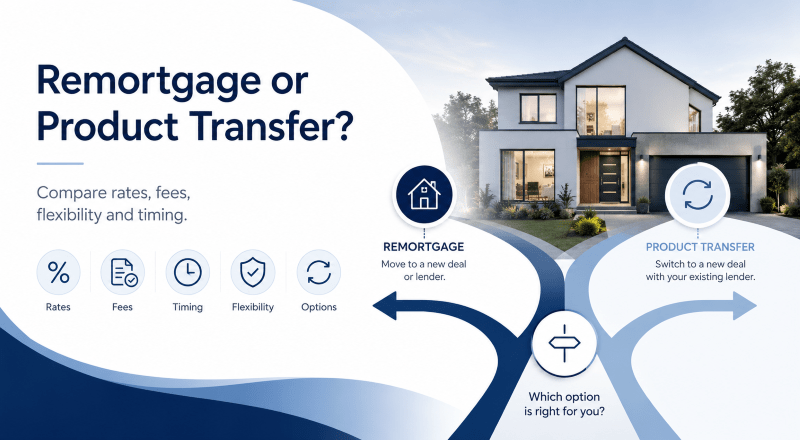

Remortgage or Product Transfer? Which Route Fits? A mortgage review is not only about finding a new rate.

It is about deciding whether to stay where you are or move because your needs have changed. That choice can shape your monthly payments, fees, paperwork, lender checks and future flexibility.

When your current mortgage deal is ending, two routes usually appear. You may be able to complete a product transfer with your current lender. You may also be able to remortgage, often by moving to a new lender.

Both can be useful. However, they work in different ways.

Remortgage or Product Transfer?

A product transfer may suit you if you want a simpler switch with your current lender. It may involve less paperwork, fewer checks and no legal work.

A remortgage may suit you if another lender offers a more suitable deal. It may also help if you want to borrow more, change the term, review your loan-to-value or change your mortgage structure.

The right route depends on the total cost, not just the interest rate. Fees, early repayment charges, affordability, valuation, legal work and timing all matter.

You can also read our wider remortgage advice page if you want broader guidance before comparing both routes.

What is a Product Transfer?

A product transfer means switching to a new mortgage product with your current lender.

You are not usually moving the mortgage to a new bank or building society. Instead, your existing lender offers you a new rate from its own product range.

This may be a fixed rate, tracker rate or another available product. The options depend on your lender, mortgage balance, loan-to-value and current criteria.

A product transfer is often used when:

- Your fixed rate is ending.

- You want to avoid moving onto the lender’s Standard Variable Rate.

- You do not need to borrow more.

- You want a simpler process.

- Your income or credit position has changed.

- Your current lender has a suitable new rate.

The appeal is practical. Sometimes the quietest route is the most useful route.

What is a Remortgage?

A remortgage usually means replacing your current mortgage with a new mortgage.

This often involves moving to a new lender. The new mortgage pays off your existing mortgage, and the new lender then takes over the loan.

A remortgage can involve more checks than a product transfer. The new lender will usually assess your income, outgoings, credit profile, property value and loan-to-value.

A remortgage may be considered when:

- Another lender may offer a more suitable deal.

- You want to borrow more.

- You want to change the mortgage term.

- You want to move from interest-only to repayment.

- You want to review the wider market.

- Your current lender has limited options.

- Your property value has changed.

- Your mortgage needs no longer fit your current lender.

A remortgage is not always better. It is simply a wider review.

Product Transfer vs Remortgage: Key Differences

| Area | Product Transfer | Remortgage |

|---|---|---|

| Lender | Same lender | Often a new lender |

| Product choice | Limited to current lender’s range | Wider market review may be possible |

| Affordability checks | May be lighter on a like-for-like switch | Usually a full affordability assessment |

| Credit checks | May be limited, depending on lender | Usually required |

| Valuation | Often not needed | Usually required, though some lenders use automated valuation |

| Legal work | Usually not required | Usually required |

| Fees | May be lower | May include arrangement, legal or valuation costs |

| Speed | Often quicker | Usually takes longer |

| Borrowing more | May be limited | May give more options |

| Complex changes | May not be suitable | May allow more structural changes |

The best choice is rarely found in one column. It is found by comparing the whole cost and the whole purpose.

Why the Cheapest Rate Is Not Always the Best Route

A low rate can look attractive, but the rate is only one part of the decision.

You should also consider:

- Arrangement fees.

