What Is Available to First-Time Buyers? Buying a first home is rarely just about finding a property.

It is also about understanding the route into ownership. Some buyers have savings. Some have family support. Some need a lower deposit option. Others may need a scheme that helps reduce the cost of buying.

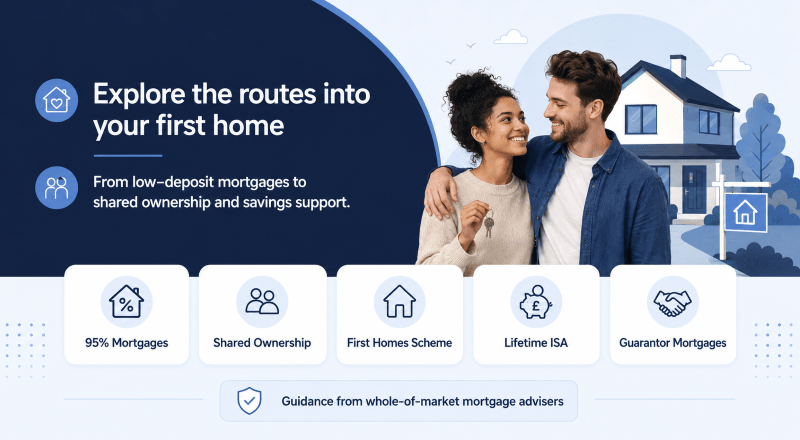

In July 2024, first-time buyers had several possible routes to consider. These included 95% mortgages, the Mortgage Guarantee Scheme, Lifetime ISAs, shared ownership, the First Homes Scheme and guarantor mortgage options.

However, availability did not mean automatic approval. Each route still depended on income, deposit, credit history, property type and lender criteria.

What is Available to First-Time Buyers?

First-time buyers in 2024 could consider several options:

| Option | What it could help with |

|---|---|

| 95% mortgages | Buying with a 5% deposit, subject to lender approval |

| Mortgage Guarantee Scheme | Supporting availability of some 95% mortgages |

| Labour’s proposed Freedom to Buy | A proposed permanent support route for low-deposit buyers |

| Lifetime ISA | Saving towards a first home with a government bonus |

| Shared ownership | Buying part of a property and paying rent on the remaining share |

| First Homes Scheme | Buying selected new-build homes at a discount |

| Guarantor mortgages | Using family support to strengthen an application |

The right option depended on the buyer’s circumstances. A scheme could help with access, but it could not replace affordability checks.

Why Awareness Mattered in 2024

In 2024, many first-time buyers were still unaware of the support that might be available.

That matters because a buyer who only looks at standard mortgages may miss a route that fits their deposit, income or family situation.

At the same time, no scheme should be viewed as a shortcut. A mortgage is a long-term commitment. The question is not only “Can I buy?” It is also “Can I sustain the payments?”

That is why first-time buyers should start with affordability, deposit position and likely monthly costs before choosing a scheme.

You can begin with the First-Time Buyer Mortgage guide for a broader overview of deposits, credit checks, and the mortgage process.

95% Mortgages and the Mortgage Guarantee Scheme

A 95% mortgage allows a buyer to purchase with a 5% deposit, subject to lender criteria.

For example, a buyer purchasing a property for £250,000 may need a £12,500 deposit. The remaining £237,500 would be covered by the mortgage, if approved.

In 2024, the Mortgage Guarantee Scheme was designed to support the availability of some 95% loan-to-value mortgages. It gave participating lenders a government guarantee on part of the loan risk.

However, the scheme did not remove the need for checks. Lenders still assessed:

- income

- credit history

- debts

- monthly commitments

- deposit source

- property type

- mortgage term

- future payment risk

A 5% deposit can help some buyers enter the market sooner. However, it can also mean higher monthly payments than with a larger deposit. It may also limit the number of available mortgage products. Before applying, buyers should check how much they can borrow using the Residential Affordability Calculator.

Labour’s Proposed Freedom to Buy Plan

After the July 2024 general election, Labour’s proposed Freedom to Buy plan became an important topic for first-time buyers.

At that point, the plan was expected to either replace or continue the Mortgage Guarantee Scheme. Its aim was to support buyers who could afford mortgage payments but struggled to build a large deposit.

The idea was simple in principle. If lenders had more confidence in offering lower-deposit mortgages, more first-time buyers could have access to the market.

However, first-time buyers still needed to be cautious. A government-backed route does not guarantee cheaper borrowing. It also does not guarantee acceptance.

The practical checks remained the same:

- Is the monthly payment affordable?

