Joint Borrower Sole Proprietor mortgages can help one person buy a home with income support from another borrower, without giving the supporting borrower legal ownership of the property.

It is often used by first-time buyers, career starters, adult children, parents, and families who want to solve an affordability gap without changing who owns the home.

The idea is simple. The responsibility is not.

A JBSP mortgage separates borrowing from ownership. More than one person may be named on the mortgage, but only the sole proprietor is named on the property title. This can help a buyer borrow more, but every borrower remains responsible for the mortgage debt.

At a Glance

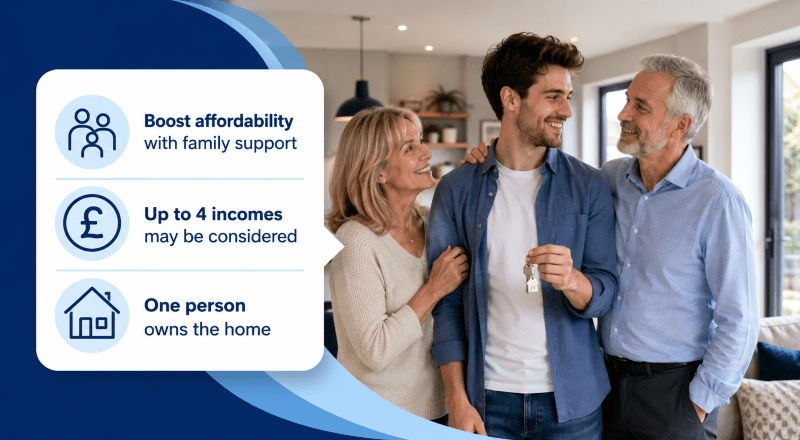

A Joint Borrower Sole Proprietor mortgage may suit a buyer who can afford the monthly payments with family support but cannot meet a lender’s affordability test alone.

The sole proprietor owns the home. The joint borrower helps with affordability and shares legal responsibility for the mortgage. The joint borrower does not usually appear on the title deeds.

This structure can be useful, but it needs careful advice. The lender will assess all applicants’ income, debts, credit history, age, affordability, and exit plan.

What is a Joint Borrower Sole Proprietor mortgage?

A Joint Borrower Sole Proprietor mortgage, often called a JBSP mortgage, allows two or more people to apply for a mortgage while only one person owns the property.

The sole proprietor is the legal owner. They are named on the title deeds and usually live in the property.

The joint borrower is named on the mortgage. Their income may help the application meet lender affordability rules. They are not usually named on the legal title.

This structure is different from a standard joint mortgage. In a joint mortgage, all borrowers are normally also owners. With a JBSP mortgage, support comes from income and liabilities, not ownership.

For many families, this is the key point. The supporter helps the buyer stand on firmer ground, but does not step into ownership.

How does a JBSP mortgage work?

A JBSP mortgage usually follows this structure:

- The buyer is named as the sole proprietor.

- A parent, relative or other acceptable supporter joins the mortgage.

- The lender assesses income, outgoings and credit details for all borrowers.

- Only the sole proprietor is normally registered as the property owner.

- All borrowers remain responsible for the mortgage payments.

- The plan should include how the joint borrower may be removed later.

This can support a buyer whose income is expected to grow. For example, a newly qualified professional may be able to manage payments but may not pass affordability checks alone at the point of purchase.

If you are buying your first home, it may also help to read the broader first-time buyer mortgage guide before comparing mortgage products.

Why do people use a JBSP mortgage?

A JBSP mortgage is usually considered when the main buyer has a clear housing need, but affordability is stretched.

Common examples include:

- A first-time buyer with a lower starting salary.

- A buyer with strong career progression but limited current income.

- A parent helping an adult child buy without becoming a co-owner.

- A borrower with variable income who needs extra strength in the application.

- A family helping a relative move closer to work, study or support.

The aim is not to borrow without discipline. The aim is to present the full financial support available while keeping ownership clear.

That distinction matters. A mortgage is not only a product. It is a long-term promise made against a home.

