Top 8 Reasons to Consider Remortgaging – A mortgage is rarely a one-time decision.

It is a financial structure that should be reviewed as life, rates, property value and lender criteria change. Remortgaging is one way to check whether your current mortgage still fits your circumstances.

Sometimes the reason is simple. Your fixed rate may be ending. At other times, the reason is more technical. You may want to release equity, change the term, review interest-only options, consolidate debts or compare a product transfer with a new lender deal.

The right answer is not always the lowest rate. It is the option that works after fees, affordability checks, early repayment charges, future plans and risk have been considered.

Your home may be repossessed if you do not keep up repayments on your mortgage.

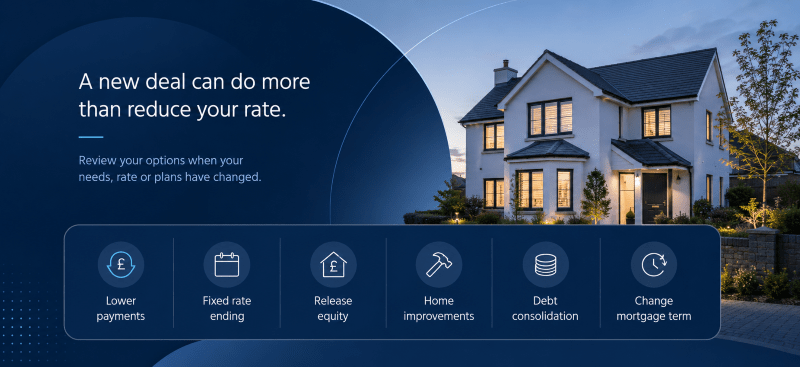

At a Glance

You may consider remortgaging if you want to:

- Review your mortgage before your current rate ends

- Avoid moving onto your lender’s standard variable rate

- Compare a product transfer with a full remortgage

- Release equity from your property

- Borrow more for home improvements

- Consolidate debts, where suitable

- Change your mortgage term or repayment method

- Move to a lender that better fits your income or property type

Before deciding, check the full cost. This includes the rate, fees, early repayment charges, valuation, legal work, monthly payment and total interest over the mortgage term.

What Does Remortgaging Mean?

Remortgaging means replacing your current mortgage with a new mortgage deal on the same property.

This may involve moving to a new lender. It may also mean staying with your current lender through a product transfer.

A remortgage is not the same as moving home. The property remains the same, but the mortgage terms may change.

You can read more about the process on the Connect Mortgages guide to remortgage deals and UK remortgage advice.

1. Your Current Mortgage Deal Is Ending

Many homeowners review their mortgage when a fixed, tracker or discounted rate is due to end.

This matters because the mortgage may move onto the lender’s standard variable rate when the deal ends. That rate can be higher than the rate you were paying before.

A remortgage review can help you compare:

- Fixed-rate options

- Tracker-rate options

- Product transfers

- New lender deals

- Fees and incentives

- Early repayment charge timings

- Monthly payment changes

Timing is important. Some lenders allow borrowers to secure a new deal before the existing rate ends. This can help you avoid a rushed decision.

A practical review should start with three questions.

When does the current rate end?

What happens if you do nothing?

Does the new deal still suit your income and future plans?

2. You Want to Avoid the Standard Variable Rate

A standard variable rate is the lender’s follow-on rate. It usually applies when a mortgage deal ends and no new deal is arranged.

It can move up or down. It may also be higher than fixed or tracker rates available elsewhere.

This does not mean every borrower should remortgage immediately. Fees, early repayment charges and eligibility still matter.

However, ignoring the standard variable rate can be costly. A review helps you understand whether staying put, switching product or remortgaging could be more suitable.

Use the quick mortgage calculator to estimate how different rates could affect monthly payments.

3. You Want to Compare a Product Transfer With a Full Remortgage

A product transfer means staying with your current lender and moving to a new mortgage product.

A full remortgage usually means moving to a new lender. The new mortgage pays off the existing mortgage.

