HMO vs Buy-to-Let: Mortgage: A rental property is judged not only by the rent it can produce.

It is judged by how it is lived in, how it is financed, how it is managed, and how much risk sits behind the income.

That is why the choice between an HMO and a standard buy-to-let matters. Both can be part of a landlord strategy. However, they are not the same product, and lenders do not always treat them in the same way.

A standard buy-to-let is usually simpler. An HMO can offer higher rental income, but it often brings more rules, more documents, more management and more lender checks.

This guide compares HMO vs buy-to-let from a mortgage, property and landlord perspective.

HMO vs Buy-to-Let

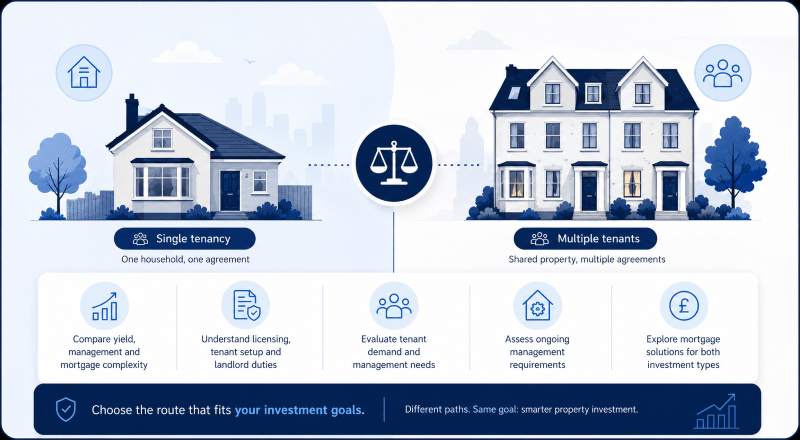

A buy-to-let usually means one property let to one household under one tenancy.

An HMO, or House in Multiple Occupation, usually means a property rented by at least three people from more than one household who share facilities.

For landlords, the key difference is not only rental income. It is the structure behind the income.

- Buy-to-let may suit landlords who want a simpler rental model.

- HMO may suit landlords who can manage higher compliance and tenant turnover.

- Buy-to-let mortgages are usually available from more lenders.

- HMO mortgages often need specialist lender criteria.

- HMO properties may need licensing, fire safety upgrades and room-size checks.

- Rental income for HMOs may be assessed differently by lenders.

- A higher rent does not always mean a better investment.

If you want a wider view of landlord finance, read our Buy-to-Let Mortgage guide.

What Is a Buy-to-Let Property?

A buy-to-let property is usually a residential property bought or refinanced for rental purposes.

In most standard cases, one household rents the whole property. This could be a family, a couple, or a group of tenants under one tenancy agreement.

The landlord receives one rent for the property. The lender usually assesses the expected rental income, deposit, property type, ownership structure and wider financial position.

A standard buy-to-let may involve:

- One household

- One tenancy

- One monthly rental figure

- Fewer specialist property checks

- Wider lender availability

- More straightforward management

This does not mean buy-to-let is simple in every case. Limited company ownership, portfolio lending, tax planning and rental stress tests can all affect the mortgage route.

However, compared with HMOs, standard buy-to-let is often the cleaner starting point.

What Is an HMO?

An HMO stands for House in Multiple Occupation.

GOV.UK describes an HMO as a property rented by at least three people who are not from one household and who share facilities such as a bathroom or kitchen.

In practical terms, an HMO is often a shared rental property. Tenants may rent rooms separately while sharing parts of the home.

Common examples include:

- Student houses

- Professional house shares

- Co-living properties

- Converted houses let by the room

- Larger shared homes with five or more tenants

An HMO is not just a standard buy-to-let with more people inside it. The occupation structure changes the mortgage, compliance and management picture.

For more detail on this property type, read our HMO Property guide.

HMO vs Buy-to-Let: The Main Difference

The main difference is how the property is occupied.

A standard buy-to-let is usually let to one household. An HMO is let to multiple people who form separate households and share facilities.

That difference affects:

- Mortgage criteria

- Rental assessment

- Valuation method

- Licensing

- Fire safety

- Management duties

- Tenant turnover

- Insurance

- Exit strategy

A landlord should not choose between them based on rent alone. The better question is whether the property, finance and management model fit the landlord’s plan.

HMO vs Buy-to-Let Comparison Table

| Area | Standard Buy-to-Let | HMO |

|---|---|---|

| Tenant structure | Usually one household | Multiple unrelated tenants |

| Rent model | One rent for the whole property | Rent may be charged per room |

| Mortgage access | Wider lender choice | More specialist lender choice |

| Rental assessment | Often based on one tenancy figure | May use room-by-room rent |

| Deposit | Can vary by lender and case | Often higher due to specialist risk |

| Management | Usually simpler | Usually more active |

| Licensing | Often not required | May be required |

| Fire safety | Standard landlord duties apply | Extra checks may apply |

| Valuation | Standard investment basis | May need specialist assessment |

| Landlord experience | Some lenders accept new landlords | Some lenders prefer experience |

| Tenant turnover | Often lower | Often higher |

| Running costs | Usually lower | Often higher |

| Potential yield | Often moderate | Often higher, but not guaranteed |

Mortgage Differences Between HMO and Buy-to-Let

The mortgage difference is one of the most important parts of the decision.

