Let-to-Buy vs Buy-to-Let: Which Mortgage Fits? A property decision is rarely about just one mortgage. It is about purpose, timing, income, risk and what you want the property to become.

That is the real difference between let-to-buy and buy-to-let.

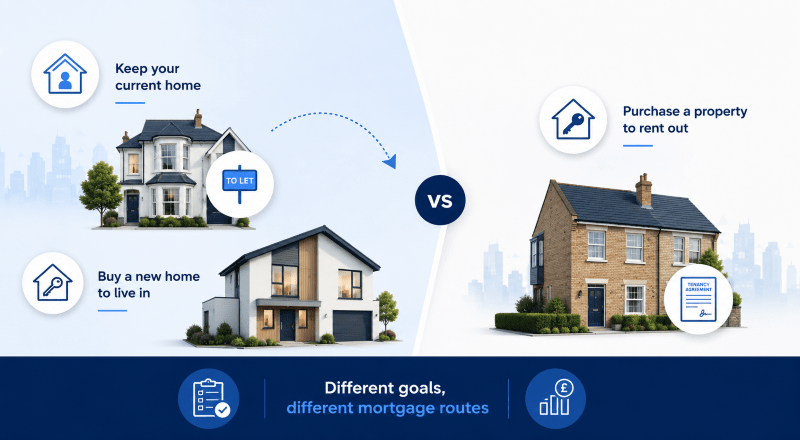

Let-to-buy usually starts with a home you already own. You move out, rent it to tenants, and buy another home to live in.

Buy-to-let usually starts with an investment decision. You buy or refinance a property to rent it out.

Both routes involve tenants, rent and lender checks. However, they are not the same product. They are built around different intentions.

Let-to-Buy vs Buy-to-Let at a Glance

Let-to-buy may suit homeowners who want to move home but keep their current property as a rental.

Buy-to-let may suit landlords or investors buying a property mainly for rental income.

The key difference is purpose. Let-to-buy combines a rental plan with a new home move. Buy-to-let focuses on a rental property as an investment.

Before choosing either route, check deposit, equity, rental income, affordability, tax, landlord duties and timing.

What Is Let-to-Buy?

Let-to-buy is when you rent out your current home and buy a new residential property to live in.

In many cases, this involves two mortgages. Your existing home may move onto a rental mortgage. Your next property may need a new residential mortgage.

A let-to-buy mortgage may be considered when you want to move but do not want to sell your current home.

This route can appeal to homeowners who see long-term value in keeping their existing property. However, the decision must work on paper before it works in practice.

Lenders may look at:

- Your equity in the current home

- The expected rental income

- Your new residential mortgage affordability

- Your income and credit profile

- The property condition and tenancy plan

- Your deposit source for the next purchase

- Whether both transactions can complete in time

Let-to-buy can be useful, but it is often time-sensitive. The old home, the new home, the rental valuation and both mortgage applications need to work together.

What Is Buy-to-Let?

Buy-to-let is used when you buy or refinance a property that will be rented to tenants.

A buy-to-let mortgage is usually assessed around the property’s expected rent. Lenders may also review your deposit, income, landlord experience, credit history and ownership structure.

Buy-to-let may suit:

- First-time landlords

- Existing landlords

- Portfolio landlords

- Limited company landlords

- HMO investors

- Property investors reviewing an existing rental mortgage

The property is usually not intended for you to live in. It is assessed as a rental property, not as your main home.

Many buy-to-let mortgages are arranged on an interest-only basis. This can help with monthly cash flow, but the capital must still be repaid at the end of the term.

The Core Difference

Let-to-buy begins with a home you already own.

Buy-to-let begins with a property you want to rent out.

That distinction matters because lenders look at purpose. A lender will want to know whether you are moving home, investing, remortgaging, releasing equity or building a rental portfolio.

| Feature | Let-to-Buy | Buy-to-Let |

|---|---|---|

| Main purpose | Move home and keep your current property | Buy or refinance a rental property |

| Starting point | You already own the property | You may be buying a rental property |

| Number of mortgages | Usually two | Usually one |

| Property you live in | The new residential home | Not the rental property |

| Rental income | Used to assess the retained home | Used to assess the investment property |

| Timing pressure | Often higher | Usually lower, unless purchase deadlines apply |

| Typical user | Home mover keeping a property | Landlord or investor |

| Main risk | Managing two mortgages and a move | Rental yield, costs and landlord duties |

How Let-to-Buy Works in Practice

A let-to-buy case often has several moving parts.