- Early repayment charges.

- Valuation fees.

- Legal costs.

- Cashback.

- Product incentives.

- Monthly payment.

- Total amount repayable.

- Mortgage term.

- Whether fees are paid upfront or added to the loan.

Adding fees to the mortgage can reduce upfront cost. However, it may increase the total amount repaid over time.

That is why a mortgage review should compare the real cost, not just the headline rate.

You can use our mortgage calculators to estimate how different rates and terms may affect monthly payments.

When a Product Transfer May Make Sense

A product transfer may be worth considering when your current lender offers a suitable new deal.

It may be useful if you want to act quickly, avoid extra paperwork or reduce the risk of moving onto a higher reversion rate.

It may also help if your circumstances have changed since your last mortgage. For example, your income may have reduced, your job may have changed, or your credit file may not be as strong as before.

In some cases, a new lender may not assess the case as favourably. A product transfer may then provide a practical route, especially when no extra borrowing is needed.

A product transfer may suit you if:

- You are happy with your current lender.

- The new rate is competitive after fees.

- You do not need major changes.

- You want a quicker process.

- You want to avoid legal work.

- Your circumstances may make a new application harder.

- You mainly want to avoid the Standard Variable Rate.

Simple does not always mean basic. Sometimes it means suitable.

When a Remortgage May Make Sense

A remortgage may be useful when your current lender cannot offer what you need.

This may happen if you want to raise extra funds, change the mortgage term or access a more suitable product elsewhere.

A remortgage may also help if your property value has increased. A lower loan-to-value could place you in a different pricing band, depending on lender criteria.

A remortgage may suit you if:

- Another lender may offer a better overall cost.

- You want to borrow more.

- You want to reduce or extend the mortgage term.

- You want to change repayment type.

- Your current lender’s options are limited.

- You want to compare the wider market.

- You need a lender that better understands your income.

- You want to review the structure of your mortgage.

If you are unsure how much you may be able to borrow, our residential affordability calculator can help you start the review.

Timing: When Should You Start Reviewing?

Many homeowners start reviewing their mortgage several months before their current deal ends.

This gives time to compare your current lender’s product transfer options with wider remortgage choices. It may also help you avoid rushing into a decision near the end of your rate.

Timing matters because early repayment charges may apply if you leave your existing deal too soon. However, waiting too long may leave you exposed to your lender’s Standard Variable Rate.

A sensible review should check:

- The date your current deal ends.

- Any early repayment charge period.

- Your current mortgage balance.

- Your current lender’s product transfer window.

- Whether another lender can issue an offer in time.

- Whether the new deal can complete after your current tie-in ends.

The aim is not to move quickly. The aim is to move at the right time.

What Lenders May Check on a Remortgage

A remortgage is a new mortgage application. Therefore, lenders usually complete a full assessment.

They may review:

- Income.

- Outgoings.

- Credit commitments.

- Credit history.

- Employment status.

- Self-employed income.

- Bonus, overtime or commission.

- Childcare costs.

- Property value.

- Mortgage balance.

- Loan-to-value.

- Mortgage term.

- Reason for extra borrowing.

If your circumstances have changed, lender choice can matter.

For example, a borrower who became self-employed may need a lender that accepts their income evidence. A borrower with recent credit issues may need a different route.

You can read more on our adverse credit mortgage advice page if your credit file has changed.

What Checks May Apply on a Product Transfer?

A product transfer can be lighter than a remortgage, especially where the change is like-for-like.

However, this depends on the lender and the type of change requested.

A straightforward rate switch may involve fewer checks. A product transfer with extra borrowing, term changes or other material changes may need more assessment.

You should check whether the lender needs:

- Updated income details.

- A new affordability check.

- A credit check.

- A property valuation.

- Evidence for extra borrowing.

- Consent from all borrowers.

A product transfer is not always automatic. It is still a mortgage decision.

Borrowing More: Product Transfer or Remortgage?

If you want to borrow more, the answer becomes more technical.

Your current lender may offer a further advance. This is extra borrowing with the same lender. It may sit alongside your existing mortgage or form part of a new arrangement.

A remortgage may also allow extra borrowing. This could be used for home improvements, family support or another accepted purpose.

Lenders will consider affordability, loan-to-value and the reason for borrowing.

You should also consider whether a second charge mortgage could be suitable if changing your main mortgage is not the right route.