A lender wants to know what it is lending against. With a standard buy-to-let, that usually means a property let to one household. With an HMO, the lender may need to understand the room layout, tenant numbers, licence position, management plan and local rental demand.

Standard Buy-to-Let Mortgage Checks

A lender may review:

- Property value

- Expected rental income

- Deposit size

- Loan-to-value

- Applicant income

- Credit profile

- Ownership structure

- Existing property portfolio

- Tenancy type

- Personal or limited company ownership

HMO Mortgage Checks

An HMO lender may also review:

- Number of lettable rooms

- Number of tenants

- Shared facilities

- Room-by-room rental income

- HMO licence position

- Fire safety standards

- Planning position

- Landlord experience

- Property condition

- Local shared housing demand

- Management arrangements

- Valuation approach

This is why an HMO mortgage can take more preparation. The lender is not only testing the rent. It is also testing how the property works.

Rental Income: Higher Rent Does Not Remove Higher Risk

HMOs can produce more rental income than a standard single-let property.

That is the main attraction. Several tenants may pay rent separately, which can increase the total monthly income from one building.

However, higher income can come with higher movement.

An HMO may involve:

- More tenant changes

- More maintenance

- More utility usage

- More wear and tear

- More compliance work

- More management time

- More void risk by room

- Higher setup costs

A standard buy-to-let may produce lower rent, but it may also have a simpler structure. One household may stay longer and create fewer operational demands.

The question is not only “which earns more?”

The better question is “which income is more durable after costs, time and risk?”

Licensing and Local Council Rules

HMO licensing is one of the biggest practical differences.

GOV.UK states that a large HMO in England or Wales needs a licence if:

- It is rented to five or more people.

- Those people form more than one household.

- Some or all tenants share toilet, bathroom or kitchen facilities.

- At least one tenant pays rent, or their employer pays it.

Smaller HMOs may also need a licence depending on local council rules. Landlords should check with the relevant council before buying, converting or letting an HMO.

You can check the official position on the GOV.UK HMO licence page.

A licence may also include conditions around property suitability, smoke alarms, gas safety, electrical safety and facilities.

This matters for mortgage purposes because a lender may ask whether the property has the correct licence. If the property does not meet local rules, the mortgage route may be affected.

Room Sizes, Safety and Property Standards

An HMO must work as a home, not just as an income model.

Room sizes, facilities and safety standards matter. A property that looks profitable on a spreadsheet may still fail if the rooms, layout or facilities are not suitable.

Landlords may need to consider:

- Bedroom sizes

- Shared kitchen space

- Bathroom access

- Fire doors

- Smoke alarms

- Escape routes

- Electrical safety

- Gas safety

- Waste storage

- General property condition

These checks can affect both the licence and the mortgage. They can also affect whether tenants want to live there.

The practical truth is simple. Higher density needs better control.

Valuation Differences

A standard buy-to-let is often valued as a rental property let to one household.

An HMO may be assessed differently, depending on the property, lender and valuer. Some lenders may use a bricks-and-mortar valuation. Others may consider investment value or rental yield in more detail.

The valuation approach can affect:

- Maximum loan size

- Deposit required

- Refinance options

- Exit strategy

- Future sale market

- Lender appetite

This is important because not every buyer wants an HMO. The exit market may be narrower than for a standard family rental property.

A landlord should therefore think beyond the first mortgage offer. The future refinance or sale may matter just as much.

Management Differences

Buy-to-let and HMO ownership feel different in day-to-day life.

A standard buy-to-let may involve one tenant relationship. There may be fewer calls, fewer moving parts and fewer shared-space issues.

An HMO may involve several tenant relationships at once. Even when rooms are let separately, the property must still operate as one home.

An HMO landlord may need to manage:

- Room advertising

- Tenant checks

- More frequent move-ins

- Shared-space cleaning

- Repairs in communal areas

- Utility arrangements

- Waste management

- Neighbour concerns

- Licence conditions

Some landlords use managing agents. Others manage the property themselves. Either way, the time and cost should be included in the investment plan.

Costs to Compare Before Choosing

The wrong comparison is gross rent against gross rent.

The better comparison is net return after realistic costs.