You may need to remortgage your current home onto a rental basis. You may also need a new residential mortgage for the home you plan to buy.

The lender on the current property may want to know whether the rent can support the mortgage. The lender on the new home will assess whether your income supports the residential borrowing.

This means your case may need two separate affordability checks.

A typical let-to-buy journey may involve:

- Checking the current mortgage terms

- Valuing the current home

- Estimating achievable rent

- Reviewing equity available for the new deposit

- Applying for the rental mortgage

- Applying for the new residential mortgage

- Coordinating both transactions with solicitors

- Preparing for landlord responsibilities

The process should not be rushed. A small timing issue can affect the whole move.

How Buy-to-Let Works in Practice

A buy-to-let case is more focused on the rental property itself.

The lender will usually assess whether the expected rent covers the mortgage payment by a set margin. This is often known as rental coverage or interest cover.

They may also check your personal income. Some lenders require a minimum income, while others take a more flexible view.

A buy-to-let assessment may include:

- Expected monthly rent

- Property value

- Deposit size

- Loan-to-value ratio

- Property type

- Tenancy type

- Credit history

- Landlord experience

- Personal or limited company ownership

- Existing rental portfolio details

The lowest rate is not always the best product. Fees, early repayment charges and rental stress calculations can change the overall result.

Deposit and Equity

Let-to-buy and buy-to-let both often require strong equity or a larger deposit.

For let-to-buy, the key question is whether there is enough equity in the current home. You may want to release some of that equity to support the next purchase.

However, releasing equity increases the borrowing on the retained property. The expected rent must still support the new mortgage.

For buy-to-let, the deposit usually comes from savings, equity release from another property, or retained business funds. Lenders will still need to understand the deposit source.

Deposit planning matters because it affects:

- Lender choice

- Interest rate options

- Rental stress test results

- Monthly payments

- Product fees

- Overall risk

A stronger deposit may create more options, but it does not remove the need for a suitable rental assessment.

Rental Income and Affordability

Rental income sits at the centre of both routes.

In a let-to-buy case, rent from the current home may support the mortgage on that property. However, the new home still needs a separate affordability assessment.

In a buy-to-let case, rent is usually the main part of the mortgage assessment. Yet lenders may also consider income, credit history and wider financial commitments.

The property should be assessed realistically. A high rent estimate may look helpful, but lenders often rely on their own valuation and rental assessment.

You should consider:

- Local rental demand

- Likely void periods

- Maintenance costs

- Letting agent fees

- Mortgage payments

- Insurance

- Tax position

- Future rate changes

Rent is income, but it is not certainty. A good mortgage plan allows for gaps, repairs and rate changes.

Stamp Duty and Tax

Tax can change the outcome of both routes.

If you buy an additional residential property in England or Northern Ireland, higher rates of Stamp Duty Land Tax may apply. GOV.UK explains the rules for higher rates of Stamp Duty Land Tax.

You can also use the Connect Mortgages Stamp Duty Calculator to estimate possible costs before you apply.

Landlords should also consider income tax, allowable expenses, Capital Gains Tax and ownership structure.

For individual landlords, GOV.UK explains the rules on residential landlord finance cost relief.

A mortgage adviser can explain mortgage options. However, they do not replace a qualified tax adviser.

Landlord Responsibilities

Both routes can make you a landlord.

That matters because a mortgage is only one part of the decision. Once tenants move in, the property becomes an ongoing responsibility.

You may need to consider:

- Tenancy agreements

- Deposit protection

- Safety checks

- Repairs and maintenance

- Letting agent support

- Buildings cover

- Rent collection

- Void periods

- Local authority rules

- HMO licensing if relevant

You may also need suitable landlord insurance to protect the property and rental arrangement.

A rental property should be treated as a business responsibility, not just a mortgage asset.

When Let-to-Buy May Fit

Let-to-buy may fit when your current home has strong rental demand and enough equity.

It may also fit when you want to move but believe the current property still has long-term value.