Who is liable for the mortgage?

All borrowers are normally jointly and severally liable for the mortgage.

This means each borrower can be responsible for the full mortgage, not just a share of it. If the sole proprietor misses payments, the lender can expect the other borrower to help meet the debt.

This is one of the most important risks on a JBSP mortgage. The supporting borrower may not own the home, but they still carry mortgage responsibility.

That liability can also affect the supporter’s future borrowing. If a parent later wants to remortgage, move home or borrow for another purpose, the JBSP mortgage may be taken into account.

Before applying, every borrower should understand:

- the monthly payment

- the full mortgage balance

- the mortgage term

- their legal responsibility

- how missed payments may affect credit files

- how and when the arrangement could end

What will lenders check?

Lenders do not treat JBSP as a shortcut around affordability. They still assess whether the mortgage is suitable and affordable.

The lender may review:

- income for all borrowers

- employment status

- self-employed income evidence

- pension income, where relevant

- existing debts and credit commitments

- dependants and household costs

- credit history for every borrower

- deposit source

- age of the oldest borrower

- mortgage term

- whether the sole proprietor will live in the property

- the proposed exit strategy

Age can be a practical issue. If the supporting borrower is older, some lenders may restrict the mortgage term. A shorter term can increase monthly payments, which may affect affordability.

Use the residential affordability calculator as an early guide, but remember that lender criteria can vary.

JBSP mortgages and Stamp Duty

A JBSP mortgage may help avoid certain ownership-related Stamp Duty issues because the supporting borrower is usually not named on the property title.

However, Stamp Duty should never be treated as a simple tick-box benefit. Rules depend on the buyer, the property, the ownership position, and the wider circumstances.

If a parent or supporter is added as a legal owner on a standard joint purchase, this may result in different Stamp Duty outcomes. This is one reason some families consider JBSP instead.

You can review the current government guidance on higher Stamp Duty Land Tax rates. You should also take tax or legal advice where needed.

For an early estimate, the Stamp Duty calculator can help you understand possible costs before you apply.

JBSP mortgage versus a joint mortgage

A JBSP mortgage and a joint mortgage are not the same.

With a joint mortgage, the borrowers usually own the property together. They may be joint tenants or tenants in common, depending on how ownership is arranged.

With a JBSP mortgage, the supporting borrower helps with affordability but is not usually on the title deeds.

That difference affects ownership, tax, control and future planning.

A JBSP mortgage may suit a buyer who wants sole ownership but needs affordability support. A joint mortgage may suit people who are buying and owning together.

The right route depends on the purpose of the purchase, the relationship between borrowers, the deposit, long-term plans and legal advice.

Benefits of a JBSP mortgage

A JBSP mortgage may offer several practical benefits.

| Potential benefit | Why it may help |

|---|---|

| Improved affordability | The lender may include income from more than one borrower. |

| Sole ownership | The main buyer may own the home without giving ownership to the supporter. |

| Family support | Parents or relatives may help without providing a large gifted deposit. |

| First-home planning | It may support buyers whose income is likely to grow. |

| Clearer exit route | The plan may allow the supporter to be removed later through remortgage or transfer, subject to criteria. |

These benefits depend on lender policy and personal circumstances.

Risks and limitations

A JBSP mortgage also has important risks.

| Risk | Why it matters |

|---|---|

| Full joint liability | Every borrower may be responsible for the whole mortgage. |

| Credit impact | Missed payments may affect all borrowers. |

| Future borrowing pressure | The supporter’s borrowing capacity may be reduced. |

| Term restrictions | The age of the oldest borrower may limit the mortgage term. |

| Fewer lender options | Not every lender offers JBSP mortgages. |

| Legal complexity | Ownership and liability are separated, so advice matters. |

A good JBSP plan should not only ask, “Can we get the mortgage?” It should also ask, “What happens in five years?”

What evidence may be needed?

The evidence depends on the lender and each borrower’s circumstances.