Before choosing between HMO and buy-to-let, compare:

- Purchase price

- Deposit

- Mortgage rate

- Valuation fees

- Legal fees

- Licence fees

- Planning costs

- Refurbishment costs

- Fire safety upgrades

- Furniture costs

- Insurance

- Utilities

- Management fees

- Maintenance

- Void periods

- Accountant fees

- Tax position

You can use our Buy-to-Let Affordability Calculator to estimate how rent may support borrowing.

A calculator is only a guide. A lender’s final view will depend on the full case.

Limited Company Ownership

Some landlords buy rental property through a limited company.

This can apply to both standard buy-to-let and HMO properties. However, limited company HMO lending may be more specialist.

A lender may review:

- Company structure

- SIC code

- Directors

- Shareholders

- Personal guarantees

- Deposit source

- Existing company borrowing

- Rental income

- Wider portfolio details

Tax advice should come from a qualified tax adviser or accountant. Mortgage advice should focus on lender criteria, affordability, property type and borrowing route.

For more on this structure, read our Limited Company Buy-to-Let Mortgages guide.

Insurance Considerations

Insurance should match how the property is used.

A standard landlord insurance policy may not be suitable for every HMO. Shared occupation, multiple tenants and higher use of communal areas can change the risk.

Landlords may need to consider:

- Buildings insurance

- Contents insurance

- Landlord liability

- Rent guarantee options

- Legal expenses cover

- HMO-specific cover where required

The policy should reflect the actual letting arrangement. If the property is used as an HMO, that should be clear to the insurer.

Read more about Landlord Insurance to understand the protection aspect.

Who Might Prefer a Standard Buy-to-Let?

A standard buy-to-let may suit landlords who want a simpler route into property investment.

It may be worth considering if:

- You are a first-time landlord.

- You want fewer compliance steps.

- You prefer one tenancy.

- You want wider lender choice.

- You have limited time for active management.

- You want a property with a broader resale market.

- You prefer a lower operational workload.

This does not make buy-to-let risk-free. It simply means the structure is often easier to understand and manage.

Who Might Prefer an HMO?

An HMO may suit landlords who are prepared for a more active investment.

It may be worth considering if:

- You understand shared housing demand.

- You can manage more tenants.

- You have funds for setup costs.

- You can meet licensing rules.

- You are comfortable with specialist lender checks.

- You want to increase rental income from one property.

- You have a clear management plan.

An HMO is not only a property decision. It is an operating model.

The landlord is not just collecting rent. They are running a shared living environment.

HMO vs Buy-to-Let: Which Is Better?

Neither is automatically better.

A buy-to-let can be better for simplicity, lender access and long-term tenant stability.

An HMO can be better for higher rental income, but only when the costs, compliance and management work are understood.

The right answer depends on:

- Your experience

- Your deposit

- The property

- The local rental market

- Council rules

- Lender criteria

- Management time

- Exit strategy

- Risk tolerance

- Long-term plans

A property strategy should not be built around one number. It should be built around how the whole structure holds together.

Speak to a Mortgage Adviser Before You Decide

Before choosing between an HMO and buy-to-let, speak to a mortgage adviser who understands landlord lending.

The right adviser can help you compare:

- Standard buy-to-let mortgage options

- HMO mortgage options

- Rental assessment methods

- Deposit requirements

- Limited company lending

- Portfolio landlord rules

- Remortgage options

- Lender documents

- Likely case challenges

If you want to compare advisers with HMO experience, you can use Connect Experts to find HMO Mortgage Brokers UK.

FAQs: HMO vs Buy-to-Let

What is the difference between an HMO and a buy-to-let?

A buy-to-let is usually rented to one household. An HMO is rented to multiple people from different households who share facilities.

Is an HMO still a buy-to-let?

Yes, an HMO can be a type of buy-to-let investment. However, it is usually treated differently by lenders because of the shared occupation structure.

Do I need a special mortgage for an HMO?

You may need an HMO mortgage if the property is let to multiple unrelated tenants. A standard buy-to-let mortgage may not allow HMO use.

Is an HMO mortgage harder to get?

It can be more detailed. Lenders may review licensing, room layout, landlord experience, rental income and property management.

Does every HMO need a licence?

Not every HMO needs a mandatory licence. However, large HMOs usually do, and smaller HMOs may need a licence under local council rules.

Can a first-time landlord buy an HMO?

Some lenders may consider first-time landlords. Others prefer HMO or buy-to-let experience. The answer depends on the lender and property.

Are HMO mortgages more expensive?

They can be more specialist, so rates, fees and deposit requirements may differ from standard buy-to-let mortgages.

Do HMOs produce higher rental income?

HMOs may produce higher total rent because rooms can be let separately. However, costs and management demands may also be higher.

Is buy-to-let safer than HMO?

Not always. Buy-to-let may be simpler, but all rental property carries risk. HMO risk is often more operational and compliance-led.

Should I choose HMO or buy-to-let?

Choose based on the property, local demand, licence position, mortgage criteria, costs, management time and exit plan.