First Charge Bridging Loans: Short-term property finance where the lender takes first priority

First charge bridging loans are short-term property loans secured against a property as the main charge.

This means the bridging lender has first priority over the property if the loan is not repaid. In simple terms, they are first in line to be repaid from the sale or refinance of the property.

They can be useful when a property purchase, refinance or project needs to move faster than a standard mortgage allows.

However, first charge bridging loans are not suitable for every borrower. They can carry higher costs than standard mortgages, and they need a clear exit strategy from the start.

Source reference: The FCA Handbook explains that some secured loans, including bridging loans, may fall within regulated mortgage contract rules where the relevant conditions apply. It also confirms that a mortgage contract may be secured by a first, second or later mortgage. Read the FCA Handbook on regulated mortgage contracts

First Charge Bridging Loans at a Glance

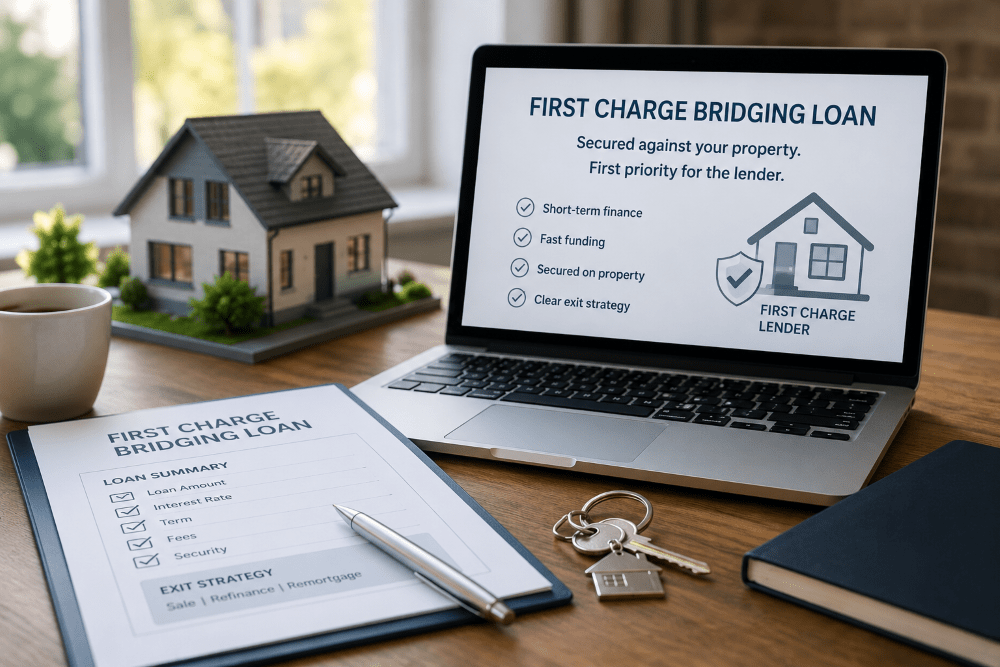

A first charge bridging loan is a short-term loan secured against a property, with the lender having first repayment priority.

It may be used when you need fast funding for a purchase, an auction deadline, a chain break, refurbishment, refinancing, or a property investment.

The loan is usually repaid through property sale, remortgage, refinance or another agreed exit.

Before applying, you should understand the interest, fees, security, repayment plan and risk to the property.

What Is a First Charge Bridging Loan?

A first charge bridging loan is a short-term loan secured against a property.

The phrase “first charge” refers to the lender’s legal position on the property. If the property is sold because the loan is not repaid, the first charge lender is repaid before any later charge lender.

This is different from a second charge loan, where another lender already has first priority.

A first charge bridging loan may apply where:

- The property has no existing mortgage.

- The existing mortgage will be repaid when the bridge completes.

- The bridging loan will replace the current secured borrowing.

- The property is being purchased with short-term funding.

For a broader overview, read our guide to bridging loans.

How First Charge Bridging Loans Work

A first charge bridging loan is usually built around four points.

- The property being used as security.

- The amount you want to borrow.

- The loan-to-value.

- The exit strategy.

The lender reviews the property, the purpose of the loan and how the borrowing will be repaid.

The exit route is important because bridging finance is not designed to run long-term. The loan may be repaid through a sale, a remortgage, a commercial mortgage, a buy-to-let mortgage, or another agreed refinancing route.

If the exit route is weak, the loan may not be suitable.

When First Charge Bridging Loans May Be Used

First charge bridging loans are often used when timing matters.

Common examples include:

- Buying a property at auction.

- Completing quickly after a chain break.

- Buying before selling another property.

- Funding refurbishment before sale or refinance.

- Buying a property that needs work before a standard mortgage.

- Raising short-term capital against an unencumbered property.

- Purchasing commercial or semi-commercial property.

- Moving from short-term finance to a longer-term mortgage.

If your case involves business premises, you may also want to read our guide to commercial mortgages.

If the property will be rented out, our buy-to-let mortgage guide may also help.

First Charge vs Second Charge Bridging Loans

The main difference is repayment priority.

A first charge bridging loan is the main secured loan on the property. The lender has first claim over sale proceeds if the loan is not repaid.

A second charge bridging loan sits behind an existing mortgage or loan. The first charge lender is repaid first, then the second charge lender.

This matters because the lender’s risk can affect pricing, criteria and available loan options.

A first charge bridge may be considered where the current mortgage is being cleared or where the property is owned without secured borrowing.

A second charge option may be considered if an existing mortgage remains in place.

You can also read about second charge mortgages if you want to compare the differences.