Common documents include:

- proof of identity and address

- payslips or income evidence

- bank statements

- tax calculations and tax year overviews for self-employed applicants

- pension income evidence, if relevant

- credit commitments

- deposit evidence

- solicitor details

- proof of relationship between borrowers, where requested

The lender may also want to understand why the supporter is joining the mortgage and how they may leave the arrangement later.

What is the exit strategy?

The exit strategy is central to a JBSP mortgage.

Many families use JBSP as a bridge. The buyer may expect their income to grow, debts to reduce, or career position to strengthen. Later, they may remortgage in their own name and remove the supporting borrower.

This is not automatic. The sole proprietor must meet lender affordability and criteria at that time.

A sensible exit plan may consider:

- likely income growth

- mortgage balance after a fixed period

- expected property value

- future remortgage options

- supporter age

- early repayment charges

- legal and advice costs

A JBSP mortgage should be designed with the future in mind, not only the purchase date.

Should protection be considered?

Protection should be part of the conversation.

If all borrowers are responsible for the mortgage, the household should consider what happens if income stops, illness occurs, or a borrower dies.

This does not mean every person needs the same cover. It means the risk should be discussed clearly.

Life cover, critical illness cover and income protection may be relevant depending on the borrower’s income sources and family position.

You can read more about mortgage protection insurance if you want to understand how cover may support a mortgage plan.

When may a JBSP mortgage not be suitable?

A JBSP mortgage may not be right if the supporter does not understand the liability, cannot afford the risk, or may need to borrow again soon.

It may also be unsuitable where the arrangement is being used to stretch borrowing too far. A larger loan is not always a better outcome.

The best mortgage structure is the one that remains workable when life changes.

Other options may include:

- a gifted deposit

- a standard joint mortgage

- a guarantor-style arrangement

- buying a lower-priced property

- waiting until income improves

- improving credit position before applying

The right answer depends on the numbers, the people and the purpose.

Speak to a mortgage adviser

JBSP mortgages can be useful, but they require careful advice because ownership and liability are allocated differently.

Connect Mortgages can help you review affordability, lender criteria, income evidence, deposit position, protection needs and the exit plan.

If you prefer to compare advisers before making contact, you can also use Connect Experts to find first-time buyer mortgage advisers across the UK.

FAQs: Joint Borrower Sole Proprietor mortgages

Can a parent help without being on the deeds?

Yes. That is one of the main reasons people consider a JBSP mortgage. A parent may support the mortgage application without usually becoming a legal owner of the property.

Does the joint borrower own the property?

Usually, no. The joint borrower is named on the mortgage but not on the legal title. The sole proprietor owns the property.

Is the joint borrower responsible for the mortgage?

Yes. The joint borrower is normally responsible for the mortgage debt along with the sole proprietor. This can apply even if they do not live in the property.

Can a joint borrower be removed later?

Possibly. This may happen through a remortgage or lender-approved change when the sole proprietor can pass affordability checks alone. It is not guaranteed.

Does a JBSP mortgage avoid Stamp Duty?

It may help avoid some ownership-related Stamp Duty issues because the supporter is not usually a legal owner. However, Stamp Duty depends on personal circumstances, property ownership and current rules. Tax advice may be needed.

Can I get a JBSP mortgage if I am self-employed?

Yes, it may be possible. Lenders will usually want income evidence such as accounts, tax calculations and bank statements. Criteria vary between lenders.

Does the joint borrower need to live in the property?

Usually, no. The sole proprietor is normally expected to live in the property. Lender rules can vary.

How many people can be on a JBSP mortgage?

This depends on the lender. Some lenders may allow more than two borrowers, but not all applicants will be treated the same way for affordability.

Is a JBSP mortgage the same as a guarantor mortgage?

No. A JBSP mortgage names the supporter as a borrower on the mortgage. A guarantor arrangement is structured differently and may involve separate security or guarantees.

What is the biggest risk of a JBSP mortgage?

The main risk is joint liability. A supporter may not own the home but may still be responsible for the full mortgage if payments are missed.