Both routes can be useful. However, they work differently.

A product transfer may be simpler because you remain with the same lender. In some cases, it may involve less paperwork and no full legal process.

A full remortgage may give access to a wider range of lenders. It may also allow you to raise extra funds or change wider mortgage terms.

The better option depends on:

- Your loan-to-value

- Your credit profile

- Your income

- Your current lender’s rates

- Fees and charges

- Whether you need extra borrowing

- Whether the property meets lender criteria

A remortgage review should compare both routes. The lowest headline rate may not be the best overall outcome after fees.

4. Your Property Value Has Changed

Property value affects loan-to-value.

Loan-to-value compares the mortgage balance with the property value. For example, a smaller mortgage compared with a higher property value may place you in a lower loan-to-value band.

This can matter because some lenders price mortgage products by loan-to-value.

If your home has increased in value, you may have more equity than before. That could improve your product options.

However, property value must be realistic. A lender may use a valuation before approving the mortgage.

The practical checks are:

- Current mortgage balance

- Estimated property value

- Loan-to-value band

- Remaining term

- Current rate and fees

- Any early repayment charge

- Whether extra borrowing is required

A higher property value can help, but it does not replace affordability checks.

5. You Want to Release Equity

Some homeowners remortgage to release equity from their property.

Equity is the difference between the property value and the mortgage balance. Releasing equity means borrowing more against the home.

Common reasons include:

- Home improvements

- Supporting a property purchase

- Helping family

- Paying for essential repairs

- Restructuring finances

- Reviewing existing secured borrowing

This should be considered carefully. Borrowing more may increase monthly payments. It may also increase the total interest paid over the life of the mortgage.

A lender will usually assess income, credit commitments, property value, mortgage balance and the reason for borrowing.

The key question is not only whether you can borrow more. It is whether the borrowing remains suitable over time.

6. You Want to Fund Home Improvements

A remortgage can be used to fund property improvements where suitable.

This may include repairs, renovations, extensions, energy improvements or changes needed because the household has changed.

Home improvement borrowing should be planned with care. The work may improve how the home functions, but the mortgage debt may also increase.

Before using a remortgage for home improvements, check:

- The project cost

- Planning or building control needs

- Contingency costs

- The impact on monthly payments

- The total interest over the mortgage term

- Whether a further advance or second charge mortgage may be better

You can read more on remortgaging for home improvements.

7. You Want to Consolidate Debts

Some homeowners consider remortgaging to consolidate debts.

This means using mortgage borrowing to repay other debts, such as loans or credit cards. It may reduce monthly payments because the debt is spread over a longer term.

However, this is a major financial decision.

Debt consolidation can turn unsecured debt into debt secured against your home. It may also increase the total amount repaid if the debt is spread over many years.

Before considering this route, review:

- The debts being repaid

- Current interest rates

- Existing monthly payments

- The new mortgage payment

- The full term cost

- Fees and charges

- Whether spending habits have changed

- The risk of building new debt afterwards

A lower monthly payment does not always mean a lower total cost.

Read the Connect Mortgages guide to remortgaging to consolidate debts before making a decision.

8. You Want to Change Your Mortgage Term or Repayment Method

Remortgaging may allow you to review the structure of your mortgage.

Some borrowers may want to extend the term to reduce monthly payments. Others may want to shorten the term to repay the mortgage faster.

Some may want to review repayment and interest-only options.

A repayment mortgage means each monthly payment covers interest and part of the mortgage balance. Over time, the balance reduces.

An interest-only mortgage means the monthly payment covers interest only. The mortgage balance remains outstanding and must be repaid at the end of the term.

This can reduce monthly payments, but it creates a serious long-term repayment need.

Before changing the mortgage term or repayment method, consider:

- Monthly affordability

- Total interest over the term

- Retirement plans

- Repayment strategy

- Income stability

- Future moving plans

- Lender criteria

The structure of a mortgage should support the life behind it. A lower payment today should not create a harder problem tomorrow.

