Interest-Only Mortgage for First-Time Buyers: Buying your first home is not only a question of borrowing enough.

It is also a question of repayment, risk and future discipline.

An interest-only mortgage can look attractive because the monthly payments are lower than those of a repayment mortgage. However, the lower payment does not mean the debt is reducing. The loan balance remains in place and must be repaid at the end of the mortgage term.

For a first-time buyer, that distinction matters. The first home often comes with new costs, new responsibilities and less experience of long-term property finance. Therefore, an interest-only mortgage should not be seen as an easy route into ownership. It should be treated as a structured borrowing decision with a clear repayment plan.

This guide explains how an interest-only mortgage works for first-time buyers, what lenders may look for, what risks to consider and what alternatives may be more suitable.

At a Glance

A first-time buyer may be able to get an interest-only mortgage, but it is usually harder to get than a standard repayment mortgage.

With an interest-only mortgage, you pay only the monthly interest, not the loan principal. At the end of the term, the original mortgage balance must still be repaid.

This means lenders usually want to see:

- A credible repayment strategy

- Strong affordability

- A suitable deposit

- Stable income

- A good credit profile

- A property that meets lender criteria

- Evidence that the plan can work over time

Many first-time buyers may find a repayment mortgage more suitable. You can compare the wider first-time buyer journey on our First-Time Buyer Mortgage page.

What Is an Interest-Only Mortgage?

An interest-only mortgage is a mortgage where your monthly payments cover only the interest charged by the lender.

The capital borrowed is not repaid through your monthly mortgage payment. Instead, you must repay the full balance at the end of the term.

For example, if you borrow £250,000 on an interest-only basis, the £250,000 capital must still be repaid when the mortgage ends. Your monthly payments only cover the interest during the term.

This is different from a repayment mortgage. With a repayment mortgage, each monthly payment covers both interest and part of the loan balance. Over time, the amount owed reduces.

MoneyHelper explains more about ways of repaying an interest-only mortgage, including the need for a repayment plan.

Why Would a First-Time Buyer Consider Interest-Only?

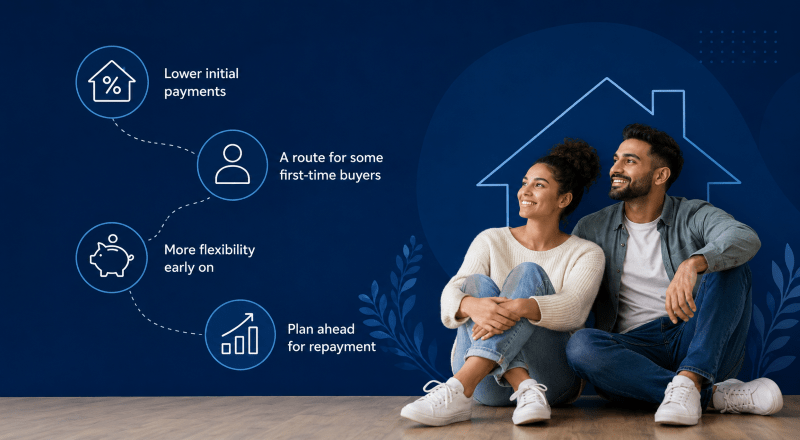

A first-time buyer may consider interest-only because the monthly payments can be lower.

This may seem helpful when budgeting for a first home, especially when other costs are due as well. These can include legal fees, valuation fees, surveys, moving costs, furnishing costs and insurance.

However, lower monthly payments can create a false sense of affordability. The mortgage may feel manageable each month, while the full debt remains unchanged in the background.

That is why the key question is not only whether the payment is lower. The key question is whether the repayment plan is realistic.

Interest-Only Mortgage vs Repayment Mortgage

| Feature | Interest-only mortgage | Repayment mortgage |

|---|---|---|

| Monthly payment | Usually lower | Usually higher |

| Capital repayment | Not repaid monthly | Repaid gradually |

| Balance at end of term | Full mortgage balance remains | Mortgage should be cleared |

| Repayment plan needed | Yes | Built into monthly payments |

| Risk level | Higher if no plan is maintained | Lower if payments are kept up |

| First-time buyer suitability | Limited and case-specific | More common |

An interest-only mortgage can provide payment flexibility. However, a repayment mortgage gives a clearer path to owning the property outright.