Extra borrowing increases the debt secured against your home. You should take advice before making that decision.

Debt Consolidation: A Careful Decision

Some homeowners review their mortgage because they want to consolidate unsecured debts.

This can reduce monthly payments in some cases. However, it may increase the total amount repaid if the debt is spread over a longer mortgage term.

It may also turn unsecured borrowing into debt secured against your home.

Debt consolidation should be assessed carefully. The lowest monthly payment is not always the lowest cost.

Product Transfer or Remortgage: Practical Decision Guide

Ask these questions before deciding:

| Question | Why it matters |

|---|---|

| Is my current lender’s rate competitive? | A product transfer may be practical if the total cost is close. |

| Do I need to borrow more? | A remortgage or further advance may need full assessment. |

| Has my income changed? | A new lender may assess affordability differently. |

| Has my credit file changed? | A product transfer may be easier in some cases. |

| Has my property value increased? | A lower loan-to-value may improve available options. |

| Are there early repayment charges? | Moving too soon can be costly. |

| Do I need legal work? | A remortgage usually needs legal involvement. |

| Do I want speed or wider choice? | Product transfers are often simpler, while remortgages may offer broader options. |

The right answer sits where cost, criteria and timing meet.

Why Advice Can Help

You can contact your current lender directly for product transfer options.

However, a mortgage adviser can help you compare those options against the wider market. They can also explain whether a remortgage, product transfer, further advance or second charge route may be more suitable.

This can help when:

- Your current deal is ending.

- You want to compare total costs.

- Your income is complex.

- Your credit profile has changed.

- You want to borrow more.

- You are unsure about fees.

- You want someone to manage the application.

Connect Mortgages is a credit broker, not a lender. Our advisers review your circumstances before discussing suitable mortgage options.

If you want to search by mortgage type and adviser preference, you can use Connect Experts to find a residential adviser for a rate review.

Current Market Context

UK Finance forecast that 1.8 million fixed-rate mortgages will come to an end in 2026. It also forecast growth in both external remortgaging and product transfers.

That does not mean every homeowner should switch lender. It means more borrowers may need to make a clear decision before their current deal ends.

MoneyHelper also explains that remortgaging may reduce mortgage costs, but borrowers should check whether it is the right move before switching.

You can read more from MoneyHelper’s remortgaging guide and the UK Finance mortgage market forecasts.

Protecting the Mortgage Decision

A mortgage review can also be a useful time to review protection.

Your mortgage balance, term, income, family position or monthly commitments may have changed since the last review.

You may want to consider:

- Life insurance.

- Critical illness cover.

- Income protection.

- Buildings insurance.

- Contents insurance.

Protection is not only about the mortgage. It is about the people who depend on the home remaining secure.

You can read more about mortgage protection insurance before reviewing your wider needs.

Find Mortgage Advice Near You

Some people prefer a local adviser. Others are happy with telephone or video advice.

What matters most is that the adviser can explain the options clearly, compare the practical costs and help you understand what each route means.

If location matters to you, Connect Experts lets you find a mortgage adviser by location.

FAQs: Remortgage or Product Transfer

Is a product transfer the same as a remortgage?

No. A product transfer usually means switching to a new deal with your current lender. A remortgage usually means replacing your mortgage, often by moving to a new lender.

Is a product transfer cheaper than a remortgage?

It can be cheaper, but not always. A product transfer may have fewer fees. However, a remortgage may offer a more suitable overall cost. You should compare the rate, fees and total cost.

Do I need a solicitor for a product transfer?

Usually, a straightforward product transfer does not need legal work. A remortgage to a new lender usually involves legal work.

Will I need an affordability check?

A remortgage usually needs a full affordability assessment. A product transfer may involve fewer checks if it is like-for-like. Extra borrowing or major changes may trigger further assessment.

Can I borrow more with a product transfer?

Some lenders may allow further borrowing. Others may treat extra borrowing separately. Affordability and loan-to-value will usually be checked.

Can I remortgage if my income has changed?

Yes, but lender criteria will matter. A new lender will usually assess your current income and outgoings. If your income is complex, advice may help you avoid unsuitable applications.

What happens if I do nothing?

Your lender may move you onto its Standard Variable Rate when your current deal ends. This may increase your monthly payment, depending on your current rate and lender.

Should I choose the lowest rate?

Not without checking the full cost. Fees, legal costs, valuation, cashback, early repayment charges and product terms can all affect the outcome.