It can be useful if:

- You are moving home but do not want to sell

- Your current home could rent well

- You need equity for the next deposit

- You can afford both mortgages

- You understand landlord duties

- You have a clear plan if the property is empty

- You are comfortable holding two properties

The main question is not whether you can keep the home. The better question is whether keeping it improves your position.

When Buy-to-Let May Fit

Buy-to-let may fit when your aim is property investment.

It may suit you if the numbers work after rent, mortgage costs, tax, repairs, insurance and void periods.

It can be suitable if:

- You want to buy a rental property

- You already own rental property

- You want to expand a portfolio

- You are reviewing an existing rental mortgage

- You are considering a limited company structure

- You understand the risks of rental income

- You have a clear repayment or exit plan

A buy-to-let property should not be judged by rent alone. The full cost of ownership matters.

Let-to-Buy vs Buy-to-Let: Which Is Better?

Neither route is automatically better.

Let-to-buy may be better if you are moving home and want to retain your current property.

Buy-to-let may be better if your main goal is buying or refinancing a rental investment.

The right answer depends on:

- Your reason for keeping or buying the property

- Your income

- Your deposit

- Your current mortgage

- The property value

- The expected rent

- Your tax position

- Your risk tolerance

- Your long-term plan

A mortgage should serve the plan. It should not become the plan.

Common Mistakes to Avoid

Many borrowers compare let-to-buy and buy-to-let too late.

They start with the property, then try to make the finance fit. A stronger approach starts with the numbers.

Common mistakes include:

- Assuming rent will cover everything

- Forgetting higher stamp duty costs

- Ignoring tax before choosing ownership structure

- Underestimating void periods

- Releasing too much equity

- Applying before checking lender criteria

- Assuming all lenders treat cases the same

- Forgetting early repayment charges

- Not checking consent to let options

- Treating landlord duties as an afterthought

Good planning does not remove risk. It makes the risk visible before you commit.

Documents You May Need

Lenders may ask for different documents depending on the route.

For let-to-buy, you may need:

- Proof of income

- Bank statements

- Current mortgage statement

- Property valuation

- Rental valuation

- Deposit evidence

- Details of the new property

- Solicitor details

- Proof of identity and address

For buy-to-let, you may need:

- Proof of deposit

- Expected rental income

- Property details

- Personal income documents

- Portfolio schedule if relevant

- Limited company documents if applicable

- Credit history details

- Proof of identity and address

Preparing documents early can reduce delays.

Speak to an Adviser

Let-to-buy and buy-to-let can look similar from the outside. In practice, they answer different questions.

Let-to-buy asks: can I move home and keep my current property?

Buy-to-let asks: can this rental property work as an investment?

If you want to compare both routes, you can also find a buy-to-let mortgage adviser through Connect Experts.

An adviser can review your income, equity, deposit, rental estimate, credit profile and timing before you apply.

FAQ: Let-to-Buy vs Buy-to-Let

What is the main difference between let-to-buy and buy-to-let?

Let-to-buy usually means renting out your current home while buying a new home to live in. Buy-to-let usually means buying or refinancing a property mainly to rent it out.

Do I need two mortgages for let-to-buy?

Usually, yes. You may need one mortgage for the property being rented and another residential mortgage for the new home.

Is buy-to-let only for experienced landlords?

No. Some lenders consider first-time landlords. However, criteria vary, and deposit requirements may be stricter.

Can I use rental income for a let-to-buy mortgage?

Yes, lenders may use expected rent when assessing the retained property. They may rely on a rental valuation.

Will I pay higher stamp duty on let-to-buy?

You may pay higher rates if you buy another residential property and keep your previous home. Tax advice should be taken before you commit.

Can I live in a buy-to-let property?

Usually, no. A buy-to-let mortgage is designed for a property rented to tenants. Speak to an adviser if your plans change.

Is let-to-buy good for moving home?

It can be useful if you want to move and keep your current property. However, affordability, equity, rental demand and timing must all work.

Is buy-to-let still worth it?

Buy-to-let can work for some landlords, but the numbers must be reviewed carefully. Mortgage rates, tax, repairs, void periods and regulation all affect returns.

Should I get tax advice before choosing either route?

Yes. A mortgage adviser can explain lending options, but tax advice should come from a qualified tax adviser.

Which route is faster?

Buy-to-let may be simpler if it involves one property. Let-to-buy can take longer because two mortgages and two property transactions may need to align.