Can First-Time Buyers Get an Interest-Only Mortgage?

Yes, some first-time buyers may be considered for an interest-only mortgage.

However, acceptance depends on lender criteria. It is not only about income or deposit size. Lenders also need to understand how the mortgage will be repaid at the end of the term.

A lender may assess:

- Your income

- Your deposit

- Your credit history

- Your age and mortgage term

- Your employment type

- Your existing debts

- Your monthly commitments

- The property value

- The loan-to-value ratio

- The proposed repayment strategy

Some lenders may restrict interest-only borrowing to certain borrower types, higher incomes, lower loan-to-value cases or stronger repayment plans.

What Repayment Plans Might Lenders Consider?

A repayment plan is the method used to repay the mortgage capital at the end of the term.

Possible repayment strategies may include:

- Sale of investments

- Pension lump sum, where suitable

- Sale of another property

- Regular savings or investment plan

- Downsizing, where accepted by the lender

- Part repayment and part interest-only structure

Not every lender accepts every repayment strategy. Some may not accept property sale as the only plan unless strict conditions are met.

A repayment plan should not rely on hope alone. Future house price growth, expected inheritance or possible bonuses may not be enough for lender approval.

Why the Repayment Plan Matters

An interest-only mortgage shifts responsibility onto the borrower.

With a repayment mortgage, the capital is reduced through monthly payments. With interest-only, the borrower must keep the repayment plan active throughout the mortgage term.

This can be difficult because life changes. Income may change. Investments may underperform. Family costs may rise. Property plans may shift.

That is why the repayment plan should be reviewed regularly, not only at the start of the mortgage.

What Deposit Might Be Needed?

First-time buyers often focus on deposit size first. That is understandable because the deposit affects the loan-to-value ratio.

For interest-only borrowing, some lenders may expect a larger deposit than they would for a standard repayment mortgage. A lower loan-to-value can reduce lender risk and may improve the chance of approval.

However, deposit rules vary. A high income and a clear repayment plan may help, but they do not guarantee acceptance.

Before applying, it can help to check your possible borrowing position using the Residential Affordability Calculator.

What Are the Main Risks?

Interest-only mortgages carry specific risks for first-time buyers.

The biggest risk is reaching the end of the term without enough money to repay the capital.

Other risks include:

- The property may not rise in value as expected

- Investments may not perform as planned

- Savings may not grow quickly enough

- Income could fall

- Remortgage options may be limited later

- Interest rates may change after a fixed period

- The home may need to be sold if the debt cannot be repaid

This does not mean interest-only is always unsuitable. It means the structure needs careful planning.

What Are the Possible Benefits?

Interest-only mortgages may offer benefits in specific cases.

The main benefit is lower monthly payments when compared with a repayment mortgage of the same size and interest rate.

This may help borrowers with a strong repayment plan who need more monthly flexibility. It may also help where income is expected to rise, although lenders will still assess affordability based on current criteria.

Possible benefits include:

- Lower monthly payments

- More short-term cash flow flexibility

- Potential to direct funds into a separate repayment plan

- Possible part-and-part options with some lenders

- More control over capital repayment, where discipline is strong

These benefits only work when the repayment plan remains realistic.

What Costs Should First-Time Buyers Consider?

The monthly mortgage payment is only one cost.

First-time buyers should also budget for:

- Mortgage arrangement fees

- Valuation fees

- Solicitor or conveyancing fees

- Survey costs

- Search fees

- Buildings insurance

- Contents insurance

- Moving costs

- Furniture and repairs

- Service charges, if buying leasehold

- Stamp Duty, where payable

Interest-only can reduce the monthly mortgage payment, but it does not remove the wider cost of buying a home.

Could Part-and-Part Be an Option?

