How EPC Regulations Affect Property Value: EPC regulations can influence how a home is viewed by buyers, tenants, landlords, valuers, and mortgage lenders.

A stronger EPC rating may support market appeal, lower running costs and access to some green mortgage products. A weaker EPC rating may lead to improvement costs, rental restrictions, buyer concerns, and valuation risk.

For landlords, the issue is more direct. In England and Wales, many private rented homes must meet the minimum energy efficiency standard before they can be legally let, unless an exemption applies. For homeowners, EPC ratings may affect saleability and future borrowing options, but the impact on value depends on the property, location, cost of improvements, and buyer demand.

What Is an EPC?

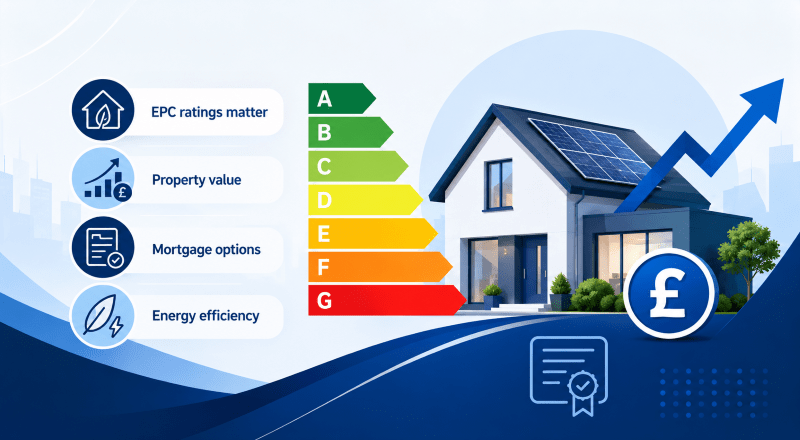

An Energy Performance Certificate, or EPC, rates a property’s energy efficiency from A to G.

An A-rated property is more energy efficient. A G-rated property is less energy efficient. The certificate also gives typical energy cost information and suggested improvements.

You usually need an EPC when a property is sold, let or built. An EPC is normally valid for 10 years. You can check the official GOV.UK Energy Performance Certificate guidance if you need to confirm the current rules.

An EPC is not just a document for a file. It is a visible signal. It tells the market how costly a property may be to run, how efficient the building is and what work may be needed in future.

That is why EPC regulations can affect value.

Why EPC Regulations Matter to Property Value

Property value is not only about bricks, location and square footage.

It is also about risk.

A buyer may ask whether the home will be costly to heat. A landlord may ask whether the property can remain legally lettable. A lender may ask whether the property is suitable security. A tenant may ask whether monthly bills will be manageable.

EPC regulations sit across all these questions.

A poor EPC rating can affect value in several ways:

- It may reduce buyer confidence.

- It may increase expected improvement costs.

- It may affect rental demand.

- It may limit landlord exit options.

- It may influence some mortgage product choices.

- It may lead to more questions during valuation.

A better EPC rating can support value in different ways:

- It may improve market appeal.

- It may reduce running costs.

- It may support access to some green mortgage products.

- It may make the property easier to rent.

- It may reduce future upgrade pressure.

- It may help buyers see the home as more future-ready.

This does not mean every EPC improvement creates an equal rise in value. A property’s location, condition, size, tenure, layout and local demand still matter. EPC is one part of the valuation picture, not the whole picture.

The Link Between EPC Ratings and Market Value

The value impact of EPC ratings is not always simple.

Some market evidence suggests that energy-efficient homes can attract a price premium. Other research shows that the premium can be modest, especially where buyers care more about location, size or affordability.

The better way to think about EPC is this:

A strong EPC rating may help the value. A weak EPC rating may create a discount risk.

That distinction matters.

A buyer may not pay much more for a C-rated property if similar homes nearby are also C-rated. But they may expect a discount for an F or G-rated property if they believe upgrades will be expensive.

This is especially relevant where improvement work could involve insulation, glazing, heating systems, ventilation, solar panels or other energy measures.

The philosophical point is simple. Property value is partly a measure of confidence. EPC regulations affect confidence by making future energy performance visible today.

EPC Rules and Buy-to-Let Property Value

EPC regulations can be more important for landlords than for owner-occupiers.

For many domestic private rented properties in England and Wales, the Minimum Energy Efficiency Standard applies. GOV.UK guidance states that landlords can no longer let or continue to let covered properties with an EPC rating below E unless a valid exemption is in place. You can read the official GOV.UK MEES landlord guidance for the current position.

This can affect property value because a rental property is often valued through income, risk and future saleability.

A low EPC rating may affect:

- whether the property can be let;

- whether a landlord needs to fund improvements;

- whether tenants may expect higher energy costs;

- whether the property is attractive against similar rentals;

- whether lenders ask more questions;

- whether future buyers see the property as a clean investment.

For landlords reviewing their finances, it may be sensible to seek buy-to-let mortgage advice before deciding whether to refinance, improve, or sell.

How EPC Ratings Can Affect Mortgage Options

Mortgage lenders do not all treat EPC ratings in the same way.

Some lenders offer green mortgage products for homes with stronger EPC ratings. These may include incentives such as cashback, lower rates or borrowing options linked to energy improvements. Criteria vary by lender and can change.