Regulated and Unregulated First Charge Bridging Loans

Some first charge bridging loans may be regulated. Others may be unregulated.

A bridging loan may be regulated where it is secured on a home used, or intended to be used, by the borrower or a close family member, subject to the relevant rules.

Unregulated bridging finance is more common where the borrowing relates to business, investment, commercial property or certain buy-to-let cases.

This distinction matters because the advice process, lender requirements and borrower protections may differ.

The FCA Handbook sets out when a mortgage contract may fall within regulated mortgage contract rules. Read the FCA guidance

You can also read our guide to regulated bridging loans.

What Costs Should You Consider?

First charge bridging loans can be more expensive than standard mortgages.

You may need to consider:

- Monthly interest.

- Rolled-up interest.

- Arrangement fees.

- Valuation fees.

- Legal fees.

- Broker fees.

- Exit fees, where applicable.

- Default interest if the loan runs beyond the agreed term.

Some loans allow interest to be rolled up. This means the interest is added to the loan and repaid at the end.

This can help cash flow, but it also increases the balance that must be repaid.

Why the Exit Strategy Matters

The exit strategy is the planned way to repay the bridging loan.

Common exit routes include:

- Selling the property.

- Selling another property.

- Remortgaging.

- Moving to a buy-to-let mortgage.

- Moving to a commercial mortgage.

- Refinancing after refurbishment.

- Using agreed funds from another completed transaction.

The lender will want to understand whether the exit is realistic.

For example, a property sale may depend on market conditions. A refinance may depend on income, valuation, rental income or works being completed.

A strong exit route can reduce risk. A weak exit route can increase cost, delay or decline risk.

Risks of First Charge Bridging Loans

First, charge-bridging loans can help in the right situation, but they carry risk.

You should consider:

- The property may not sell on time.

- A refinance may not be approved.

- Refurbishment work may cost more than planned.

- Interest can build quickly.

- Fees can increase the total cost.

- The property is at risk if the loan is not repaid.

- Some bridging loans are not regulated by the FCA.

MoneyHelper explains that secured borrowing uses an asset as security. It also warns that the asset may be lost if repayments are not maintained. Read MoneyHelper’s guide to secured borrowing

Your home may be repossessed if you do not keep up repayments on your mortgage or loans secured on it.

First Charge Bridging Loan Example

A buyer agrees to purchase a property at auction.

The auction terms require completion within a fixed deadline. A standard mortgage may not complete quickly enough.

A first charge bridging loan could help complete the purchase.

The loan may then be repaid by sale, refinancing, or a longer-term mortgage once the property meets the lender’s criteria.

This is only an example. Suitability depends on the property, borrower, loan purpose, costs and exit strategy.

Who Might Need First Charge Bridging Loan Advice?

You may want advice if you are:

- Buying at auction.

- Buying before selling.

- Dealing with a chain break.

- Funding light refurbishment.

- Buying an unmortgageable property.

- Refinancing short-term property debt.

- Buying commercial or mixed-use property.

- Raising short-term capital against property.

- Planning to refinance onto a longer-term mortgage.

A specialist adviser can help assess whether a first charge bridge fits your circumstances.

If you prefer to choose an adviser by expertise, location, or language, you can also find a bridging-loan mortgage broker through Connect Experts.

Alternatives to a First Charge Bridging Loan

A first charge bridging loan is not always the best route.

Depending on your circumstances, alternatives may include:

- A standard residential mortgage.

- A remortgage.

- A further advance.

- A second charge mortgage.

- A buy-to-let mortgage.

- A commercial mortgage.

- Development finance.

- Refurbishment finance.

The right option depends on timing, property type, repayment plan, affordability and risk.

For larger works or development projects, read our guide to development finance.

Why Speak to Connect Mortgages?

First charge bridging finance is not only about speed.

The structure matters.

Connect Mortgages can help you review the property, loan purpose, exit strategy and possible alternatives before you apply.

We can help you understand:

- Whether a first charge bridge may fit your situation.

- What lenders may consider.

- How the exit strategy may be assessed.

- What costs and risks may apply.

- Whether another finance route may be more suitable.

Frequently Asked Questions

What is a first charge bridging loan?

A first charge bridging loan is a short-term loan secured against property. The lender has first repayment priority if the property is sold or refinanced.

Is a first charge bridging loan the same as a mortgage?

No. It is secured against property, but it is short-term finance. A standard mortgage is usually arranged over a much longer term.

How long does a first charge bridging loan last?

Terms vary by lender and case. Bridging loans are usually short-term and should have a clear repayment plan before completion.

What can a first charge bridging loan be used for?

It may be used for auction purchases, chain breaks, buying before selling, refurbishment, refinance or time-sensitive property transactions.

Is a first charge bridging loan regulated?

Some first charge bridging loans may be regulated. This depends on the property, borrower and purpose of the borrowing.

What is the main risk?

The main risk is that the exit strategy fails. If the loan is not repaid, the property used as security may be at risk.

Can I use a first charge bridge for a buy-to-let property?

Yes, in some cases. The loan may be used to buy or refinance a rental property before moving to a longer-term buy-to-let mortgage.

Do I need an exit strategy?

Yes. A clear exit strategy is essential. Lenders need to understand how the loan will be repaid.

Speak to Connect Mortgages About First Charge Bridging Loans

If you need short-term property finance, speak to Connect Mortgages before you apply.

We can help you understand whether a first charge bridging loan may fit your plans, risks and repayment route.

Your home may be repossessed if you do not keep up repayments on your mortgage or loans secured on it.

Connect Mortgages is a trading style of Connect IFA Ltd, which is authorised and regulated by the Financial Conduct Authority.