your adviser understand which lender route may be suitable.

Why Protection Should Be Part of The Conversation

A specialist mortgage is still a long-term financial commitment.

If your income is variable, your household depends on one income, or your borrowing is large, protection planning may be important.

Protection may include:

- Life cover

- Critical illness cover

- Income protection

- Buildings insurance

- Contents insurance

- Landlord insurance

The right protection depends on your needs, budget and mortgage type.

Read more about mortgage protection insurance.

How Connect Mortgages Can Help

Connect Mortgages helps clients understand mortgage options across residential, buy-to-let, commercial finance and protection.

We can help you:

- Understand why your case may be specialist

- Review income and affordability evidence

- Check which lender routes may fit

- Prepare documents before application

- Compare suitable mortgage options

- Understand risks, fees and next steps

- Consider protection needs alongside borrowing

We are a credit broker and not a lender. A fee may be payable for arranging your mortgage. Your adviser will confirm any fee before you choose to proceed.

Find a Specialist Mortgage Adviser

Some clients want to choose an adviser based on location, language, gender or mortgage type.

Connect Experts is part of Connect Group and helps users search for mortgage advisers across the UK. It is a directory and matching platform. Mortgage advice is provided by the adviser or firm you choose.

You can find a specialist mortgage adviser through Connect Experts if you want to compare adviser profiles before making contact.

FAQs: Specialist Mortgages

What is a specialist mortgage?

A specialist mortgage is a mortgage route for borrowers, properties or borrowing needs that do not fit standard lender criteria. This may involve complex income, credit issues, buy-to-let finance, non-standard property or urgent funding.

Who may need a specialist mortgage?

You may need specialist mortgage advice if you are self-employed, a company director, a contractor, a landlord, an expat, a foreign national, or someone with credit issues. You may also need specialist advice if the property is unusual.

Can I get a mortgage if I am self-employed?

Yes, self-employed applicants can get mortgages. Lenders usually need clear income evidence, such as tax calculations, Tax Year Overviews, accounts or bank statements.

Can I get a mortgage with bad credit?

Bad credit does not always mean a mortgage is impossible. Lenders may consider the type of credit issue, how recent it was, whether it has been settled and your current affordability.

Are buy-to-let mortgages specialist mortgages?

Some buy-to-let mortgages are straightforward. Others become specialist when they involve portfolio landlords, limited company ownership, HMOs, holiday lets, expat landlords or unusual rental structures.

What is a portfolio landlord mortgage?

A portfolio landlord mortgage is usually relevant when a landlord owns several mortgaged buy-to-let properties. Lenders may ask for a property schedule, rental income details, mortgage balances and wider financial information.

Can I get a mortgage on a non-standard property?

It may be possible, but lender choice can be narrower. Non-standard construction, listed status, short leases, flats above commercial premises or unusual property layouts can affect lender appetite.

Is bridging finance a specialist mortgage?

Bridging finance is specialist short-term property finance. It is usually used when speed, timing or property condition makes a standard mortgage unsuitable at that point.

Do I need a specialist mortgage broker?

You may benefit from a specialist mortgage broker if your case needs more detailed lender criteria. A broker can help identify lenders that may consider your income, credit history, property type or borrowing purpose.

Will I pay more for a specialist mortgage?

You may pay more if the lender sees the case as higher risk. Rates, fees and deposit requirements depend on the lender, your circumstances and the product available at the time.

Does Connect Mortgages provide specialist mortgage advice?

Connect Mortgages can help clients explore specialist mortgage options across residential, buy-to-let, bridging, second charge and other property finance areas.

Important information

Your home or property may be repossessed if you do not keep up repayments on your mortgage or loans secured on it.

Connect Mortgages is a trading style of Connect IFA Ltd, which is authorised and regulated by the Financial Conduct Authority.

The FCA does not regulate some forms of buy-to-let, commercial mortgage and bridging finance.

A fee may be payable for arranging your mortgage. Your adviser will confirm the amount before you choose to proceed.

We are a credit broker and not a lender. We have access to an extensive range of lenders. Once we have assessed your needs, we will recommend lender options that may suit your circumstances. You are not obliged to take our advice or recommendation.