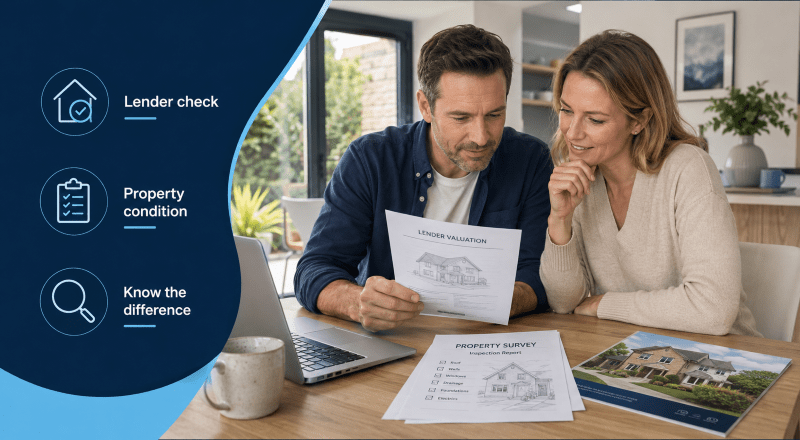

Mortgage Valuation Versus Survey: A mortgage valuation and home survey examine the same property for different reasons.

The lender’s valuation considers mortgage security.

A home survey helps the buyer understand the property’s condition.

Confusing the two can leave important defects unexplored.

The lender asks whether the property supports the loan. The buyer must ask whether the property supports their plans.

Valuation Versus Survey

- A mortgage valuation is primarily for the lender.

- A home survey is commissioned for the buyer.

- A valuation may not involve an internal inspection.

- A survey provides more information about property condition.

- A satisfactory valuation does not mean the home has no defects.

- The appropriate survey level depends on the property.

Mortgage Valuation Versus Survey Comparison

| Point | Mortgage valuation | Home survey |

|---|---|---|

| Main customer | Mortgage lender | Property buyer |

| Main purpose | Assess mortgage security | Assess property condition |

| Who arranges it | Lender | Buyer |

| Inspection detail | Limited | Depends on survey level |

| Defect reporting | Limited | More detailed |

| Market value | Usually considered | Optional within some reports |

| Repair advice | Usually limited | May be included |

| Mortgage requirement | Commonly required | Usually the buyer’s choice |

What Is a Mortgage Valuation?

A mortgage valuation helps the lender assess the property.

The lender considers whether it provides suitable security for the requested loan.

The assessment may use:

- Automated property data.

- Desktop research.

- An external inspection.

- A physical inspection.

- Recent comparable sales.

The lender chooses the method.

Borrowers cannot usually request a physical visit when the lender considers electronic evidence sufficient.

Our guide to the mortgage valuation process explains what lenders may check.

What Is a Home Survey?

A home survey provides information about the property’s condition.

The buyer appoints the surveyor and receives the report.

The survey can help identify:

- Visible defects.

- Repair requirements.

- Damp.

- Roof concerns.

- Structural movement.

- Insulation issues.

- Safety concerns.

- Areas needing further investigation.

The detail depends on the service selected.

What Are the RICS Home Survey Levels?

RICS Home Survey Level 1

This is the least detailed RICS Home Survey.

It may suit a conventional property appearing to be in reasonable condition.

It provides a basic overview using condition ratings.

RICS Home Survey Level 2

This provides more detail than Level 1.

It may suit many conventional properties in reasonable condition.

A Level 2 service may be offered with or without a valuation.

RICS Home Survey Level 3

This provides a more detailed assessment.

It may suit:

- Older properties.

- Unusual construction.

- Poorly maintained homes.

- Extensively altered properties.

- Homes requiring major work.

RICS publishes the current framework through its Home Survey standard.

Why Does a Mortgage Valuation Not Replace a Survey?

The lender’s valuation has a narrower purpose.

It may not provide detailed information about repairs or maintenance.

Some valuations are completed without entering the property.

Even a physical mortgage valuation remains limited to the lender’s instructions.

A property may therefore receive an acceptable lender valuation while containing expensive defects.

Does a Home Survey Affect the Mortgage?

The survey belongs to the buyer.

However, serious findings may affect the buyer’s decision.

The buyer could:

- Continue without changing the offer.

- Request specialist reports.

- Renegotiate the price.

- Ask the seller to complete work.

- Reconsider the purchase.

- Inform the lender about material issues.

Applicants should not hide significant information affecting the lender’s security.

Should You Arrange Both?

Many mortgage buyers will have a lender valuation and choose a separate survey.

Whether to commission a survey depends on:

- Property age.

- Construction.

- Condition.

- Planned alterations.

- Previous extensions.

- Visible defects.

- Buyer risk tolerance.

- Available warranties.

A new property is not automatically free from defects.

A warranty also does not provide the same information as an independent inspection.

When Should the Survey Be Arranged?

The buyer usually arranges a survey after the offer has been accepted.

Some buyers wait until the lender has completed initial checks.

Others book earlier to reduce delays.

The appropriate timing depends on:

- Transaction speed.

- Surveyor availability.

- Mortgage progress.

- Refund terms.

- Property demand.

- Buyer priorities.

Discuss the timing with the solicitor, adviser and surveyor.

Can You Upgrade the Lender’s Valuation?

Some lenders or valuation firms may offer an upgraded service.

However, the buyer should check:

- Who receives the report.

- What inspection level applies.

- Whether the surveyor owes a duty to the buyer.

- What is included.

- Whether a valuation is included.

- The complaints process.

- The total cost.

A separate survey can provide a clearer contractual relationship with the surveyor.

Which Report Protects the Buyer?

The home survey is designed to inform the buyer.

The mortgage valuation principally protects the lender’s lending decision.

Neither report guarantees that every defect will be identified.

Each service has limits stated within its terms.

How Can a Mortgage Adviser Help?

A mortgage adviser can explain the lender’s valuation requirement.

They should not choose the buyer’s survey or provide structural advice.

However, they can clarify:

- Whether a valuation fee applies.

- Whether the lender offers an upgrade.

- How the valuation affects LTV.

- Whether further property reports are required.

- How a valuation issue affects the mortgage.

Connect Lifetime also explains wider property borrowing through its residential mortgage guide.

Speak to Connect Mortgages

A valuation and survey ask different questions about the same property.

Understanding that difference helps protect both the mortgage application and buying decision.

Connect Mortgages can explain the lender’s valuation requirements within your mortgage journey.

Discuss your home purchase with our mortgage team.

FAQs About Valuations and Surveys

Is a mortgage valuation a survey?

No. It is a limited assessment completed for the lender’s mortgage decision.

Does an approved valuation mean the property is sound?

No. It does not confirm that the property has no defects.

Does every homebuyer need a Level 3 survey?

No. The suitable survey depends on the property and required detail.

Can I rely on the lender’s valuation?

It should not be treated as a detailed report for the buyer.

Does a survey include a market valuation?

Some services include one. Check the surveyor’s terms before proceeding.

Can survey findings help renegotiate the price?

They may provide evidence, but the seller is not required to renegotiate.

Your home may be repossessed if you do not keep up repayments on your mortgage.