Remortgage to Consolidate Debt: What Homeowners Should Check – Debt is not only a number on a statement. It can shape how a household feels each month.

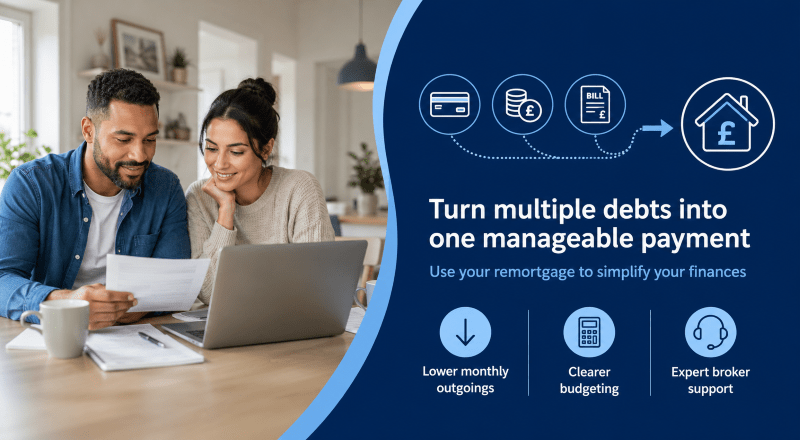

For some homeowners, a remortgage to consolidate debt may create a simpler route forward. Several repayments can be replaced with one mortgage payment. This may reduce monthly outgoings and make budgeting clearer.

However, this choice needs careful thought. Unsecured debts, such as credit card debt or personal loans, may be secured against your home. That can change the risk, even when the monthly payment looks lower.

At a Glance

A debt consolidation remortgage may help homeowners combine selected debts into one mortgage payment. It may reduce monthly costs, but it can also increase the total amount repaid over time. Lenders will check equity, income, credit history, affordability and the reason for extra borrowing. Advice is important because securing short-term debt against your home is a serious decision.

Your home may be repossessed if you do not keep up repayments on your mortgage or loans secured on it.

What Does Remortgaging to Consolidate Debt Mean?

A remortgage means replacing your current mortgage with a new deal. This may be with your existing lender or a different lender.

When debt consolidation is involved, you may borrow more than your current mortgage balance. The extra funds are then used to repay selected debts. These may include credit cards, loans or other unsecured credit commitments.

You can read more about the wider remortgage process on our remortgage guide.

The aim is usually to reduce monthly payments and consolidate them into a single structured repayment. However, a lower monthly payment does not always mean a lower total cost.

Why Homeowners Consider This Route

Homeowners may look at debt consolidation when several monthly repayments become difficult to manage. Different payment dates, interest rates and balances can make household budgeting harder.

A remortgage may help by:

- combining selected debts into one monthly payment

- reducing monthly outgoings

- moving higher-interest unsecured debt onto a lower mortgage rate

- creating clearer payment dates

- reviewing the mortgage at the same time

Yet the decision should not be based on monthly payment alone. A mortgage is often repaid over many years. If short-term borrowing is spread over a longer mortgage term, the total interest paid may increase.

That is why the right question is not only “Can this reduce my payment?” It is also “What will this cost over the full term?”

What Lenders May Check

A lender will usually not approve additional borrowing without reviewing the full case. Debt consolidation is still borrowing against a mortgage, so affordability matters.

Lenders may check:

- your income and employment status

- existing mortgage balance

- property value

- available equity

- loan-to-value

- credit history

- current debts and monthly commitments

- household spending

- dependants and regular costs

- the reason for the extra borrowing

- whether the new payment is affordable

If you have missed payments or had credit issues, lender choice may become more important. You may also need more detailed advice if your income is variable, if you are self-employed, or if it is complex.

You can read more about this area on our adverse credit mortgage page.

The Role of Equity and Loan-to-Value

Equity is the difference between your home’s value and the mortgage still owed.

For example, if your home is worth £300,000 and your mortgage is £180,000, you have £120,000 equity before costs.

However, this does not mean you can borrow all that equity. Lenders set maximum loan-to-value limits. They also assess whether the new mortgage is affordable.

If property values have changed, your available equity may be lower than expected. A valuation may therefore form part of the process.

Costs That Need to be Included

A debt consolidation remortgage may include fees. These can affect whether the arrangement makes financial sense.

Possible costs include:

- product fees

- valuation fees

- legal fees

- broker fees

- early repayment charges

- exit fees from your current lender

- charges linked to repaying existing debts early

These costs should be reviewed before any decision is made. A lower monthly payment can look attractive, but fees may reduce the benefit.

It may also be worth using an affordability tool before speaking to an adviser. Our residential affordability calculator can help you start that review.

Why Aadvice Matters

Debt consolidation is not suitable for everyone.

A broker can help compare a full remortgage, a product transfer, a further advance or a second charge mortgage. Each option has different costs, risks and lender rules.

A second-charge mortgage may be considered when replacing the main mortgage is not suitable. This could apply if the current mortgage has a strong rate or high early repayment charges.

The right route depends on the numbers, the timing and the reason for borrowing. It also depends on whether the homeowner can avoid building up new unsecured debt after consolidation.

This is where advice becomes more than product selection. It becomes a test of the plan’s stability.

Why Connect Experts May Help

Some debt consolidation cases are straightforward. Others are not.

You may need an adviser who understands remortgaging, credit commitments, affordability checks and lender criteria. If your case involves complex income, credit issues or a high loan-to-value, adviser choice can matter.

Connect Experts helps homeowners search for advisers by location, language and mortgage area. You can use the directory to find remortgage mortgage brokers who can review your options.

You can also use the wider find mortgage advisers page if you want to compare advisers across different mortgage needs.

Connect Experts is a directory and matching platform. Advice is provided by the adviser or firm selected by the customer.

Independent Guidance to Consider

Before securing debts against your home, it is sensible to understand the wider debt position. Free guidance from MoneyHelper on debt consolidation loans explains when consolidation may help and what risks to consider.

If you are struggling with repayments, free debt advice may be more appropriate before taking on further secured borrowing.

FAQs

Can I remortgage to pay off credit cards?

It may be possible if you have enough equity and meet lender affordability checks. However, credit card debt is usually unsecured. Adding it to your mortgage may secure that debt against your home.

Will a debt consolidation remortgage reduce my monthly payments?

It may reduce monthly payments, especially if debts are spread over a longer mortgage term. However, the total amount repaid may increase.

Do all lenders accept debt consolidation?

No. Lenders have different rules. Some may limit the amount, ask for evidence or apply stricter affordability checks.

Is a remortgage better than a personal loan?

Not always. A personal loan may keep the borrowing unsecured. A remortgage may offer a lower rate, but it can increase risk and long-term cost.

Should I speak to a broker first?

Yes, advice is strongly recommended. A broker can compare options and explain whether a remortgage, further advance, product transfer or second charge mortgage may be more suitable.