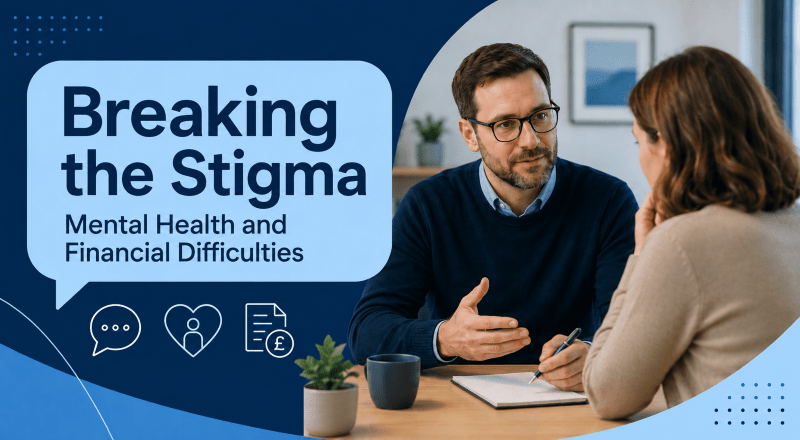

Breaking the Stigma Between Mental Health and Finance: World Mental Health Day 2023 carried a simple but important message: mental health is a universal human right.

That message matters in finance.

Money does not sit outside our emotional life. It affects sleep, confidence, relationships, work and the choices people feel able to make. When someone is worried about mortgage payments, debt, income, protection or housing security, the pressure can become more than financial.

Breaking the stigma means saying this clearly: financial difficulty is not a personal failure.

It can be caused by illness, rising costs, family changes, job loss, business pressures, bereavement, a poor credit history, or a mortgage deal ending at the wrong time. For some people, the hardest part is not the numbers. It is the shame that stops them from asking for help.

At a Glance

This article looks at the link between mental health and financial pressure.

It explains:

- Why money worries can affect emotional wellbeing

- Why stigma can stop people seeking support

- How mortgage and protection advice may help with practical decisions

- Why financial services firms must treat vulnerable customers fairly

- How Connect Mortgages supports wellbeing through people, culture and advice

- Where borrowers can start if they need mortgage or protection guidance

This article is not medical advice, debt advice or crisis support. It is a practical guide to how financial pressure and wellbeing can overlap.

Why Mental Health and Money are Connected

Financial pressure can make life feel smaller.

A person may avoid opening letters. They may delay calls. They may stop speaking about money because it feels easier to stay silent. Yet silence often makes the problem harder to manage.

Money worries can affect mental wellbeing in several ways:

- Stress from bills, mortgage payments or changing interest rates

- Anxiety about future affordability

- Low mood caused by long-term financial pressure

- Relationship strain caused by money decisions

- Isolation when people feel embarrassed about asking for support

- Reduced confidence when past credit problems affect new applications

The link can also work the other way.

Poor mental health can make financial decisions harder. It may affect concentration, paperwork, planning, communication and confidence. A person may miss deadlines or avoid important decisions because the situation feels too difficult to face.

This is why early, clear and respectful support matters.

Why Stigma Makes Financial Pressure Worse

Stigma turns a practical problem into a private burden.

Someone may feel they should have managed better. They may worry about being judged by an adviser, lender, employer, family member or friend. They may believe there is no point asking for help because their circumstances are too complex.

That is often not true.

Mortgage and protection advice is built around individual circumstances. A good adviser should look at income, commitments, credit history, property type, goals, risks and lender criteria. The purpose is not to judge. The purpose is to understand the position clearly enough to explain possible routes.

Breaking the stigma starts with better questions.

Not “Why did this happen?”

But “What is the situation now?”

Not “Who is to blame?”

But “What options can be reviewed?”

That shift matters.

The Mortgage Pressure Points That Can Affect Wellbeing

Mortgage stress is rarely caused by one issue alone.

It is often the result of several pressures arriving together. In 2023, many borrowers were thinking about higher living costs, changing mortgage rates and the end of fixed-rate deals. These pressures could affect confidence, affordability and future planning.

Common mortgage-related pressure points include:

- A fixed-rate mortgage ending

- Higher monthly payments after a product transfer or remortgage

- Missed or late payments

- Credit issues from a difficult period

- Divorce or separation

- Bereavement

- Illness or reduced income

- Self-employed income changes

- Business cash flow pressure

- Needing to raise funds for urgent costs

- Worries about protecting the family home

Some cases need careful advice because the answer is not always obvious.