For homeowners, this means the EPC rating may become part of the mortgage conversation. It may not decide the whole application, but it can influence product choice.

For landlords, the EPC position can be more technical. Lenders may consider lettability, rental demand, future improvement costs and the property’s long-term suitability as security.

This is why EPC should be reviewed before a purchase, remortgage or major property improvement.

If the aim is to fund energy upgrades, a homeowner may need to compare savings, loan cost and long-term value. Our guide to remortgaging for home improvements explains how releasing equity may support planned renovation work.

Practical Improvements That May Support Property Value

Improving an EPC rating does not always require a full renovation.

The right work depends on the property and the EPC recommendation report. Some older homes may need more careful planning, especially where solid walls, listed status, ventilation or heating design are involved.

Common EPC improvements may include:

- loft insulation;

- cavity wall insulation;

- floor insulation;

- modern heating controls;

- efficient boilers or heating systems;

- double or triple glazing;

- LED lighting;

- solar panels;

- improved hot water insulation;

- draught reduction;

- smart thermostats.

The best improvement is not always the most expensive one. A lower-cost upgrade that moves the property into a better EPC band may offer more practical value than a costly upgrade with limited impact on the rating.

Before spending money, property owners should review:

- the current EPC rating;

- the recommended improvement list;

- the expected cost;

- the likely EPC gain;

- the effect on comfort and running costs;

- whether planning or building rules apply;

- whether the work supports the property’s target market.

When EPC Upgrades May Not Increase Value

It is important not to promise that every EPC improvement will increase a property’s value.

Some upgrades may improve comfort and energy use without producing a clear sale price increase. Others may be necessary for compliance but may not produce a profit.

EPC work may have limited value impact where:

- the property is already competitive locally;

- the improvement cost is higher than the likely uplift;

- buyers in the area are mainly driven by price or location;

- the work is poorly installed;

- the property has other major defects;

- the EPC rating improves but the home still feels dated;

- the upgrade does not suit the building type.

This is where advice matters. EPC improvement should be treated as a financial decision, not just a technical checklist.

EPC, Property Value and Remortgaging

If your mortgage deal is ending, EPC can form part of the wider remortgage review.

A remortgage may be used to secure a new rate, release equity, review borrowing or fund home improvements. However, borrowing more money increases debt and should be considered carefully.

A better EPC rating may support product choice with some lenders. A weaker EPC rating may lead to more questions, especially if the property is being let or if improvement work is expected.

You can read more about remortgage advice if you are reviewing your current mortgage and want to understand the options.

EPC Certificates and Buy-to-Let Planning

For landlords, EPC should be reviewed before buying, refinancing or expanding a portfolio.

A property with a low rating may still be attractive, but only if the numbers work after accounting for improvement costs. A cheap purchase can become expensive if insulation, heating, glazing or compliance work is needed.

Landlords should ask:

- What is the current EPC rating?

- When does the EPC expire?

- What improvements are recommended?

- What would the work cost?

- Could the property remain legally lettable?

- Would the rent support the borrowing?

- Would tenants accept the likely energy costs?

- Could future rules affect the exit plan?

The answer is rarely only about regulation. It is about resilience. A rental property with poor energy performance may still produce income today, but the question is whether it remains strong tomorrow.

How Homeowners and Landlords Can Use EPC Information

An EPC can be used as a planning tool.

For sellers, it may help shape how the property is presented to the market. For buyers, it may help identify future costs. For landlords, it may support compliance planning. For homeowners, it may help them decide whether improvements should be funded now or later.

You can also read our wider Energy Performance Certificate guide for more detail on EPCs and buy-to-let considerations.

Speak to an Adviser Before Making a Mortgage Decision

EPC regulations can affect property value, but the right decision depends on the person, the property and the borrowing.

A landlord may need to think about rental rules and portfolio finance. A homeowner may need to consider comfort, resale value, and remortgage options. A buyer may need to think about the true cost of ownership.

If you want advice tailored to your circumstances, you can use Connect Experts to find a mortgage adviser who can help you review mortgage options for your property plans.

FAQs

Do EPC regulations affect property value?

Yes, EPC regulations can affect property value. They may influence buyer demand, tenant demand, running costs, mortgage options, landlord compliance and future improvement costs.

Does a better EPC rating always increase property value?

No. A better EPC rating may improve market appeal, but it does not guarantee a higher sale price. Location, condition, size, local demand and improvement cost still matter.

Why does EPC matter more for landlords?

EPC matters more for landlords because many rented homes must meet minimum energy efficiency rules before they can be legally let, unless an exemption applies.

Can a poor EPC rating make a property harder to sell?

Yes, it can. A poor EPC rating may make buyers worry about heating costs, future upgrade work and resale risk.

Can EPC ratings affect mortgage options?

Yes, in some cases. Some lenders offer green mortgage products for homes with higher EPC ratings, while low-rated properties may lead to more questions during a mortgage review.

Should I improve my EPC before selling?

It depends on the cost, the likely rating gain and the local market. Small improvements may help, but larger work should be reviewed carefully before spending money.

Can I remortgage to fund EPC improvements?

Possibly. Some homeowners release equity to fund improvements, but this increases borrowing and should be reviewed with a mortgage adviser.