Some borrowers may consider a part-and-part mortgage.

This means part of the mortgage is on repayment and part is on interest-only. The repayment component decreases over time, while the interest-only component still requires a repayment strategy.

This can sometimes create a middle ground. Monthly payments may be lower than with a full repayment mortgage, but some capital is still repaid each month.

However, part-and-part borrowing is still subject to lender criteria. It also needs a clear plan for the interest-only part.

When Might Interest-Only Be Unsuitable?

Interest-only may be unsuitable where the repayment plan is weak or unclear.

It may also be unsuitable if the buyer is using it only because a repayment mortgage feels too expensive. In that case, the issue may be affordability, not product choice.

It may be unsuitable if:

- There is no credible repayment plan

- The buyer is relying only on future house price growth

- The deposit is too small for lender criteria

- The buyer has unstable income

- Existing debt levels are high

- The buyer does not want investment or repayment-plan risk

- Selling the home would cause serious difficulty later

A mortgage should support the home purchase, not hide a future problem.

Alternatives for First-Time Buyers

Interest-only is not the only route.

A first-time buyer may also consider:

- Repayment mortgage

- Fixed-rate mortgage

- Tracker mortgage

- Longer mortgage term, where suitable

- Part-and-part mortgage

- Family-assisted mortgage options

- Joint borrower arrangements

- Shared ownership, where appropriate

- Saving a larger deposit before applying

The right option depends on income, deposit, credit history, property type and long-term plans.

You can learn more about how interest-only borrowing works in a residential context on our Interest-Only Residential Mortgage page.

How a Mortgage Broker Can Help

A mortgage broker can help a first-time buyer understand whether interest-only is realistic.

This can include checking lender criteria, affordability, repayment strategy options and deposit requirements. A broker can also compare interest-only with repayment and part-and-part options.

The aim is not simply to find the lowest monthly payment. The aim is to understand whether the mortgage structure fits the buyer’s circumstances.

Some buyers may want to choose an adviser by location, language or mortgage area. Connect Experts lets you search for first-time buyer mortgage advisers across the UK.

Documents You May Need

Lenders may ask for documents to assess your mortgage application.

These may include:

- Proof of ID

- Proof of address

- Payslips

- Bank statements

- Proof of deposit

- Credit commitment details

- Employment contract, where relevant

- Tax documents, if self-employed

- Evidence of your repayment strategy

- Details of the property being purchased

If the application is interest-only, the repayment strategy evidence can be especially important.

Protection Should Not Be Ignored

Buying a first home creates a long-term financial commitment.

If illness, injury, death or loss of income affects the household, mortgage payments may become harder to maintain. This is why protection should be discussed as part of the wider mortgage conversation.

Protection does not repay an interest-only mortgage on its own unless the policy is designed for that purpose. However, it can help protect the household against specific risks.

You can read more about cover options on our Mortgage Protection and Life Insurance page.

FAQ: Interest-Only Mortgage for First-Time Buyers

Can a first-time buyer get an interest-only mortgage?

Yes, but it may be difficult. Lenders usually need strong affordability, a suitable deposit and a credible repayment plan.

Is an interest-only mortgage cheaper?

The monthly payments are usually lower than a repayment mortgage. However, the original loan balance is not being reduced.

What happens at the end of an interest-only mortgage?

The full capital balance must be repaid. This is usually done through a repayment plan agreed with the lender.

Do I need a repayment plan?

Yes. A lender will normally want to know how you plan to repay the mortgage capital at the end of the term.

Can I rely on selling the property?

Some lenders may consider property sale in certain cases. However, they may apply strict rules and may not accept it for every borrower.

Is interest-only better than repayment?

Not usually for a first-time buyer unless there is a clear reason and a strong repayment plan. A repayment mortgage is more common because the debt reduces over time.

Can I switch from interest-only to repayment later?

Some lenders may allow this, subject to affordability and product terms. However, you should not rely on a future switch without checking the position first.

What is the main risk of interest-only?

The main risk is reaching the end of the mortgage term without enough money to repay the original loan.