A remortgage option may help some borrowers review their current deal. Others may need to understand whether a second charge mortgage is more suitable than changing their main mortgage. In time-sensitive cases, bridging finance may be considered, although it is not suitable for every borrower.

Where credit history is a concern, adverse credit mortgage advice may help a borrower understand how lenders could assess their recent conduct, deposit, income and affordability.

All borrowing must be considered carefully.

Your home may be repossessed if you do not keep up repayments on your mortgage or any loan secured on it.

Why Protection Belongs in this Conversation

Financial wellbeing is not only about borrowing.

It is also about what happens if life changes.

A mortgage is often a long-term commitment. If illness, injury, death or loss of income affects a household, the financial impact can be serious. This is why protection advice can be part of a responsible mortgage conversation.

Protection may include:

- Life insurance

- Critical illness cover

- Income protection

- Mortgage protection insurance

- Buildings and contents insurance

- Landlord insurance, where relevant

The aim is not to remove every risk. No policy can do that.

The aim is to help people understand what could happen, what support may be available, and what cover may fit their needs and budget. You can read more about mortgage protection and life insurance to understand how protection may sit alongside a mortgage.

Vulnerability, Care and Financial Services

Some people are more vulnerable to harm when making financial decisions.

This may be due to health, life events, resilience or capability. Financial firms need to recognise this and respond with care. The FCA guidance on vulnerable customers explains that firms should understand customer needs, support staff capability, respond through customer service and monitor outcomes.

This matters in mortgage advice because clients may be dealing with invisible pressure.

A client may sound calm but feel overwhelmed. They may understand the product but struggle with paperwork. They may want to act quickly, but need more time to process the risks.

Good communication can make a difficult decision easier to face.

That may mean clear explanations, no unnecessary jargon, careful suitability checks, realistic affordability conversations and enough time for the client to understand the next step.

The Role of Wellbeing at Connect Mortgages

Connect Mortgages believes wellbeing should not be treated as a slogan.

It should be seen in how people communicate, how teams support each other, and how clients are helped during important financial decisions.

The culture behind advice matters. Mortgage and protection conversations require patience, accuracy and care. A supported team is better placed to listen clearly, explain options and recognise when a client may need extra support.

You can read more about wellbeing at Connect Mortgages and how the business connects mental health, inclusion, respect and client care.

This is part of the wider point behind World Mental Health Day.

People should not have to leave their worries at the door before asking for financial help. The right conversation can help them understand their position without shame.

When Specialist Advice May Help

Some borrowers need advice that looks beyond a standard mortgage route.

This may include people with complex income, previous credit issues, unusual property types, buy-to-let needs, commercial borrowing, later-life lending questions or protection needs.

A specialist adviser can help review the facts and explain which routes may be available. That does not mean every case will be accepted by a lender. It means the borrower can get a clearer view before making decisions.

If you want to compare advisers by location, language, gender, mortgage type or specialist area, you can find a specialist mortgage or protection broker through Connect Experts.

Connect Experts is a directory and matching platform. Mortgage advice is provided by the adviser or firm selected by the customer.

Practical Steps if Money Worries are Affecting You

If financial pressure is affecting your wellbeing, it may help to start with small, practical steps.

- Write down the issue in plain terms

- Check when your mortgage rate ends

- Review your monthly commitments

- Keep letters and lender messages in one place

- Ask for help before missing a payment, where possible

- Speak to your lender if you are struggling

- Consider regulated mortgage advice before changing secured borrowing

- Seek debt advice if the issue involves unsecured debts

- Speak to a mental health professional or support service if your wellbeing is suffering

No single step fixes everything.

But one clear step can reduce the fear of the unknown.

Breaking the Stigma Starts with Clarity

Money worries can make people feel trapped. Mental health challenges can make decisions feel heavier. When both happen together, silence can become part of the problem.

Breaking the stigma means treating financial pressure as something that can be discussed, reviewed and supported.

It means recognising that people are more than their credit file, income pattern or current mortgage problem. It also means being honest about risks, affordability and suitability.

A mortgage adviser cannot replace medical, legal or debt support.

But the right adviser can help with the financial part of the picture. They can explain mortgage options, protection needs, lender criteria and possible next steps with care.

That clarity can matter.

Because sometimes progress begins when someone feels able to say, “This is my situation, and I need help understanding what comes next.”