When Remortgaging May Not Be the Right Option

Remortgaging can be useful, but it is not always suitable.

It may not be the best route if:

- Your current deal has high early repayment charges

- You plan to move home soon

- Your income has reduced

- Your credit profile has changed

- You have limited equity

- The fees outweigh the saving

- A product transfer is more suitable

- A second charge mortgage may fit the need better

- You are extending debt without a clear plan

A remortgage should be reviewed against the alternatives. For some borrowers, a further advance, product transfer or second charge mortgage may need to be compared.

What Lenders Usually Check

Lenders may assess:

- Income

- Employment type

- Outgoings

- Credit history

- Mortgage balance

- Property value

- Loan-to-value

- Mortgage term

- Age and retirement plans

- Property type

- Reason for extra borrowing

Self-employed borrowers, contractors, landlords and applicants with complex income may need more detailed evidence.

This is why remortgaging is not just a rate search. It is a review of fit, risk and lender criteria.

Documents You May Need

The documents needed can vary by lender and case type.

You may need:

- Proof of income

- Bank statements

- Mortgage statement

- Identification

- Proof of address

- Property details

- Credit commitment details

- Evidence of bonuses, overtime or self-employed income

- Details of any extra borrowing purpose

Preparing documents early can reduce delays.

How Early Should You Review Your Mortgage?

A good time to start reviewing your mortgage is often around six months before your current deal ends.

This gives you time to check your current rate, compare options, review fees and prepare documents.

It may also help you avoid moving onto a standard variable rate by accident.

If your deal has already ended, it may still be worth reviewing your options.

Speak to a Remortgage Adviser

Remortgaging is not only about finding a new rate. It is about checking whether your mortgage still supports your plans.

A suitable review should consider the rate, fees, term, repayment method, equity, affordability and long-term cost.

If you want to compare advisers, Connect Experts can help you search by location, language and mortgage specialism. You can use Remortgage Mortgage Brokers UK to find advisers who may help with remortgage reviews.

You can also use the wider Find Your Mortgage Broker search if you want to compare advisers across different mortgage needs.

FAQs: Top 8 Reasons to Consider Remortgaging

What is the main reason to consider remortgaging?

The main reason is often to review your mortgage before your current deal ends. This can help you compare new rates, product transfers, fees and lender options before moving onto a standard variable rate.

Is remortgaging always cheaper?

No. Remortgaging is not always cheaper. You need to compare the interest rate, fees, early repayment charges, legal costs, valuation costs and total interest over the mortgage term.

Can I remortgage to release equity?

Yes, you may be able to remortgage to release equity if your property value, mortgage balance, affordability and lender criteria support the application. Borrowing more may increase your monthly payments and total interest.

Can I remortgage for home improvements?

Yes, some homeowners remortgage to fund home improvements. However, you should compare the full cost against alternatives such as a further advance, savings, personal borrowing or a second charge mortgage.

Can I remortgage to consolidate debts?

You may be able to remortgage to consolidate debts, but this needs careful advice. It may reduce monthly payments, but it can increase the total amount repaid and secure previously unsecured debts against your home.

Is a product transfer the same as a remortgage?

No. A product transfer usually means staying with your current lender and moving to a new product. A full remortgage usually means moving to a new lender and replacing the existing mortgage.

How early should I start looking at remortgage options?

Many homeowners start reviewing options around six months before their current deal ends. This gives time to compare rates, check fees and prepare documents.

Do I need a broker to remortgage?

You do not have to use a broker. However, a mortgage adviser can help compare product transfers, new lender deals, affordability, fees and lender criteria before you decide.

Can I remortgage with bad credit?

It may be possible, but options can be more limited. Lenders will review the type, date and seriousness of the credit issue, alongside income, equity and affordability.

What should I check before remortgaging?

Check your current balance, property value, deal end date, early repayment charge, income, credit commitments, fees, monthly payment and total mortgage cost.