- Is the deposit enough?

- Does the property meet lender rules?

- Is the credit profile suitable?

- Is the mortgage term realistic?

- Would payments still be manageable if costs rose?

Freedom to Buy was therefore relevant, but it should not be viewed alone. It sat alongside wider issues such as housing supply, affordability and lender confidence.

Lifetime ISA for First-Time Buyers

A Lifetime ISA can help some first-time buyers save towards a first home.

Eligible savers can pay in up to £4,000 each tax year. The government then adds a 25% bonus, up to £1,000 per year. This can make the Lifetime ISA useful for buyers who are still building their deposit.

However, the rules matter. Buyers should check the property price limit, withdrawal rules and timing before relying on the bonus.

This is important because a Lifetime ISA is not simply a savings account. It is a product with conditions. Used correctly, it can help. Used without planning, it can create delays or costs.

Shared Ownership

Shared ownership can help buyers who cannot yet afford to buy a full property.

Under shared ownership, a buyer purchases a share of the home and pays rent on the remaining share. Over time, they may be able to buy more shares. This is often called staircasing.

The main benefit is that the deposit and mortgage may be based on the share being bought, not the full property value.

However, buyers should also review:

- rent on the unsold share

- service charges

- lease terms

- staircasing costs

- resale restrictions

- lender availability

Shared ownership can be useful, but it is not suitable for every buyer. The total monthly cost matters more than the headline deposit.

First Homes Scheme

The First Homes Scheme was created to help eligible first-time buyers purchase selected new-build homes at a discount.

The discount is usually at least 30% below market value. In some areas, the discount may be higher. Local rules can also apply, especially where councils prioritise key workers or local residents.

The main advantage is that the lower purchase price may reduce the deposit and mortgage needed.

However, availability can be limited. Buyers may also need to meet income, local connection and property rules.

This means the First Homes Scheme should be checked early. It may be useful, but only where qualifying properties are available.

Guarantor and Family-Supported Mortgages

Some first-time buyers receive help from family.

This may include a gifted deposit, savings support, a family deposit arrangement or a guarantor-style mortgage. The structure depends on the lender and the family’s circumstances.

A guarantor mortgage may involve another person supporting the application. In some cases, family savings or property may help reduce lender risk.

However, family-supported mortgages need careful advice. The person helping the buyer may take on financial responsibility. They may also place savings or property at risk.

Before using family support, everyone involved should understand the legal and financial impact.

What Should First-Time Buyers Check First?

First-time buyers should avoid choosing a scheme before checking affordability.

A better order is:

- Work out the deposit available.

- Check income and monthly commitments.

- Review credit history.

- Estimate monthly repayments.

- Consider the property type and location.

- Compare suitable schemes.

- Speak to a mortgage adviser before applying.

You can use the Mortgage Calculators page to estimate repayments, affordability and other buying costs.

This helps turn a broad idea into a practical budget.

Why Mortgage Advice Can Help

First-time buyers often face too much information at once.

There may be schemes, lender rules, product types, legal steps, affordability checks and property risks. Each part can affect the next.

A mortgage adviser can help compare options and explain which routes may fit your circumstances. They can also help you understand why one lender may assess your income differently from another.

If you want to choose an adviser by location, language, or preference, you can search for first-time-buyer mortgage advisers through Connect Experts.

Connect Experts is part of the Connect Group. It is a mortgage adviser directory and matching platform. Advice is provided by the adviser or firm you choose.

Frequently Asked Questions

What was available to first-time buyers in 2024?

First-time buyers could consider 95% mortgages, the Mortgage Guarantee Scheme, Lifetime ISAs, shared ownership, First Homes and family-supported mortgage options. Availability depended on eligibility, lender criteria and property type.

Could first-time buyers buy with a 5% deposit?

Some first-time buyers could buy with a 5% deposit using a 95% loan-to-value mortgage. Approval still depended on affordability, credit history, income and the property being purchased.

Was Freedom to Buy available in July 2024?

In July 2024, Freedom to Buy was a Labour proposal. It was expected to support lower-deposit mortgage access, but buyers still needed to check current lender and scheme rules before relying on it.

Is shared ownership better than a 95% mortgage?

Not always. Shared ownership may reduce the mortgage needed, but buyers also pay rent on the remaining share. A 95% mortgage may give full ownership, but repayments may be higher. The better route depends on total cost and long-term plans.

Can a Lifetime ISA help with a first home?

Yes, a Lifetime ISA can help eligible first-time buyers save towards a deposit. The government bonus can support savings, but buyers must follow the product rules.