Self-Employed Mortgage Guide: What Lenders Need to See – Being self-employed does not stop you from getting a mortgage.

The real question is not whether you work for yourself. It is whether your income can be clearly evidenced, properly checked, and assessed as sustainable by a lender.

That is the part many self-employed applicants underestimate. A good business may still look unclear on paper if the right documents are missing, income has changed, or accounts do not explain the full picture.

This guide explains what lenders may check, what documents you may need, and how to prepare before applying for a mortgage.

At a Glance

Self-employed applicants can apply for the same residential mortgage products as employed applicants. There is not usually a separate “self-employed mortgage” product.

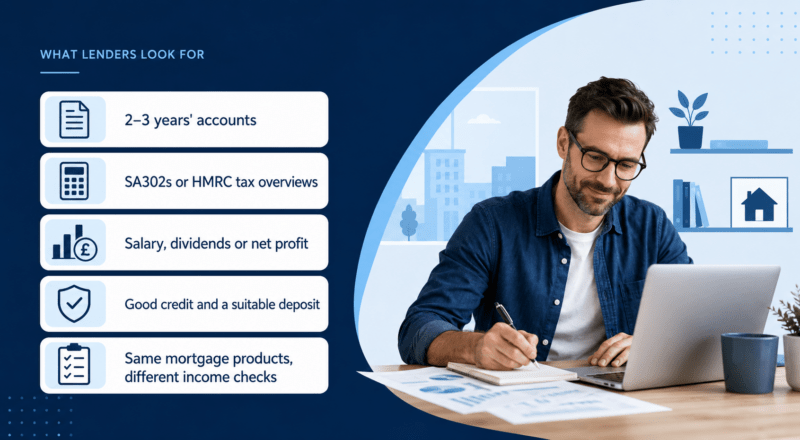

The main difference is income assessment. Instead of payslips and a P60, lenders may review tax records, accounts, dividends, retained profit, contracts, bank statements and business performance.

You may need:

- SA302 tax calculations

- Tax Year Overviews

- Finalised accounts

- Business and personal bank statements

- Accountant details

- Contract evidence, if you are a contractor

- Proof of deposit

- Credit commitments and regular expenditure

If you want advice before applying, Connect Mortgages can help with self-employed mortgage advice.

How Does a Self-Employed Mortgage Differ?

A mortgage for a self-employed person is usually no different from a mortgage for an employed person.

The difference is how the lender checks income. Employed applicants often have regular monthly pay. Self-employed income can vary due to trading patterns, business costs, dividends, tax planning, or seasonal work.

Lenders therefore want to understand three things:

- What you earn

- How reliable is that income

- Whether the mortgage remains affordable after tax, spending and commitments

This is why preparation matters. A lender is not only looking at the number on your application. They are looking at the evidence behind it.

Who Counts as Self-Employed for a Mortgage?

You may be treated as self-employed if your income comes from your own work, business or company structure.

This may include:

- Sole traders

- Freelancers

- Contractors

- Limited company directors

- Business partners

- CIS workers

- Shareholders with business income

Some lenders may treat company directors differently depending on their shareholding, salary, dividends and retained profit. This is why two applicants with similar earnings can receive different lender outcomes.

What Documents May Lenders ask for?

The documents depend on your business structure and lender criteria.

Sole traders and freelancers are often assessed using net profit. This is usually shown through tax calculations and Tax Year Overviews.

Limited company directors may be assessed using salary and dividends. Some lenders may also consider retained profit, depending on their criteria.

Contractors may need to provide current and previous contracts, evidence of day rates, bank statements, and trading history.

Partnership income may be assessed based on your share of the net profit. The lender may want accounts and tax documents to confirm this.

HMRC explains that self-employed applicants may be asked to provide an SA302 tax calculation and a Tax Year Overview as evidence of income when applying for a mortgage.

How Many Years of Accounts Do You Need?

Many lenders prefer two years of accounts or tax records.

Some may consider one year, but this depends on the wider case. A stronger application may include a good deposit, a clean credit history, stable bank statements, previous experience in the same trade, or signed contracts for future work.

Three years of figures may help where income has moved up and down. It can give the lender more context.

The key point is consistency. Lenders do not only want to know what happened last year. They want to understand whether the income is likely to continue.

What if your income Has Changed?

Self-employed income is rarely perfectly flat.

If your income has increased, the lender may ask why. Growth can be positive, but it may need evidence. This could include new contracts, business bank statements or accountant commentary.

If your income has fallen, the lender may also ask why. A one-off cost, business investment or temporary change may need explaining.

This is where advice can be useful. The figures need to be presented in a way that is accurate, clear and supported by evidence.

How Affordability is Assessed

Lenders look beyond income.

They may review your regular spending, credit commitments, dependants, mortgage term, deposit, property type and future affordability. This applies to all mortgage applicants, but self-employed applicants may need more income evidence.

The aim is not just to prove that you earn money. It is to show that the mortgage is affordable now and can remain affordable over the term.

Before applying, you can use a mortgage calculator to understand possible monthly repayments. This is only a guide, but it can help you think about a budget before giving advice.

How to Improve Your Chances Before Applying

Good preparation can reduce delays.

Start by checking that your tax records and accounts are complete. Make sure your bank statements support the income being declared. Avoid unnecessary new borrowing before applying. Check your credit file and correct any errors.

It can also help to speak with your accountant before submitting a mortgage application. They may be able to explain figures, confirm retained profit or provide documents in the format a lender expects.

A mortgage adviser can then help review lender options based on your income type, deposit, credit position and property plans.

Can You Remortgage if You Are Self-Employed?

Yes, self-employed applicants can remortgage.

A lender may still ask for up-to-date income evidence, even if you already own the property. This can include recent accounts, SA302s, Tax Year Overviews and bank statements.

If your current deal is ending, it is sensible to review your remortgage options before leaving enough time for document checks.

What About Protection?

Self-employed applicants should also think about protection.

A mortgage is a long-term commitment. If you work for yourself, you may not have employer sick pay, death-in-service cover or employee benefits. That can make protection planning more important.

You can read more about mortgage protection insurance and how it may support mortgage planning.

When Should You Speak to an Adviser?

You may want to speak to an adviser before applying if:

- You have one year of accounts

- Your income has changed recently

- You are a company director

- You use dividends or retained profit

- You are a contractor

- You have credit issues

- You are remortgaging

- You are unsure which documents are needed

Some applicants also want to choose an adviser by location, language or area of experience. Connect Experts can help you find a self-employed mortgage broker where specialist adviser matching is useful.

FAQs

Can I get a mortgage if I am self-employed?

Yes. Self-employed people can get residential mortgages. The main difference is that lenders usually need more evidence of income than they would for an employed applicant.

Do self-employed applicants pay higher mortgage rates?

Not always. Rates depend on lender criteria, deposit, credit profile, affordability, property type and the strength of the application. Being self-employed alone does not automatically mean a higher rate.

What income do lenders use for sole traders?

Lenders often use net profit shown in tax calculations and Tax Year Overviews. Some may average figures over two or more years.

What income do lenders use for company directors?

Some lenders use salary and dividends. Others may consider retained profit, depending on their criteria and the strength of the business.

Can I get a mortgage with one year of accounts?

It may be possible, but lender choice may be smaller. Strong supporting evidence can help, such as a good deposit, clear bank statements, previous trade experience or signed contracts.

Should I apply before my accounts are ready?

It is usually better to prepare documents first. Missing or unclear evidence can delay the application or limit lender options.